In today’s business landscape, small business owners face the challenge of navigating through financial uncertainties to secure a prosperous future for their enterprises. At the heart of this challenge lies the need for adequate financial forecasting. This tool goes beyond mere prediction as a strategic compass guiding businesses toward stability and growth. Recognizing this, Xendoo strives to be an ally for small businesses, offering a comprehensive suite of financial tools and services designed to empower entrepreneurs. From advanced cloud-based accounting software and AI-driven analytics to personalized financial advisory services, Xendoo equips small business owners with the resources to create precise financial forecasts, manage cash flow efficiently, and make informed decisions.

Moreover, for small business management, gaining control of their financial future is necessary and an added advantage. Amid this crucial requirement, financial forecasting emerges as a beacon of guidance, empowering businesses to navigate uncertainty confidently. This is where the role of Fractional CFOs and comprehensive financial services like Xendoo become pivotal. This blog sets the stage for an in-depth exploration of how Xendoo’s solutions and expert guidance transform the financial forecasting landscape, enabling small businesses to envision and actively shape their financial future.

Cloud-Based Accounting Software:

Cloud-based accounting software, prominently featured in Xendoo’s suite of financial tools, revolutionizes how small businesses approach their finances. Platforms like QuickBooks Xero offer more than convenience; they provide a foundation for transformative financial management. By enabling real-time tracking and analysis, these software solutions ensure that businesses can keep a constant pulse on their financial health. Integrating expense tracking, invoicing, and detailed financial reporting streamlines the complex financial forecasting process. This not only demystifies the gathering and analysis of critical financial data but also enhances the accuracy and reliability of forecasts. For small businesses, this means the ability to anticipate financial challenges and opportunities with a new level of precision. By leveraging cloud-based accounting software, businesses can make informed decisions, plan strategically for the future, and maintain a competitive edge in their respective markets, all through the power of efficient and accessible financial management tools provided by Xendoo.

AI and Machine Learning Tools:

Integrating Artificial Intelligence (AI) and Machine Learning (ML) in financial forecasting represents a revolutionary leap forward. Xendoo harnesses these advanced technologies to offer small businesses a competitive edge in financial management. Our AI and ML algorithms are designed to delve deep into extensive datasets, extracting patterns and trends that might elude traditional analysis. This capability enables the prediction of future financial outcomes with high precision and furnishes businesses with actionable insights to guide strategic decision-making. Automating forecasting processes through these intelligent tools reduces the potential for human error, ensuring that the forecasts are reliable and robust. By embracing AI and ML, Xendoo elevates financial forecasting from a necessary chore to a strategic asset, empowering businesses to anticipate challenges, seize opportunities, and confidently navigate the future, thus markedly enhancing their forecasting accuracy and overall financial strategy.

Financial Dashboards and Analytics Platforms:

Consequently, Xendoo’s financial dashboards and analytics platforms are pivotal tools for small businesses, providing a consolidated view of financial data and valuable insights into financial health and forecasting metrics. By offering a comprehensive visualization of their financial data, our service enables small business owners to understand their current financial position and forecast future trends. This comprehensive view empowers proactive and strategic decision-making, allowing businesses to make informed choices to drive growth and success. With Xendoo’s dashboards, small business owners can efficiently monitor critical financial indicators, identify patterns, and anticipate future challenges and opportunities. Visualizing financial data in a single view enhances transparency, fosters better financial management, and equips businesses with the knowledge to navigate their financial landscape confidently and strategically.

Cash Flow Management Tools:

Xendoo recognizes that managing cash flow is crucial for the sustainability of small businesses. Our platform offers invaluable insights into cash flow patterns, empowering businesses to effectively manage their liquidity and prevent cash shortages. Through our cash flow management tools, entrepreneurs can understand their cash flow dynamics comprehensively, enabling them to maintain a healthy financial position and allocate resources optimally. By monitoring cash inflows and outflows, businesses can make informed decisions regarding expenditures, investments, and operational strategies. This proactive approach safeguards against liquidity challenges and facilitates the prudent allocation of funds toward growth initiatives. Ultimately, Xendoo’s cash flow management tools provide small businesses with the insight and control necessary to navigate their financial landscape confidently and financially.

Online Financial Advisory Services:

Xendoo’s commitment to facilitating the success of small businesses extends beyond providing software solutions. While fintech companies and online platforms offer personalized financial advice, Xendoo offers a comprehensive package with access to financial experts and cutting-edge software solutions. This unique integration enables small businesses to benefit from expert financial forecasting and risk management guidance while leveraging the latest financial technology. By combining the insights and expertise of financial experts with advanced software, Xendoo empowers businesses to make informed, strategic decisions while securing their financial future. This approach provides small businesses the resources and support to navigate complex financial landscapes confidently, ensuring sustainable growth and success.

In conclusion, small business owners face the crucial challenge of navigating financial uncertainties to secure a prosperous future in the competitive business world. Particularly in this context, the role of Fractional CFOs and comprehensive financial services like Xendoo becomes pivotal. Xendoo’s suite of financial tools and services, which includes cloud-based accounting software, AI and machine learning tools, financial dashboards, cash flow management tools, and online financial advisory services, equips small business owners with the resources they need to create precise financial forecasts, manage cash flow efficiently, and make informed decisions. Xendoo’s innovative solutions and expert guidance transform the financial forecasting landscape, enabling small businesses to envision and actively shape their financial future. By providing businesses with robust and reliable financial management tools, Xendoo empowers them to make informed decisions, strategically plan for the future, and maintain a competitive edge in the market. Through advanced technology and expert support, Xendoo ensures sustainable growth and success for small businesses. Visit Xendoo.com today to explore how our tailored financial solutions can unlock the full potential of financial forecasting for your small business, guiding you toward a successful journey.

It is exciting to start a business, but beyond having a great idea, one needs to work out many things as well. Small and medium-sized enterprises (SMEs) frequently need help shaping their brand in a constantly changing environment where invention, market comprehension, and efficient management are key factors. One crucial thing that may become a success or failure determiner for a startup is how it handles its financial affairs. Good accounting practices not only conform a business to regulations but also create valuable information that can grow the business. This article discusses how entrepreneurial accounting helps progress from a startup to success.

Understanding the Essence of Bookkeeping

Accounting combines precise and well-kept bookkeeping, which is vital in every flourishing business. Bookkeeping ties these deals together by registering any financial transaction: sales, purchases, receipts, and payments. Maintaining flawless and up-to-date records for small business owners involves keeping records of how income and expenses are split, how cash flow is managed, and how taxes are prepared. Based on my experience, the critical idea of a successful SMB accounting system is in high demand. Bookkeeping hit the boundary of causing calculated mathematical operations, including all processes of systematic transaction recording, accurate expense tracking, and the efforts in managing the cash flow.

Getting bookkeeping help from expert firms like Xendoo may jump-start your small business’s journey to success. Not only does it aid in time management, but it also guarantees the accuracy of financial records in line with regulations. The fact that Xendoo.com exists as an accounting outsourcing firm makes it, unlike an ordinary accountant or calculator. When a CEO outsources the handling of the finances to the experts, they can free time and gratis it again to impelling business growth while upgrading their company’s finances. This allows them to channel their energies into what they do best – their most apt trade.

Challenges Faced by Small Business Owners

Accounting requirements can be challenging for many small enterprises because they grow without basic operational procedures during the initial business period. Time pressure, resource scarcity, and the lack of professional skills that contribute to the quality of financial management are relatively common obstacles. As a result, wrong entries in bookkeeping may emerge, which can result in financial discrepancies, missed tax deadlines, and, in the end, exactly, threaten the sustainability of the business.

In addition, companies with expanding operations and a large quantity of paperwork will see a wide variety in their transactions boom at an equal charge. During those moments, guide bookkeeping systems cannot reply to operational worries, making printing errors vital. Small commercial enterprise owners increasingly turn to outsourced bookkeeping services, which offer a strategic alternative for financially retaining a commercial enterprise, even permitting the owner to pay attention to their number one duties.

The Advantages of Outsourced Bookkeeping

Engaging a bookkeeping company is like a gift in a box since businesses can handle bookkeeping alone or pay high organization accounting fares. Another main advantage is the availability of talented accountants, no complete staff hiring, and, therefore, managers. These experts ensure compliance with the rules and, if necessary, inspect compliance through audits and checklists. Unlike these, contracting out in one way or another allows the proprietorships to grasp all over their production schemes, connections, and clients to achieve all-over productivity and scalability. Moreover, software of such power helps individuals navigate processes that let them eliminate errors or missteps and take quick actions from the software, making them a top competitor.

Driving Business Growth Through Effective Financial Management

In today’s competitive world, where rival features are constantly emerging, agility and adaptability are crucial for either survival or growth. Well-structured accounting practices provide small business owners with the necessary inputs for decision-making, identification, and handling of risks, as well as opening up to the opportunities that may be available. Through precise financial records, businesses can focus on the trend of cash flow, monitor expenses, and identify when efficiency is sliding low or the company is overspending money.

Furthermore, strategic financial planning empowered by outsourced bookkeeping services supports businesses in devoting the resources where they are needed and choosing the investments that make the best economic sense. All these financial decisions are taken if you deal with expanding operations, new products, or entering new markets, but they create a base for sustainable development and profitability.

Moreover, outsourcing the bookkeeping processes will associate the business with credibility and reputation, build trust with shareholders, and invite investment or partnerships. Credible and trustworthy financial reporting will favor transparency and fiscal responsibility, again showing that these features are essential for building a marketplace.

Navigating Growth: Solutions Offered by Xendoo.com

Xendoo.com gives small and medium-sized businesses (SMBs) the tools they require to explain and manage their financials and, in turn, to grow sustainably and remain competitive. Xendoo.com, being a bookkeeping expert platform, helps local businesses (SMBs) take control of their finances and minimize time and resources that can be used to perform their core business activities. By carefully developing and optimizing tax planning strategies, Xendoo.com translates those savings into business growth, boosting financial resources strategically. Apart from CFO services outsourced through Xendoo.com, owners and business managers can set strategies that place them in superior decision-making characteristics. SMBs, having a partnership with Xendoo.com, could work with a group of relying professionals with the required competencies and tools for the successful handling of financial challenges and for maximizing profit. Success as SMBs see the light at the end of the tunnel with Xendoo.com by their side, and it’s just a matter of time before they reach the echelons of successful businesses with confidence and clarity of purpose, finally digging their feet deep in the path to a sustainable future.

In conclusion, accounting discipline is necessary for the growth and sustainability of small and medium-sized enterprises. To eliminate difficulties in financial accountability, entrepreneurs should consider the utility of outsourced bookkeeping. Such a move would boost the overall development of the business. It is catching up because effective bookkeeping makes perfect record-keeping, a strategic tool for growth, innovation, and resilience in our current economy. Being small business owners and going to achieve the path from startup to success, partnering with a credible accounting provider can become the differentiator from others, taking your business to the green pastures and prosperity.

We share your passion for small businesses and are inspired by your dedication to making your dreams a reality. That’s why we’re committed to providing you with the financial visibility and support you need to thrive.

More Than Just Numbers

It’s more than simply crunching numbers. It’s about building meaningful relationships with our clients and understanding their needs. Our people-first mentality ensures you receive personalized attention and expert guidance throughout your financial journey.

A One-Stop Solution

Xendoo offers a comprehensive suite of services, including:

Full-service bookkeeping and accounting team to free up your time and resources.

Hassle-free tax preparation and filing

Fractional CFO Services to work with you on a roadmap of future growth

A dashboard that provides real-time financial insights

Passionate about your success?Xendoo is, too. We provide the financial visibility and support small businesses need to thrive and scale. Let us handle the financial burden so you can focus on what matters most – running your business and achieving your goals.

Contact Xendoo today and discover how we can give you time back to grow your business.

Managing an eCommerce business extends beyond the simple transaction of goods online. Unlike traditional businesses, eCommerce accounting involves unique challenges, like managing inventory costs, tracking marketing spending across multiple channels, and dealing with complex tax regulations. These complexities can leave you needing help to make sense of your finances and unsure of your business’s true performance.

An important part of managing an eComm business is understanding and visibility of the eComm financial ecosystem, emphasizing the chosen accounting approach.

This in-depth guide will explore the complexities of eCommerce accounting.. From outlining the pivotal role of proper financial oversight to pinpointing the tangible advantages gained from streamlined accounting solutions, this guide is a valuable resource for eCommerce entrepreneurs looking to fortify their financial foundations and propel their businesses toward enduring success and growth.

The Significance of eCommerce Accounting

Running a successful eCommerce business requires clear control and visibility of your finances. It’s easier to make smart decisions for your business with clear and organized accounting.

Think of accounting as your financial roadmap. It helps you track everything from who owes you money (receivables) to whom you owe (payables), expenses, and supplier invoices. This way, you have a clear picture of your cash flow and can make informed decisions about your business, like how much to invest in inventory or marketing.

Investing in a proper accounting system that can handle the increasing complexity as your business grows is crucial. This will save you time and headaches, allowing you to focus on what matters most: growing your business.

Your eCommerce business needs insightful accounting to understand its health. It goes beyond simply keeping track of numbers. Understanding your numbers empowers you to make smart decisions. You can see where your money goes so that you can invest wisely. Accounting also helps you forecast your short-term and long-term income to plan effectively.

Good accounting helps you stay on top of taxes and avoid penalties. This frees up your time and energy to focus on what matters most – growing your business!

Accurate bookkeeping and accounting are your secret weapon against wasted spending and missed opportunities. By combining powerful analytics with your everyday bookkeeping, you will gain valuable knowledge about your business and unlock insights about your customers.

These insights are like gold. They’ll help you become laser-focused on strategies that resonate deeply with your target audience, leading to more meaningful connections and scaling your business.

That’s not all. By knowing your financial data, you can identify areas where your business can become efficient: streamlined operations, reduced costs, and more efficiency.

Plus, having all your financial data in one place gives you a clear bird’s-eye view of your business. This means you can make data-driven decisions perfectly aligned with your customers’ wants and market demands.

Understanding E-commerce Accounting: Your Guide to Profitable Decisions

E-commerce accounting might sound intimidating, but it’s ultimately about understanding your financial data to make smart business decisions that boost your profits. It helps you answer questions like:

How much money is coming in and going out?

Where can I make cuts without impacting my sales?

Am I investing in the right marketing channels?

Here’s a breakdown to make things easier:

Think of bookkeeping as the “how” and accounting as the “what” of your finances. Bookkeeping involves recording and managing daily transactions, like sales, expenses, and payments. Accounting analyzes that data to tell you the “what,” like your overall profitability and growth potential.

The foundation of good accounting is accurate bookkeeping. If you categorize and track your transactions correctly, the insights you get from the data will be reliable. This can lead to missed opportunities or even costly mistakes.

There are two main accounting methods: cash-basis and accrual.

Cash-basis accounting: Records income when you receive payment and expenses when you pay them. This is simpler and often used by startups.

Accrual accounting: Records income when it’s earned (even if not received yet) and expenses when incurred (even if not paid yet). This provides a more accurate picture of your business’s financial health but is also more complex.

The next section will delve deeper into bookkeeping practices for e-commerce businesses. We’ll explore how to keep your financial data organized and ready for valuable analysis.

Improving Your eCommerce Accounting

Insights into cash flow and comprehensive reporting capabilities are vital for eCommerce businesses to understand their financial health, monitor performance, and identify opportunities for improvement. This level of insight is especially important in the dynamic and fast-paced eCommerce environment, where quick and informed decisions can greatly impact growth and success.

Scalability for Sustainable Growth:

Some robust accounting solutions cater to both new and established businesses. Look for features that can adapt and grow alongside your company. This eliminates the need for major overhauls later on, allowing you to focus on scaling your business seamlessly.

Streamlined Processes and Reduced Errors:

Many platforms offer automated transaction tracking features. This saves you valuable time and reduces the risk of human error in recording sales and expenses.

Navigating Tax Complexities:

E-commerce businesses, especially those operating across state lines or internationally, often face complex tax requirements. Look for solutions that offer tax assistance features to help you stay compliant and avoid unnecessary complications.

Gaining Clear Financial Insights:

Comprehensive reporting capabilities and clear cash flow insights are crucial for understanding your financial health, monitoring performance, and identifying areas for improvement. This is especially important in the fast-paced world of e-commerce, where quick and informed decisions can significantly impact your success.

Multi-Channel Integration for Effortless Data Management:

Managing finances across multiple sales channels can be time-consuming and error-prone. Look for solutions that integrate seamlessly with popular e-commerce platforms like Shopify, Amazon, and eBay. This allows you to systematically consolidate and analyze your financial data from various sources, ensuring accurate and comprehensive financial visibility across your entire business.

In conclusion, choosing the right accounting tools empowers your e-commerce business to manage finances efficiently, gain valuable insights, and fuel sustained growth in the competitive landscape. Explore your options and find the solutions that best suit your needs and goals.

Practical Tips for Immediate Implementation

Employ Cash Basis Accounting: This beginner-friendly method simplifies record-keeping by tracking transactions when cash moves, making tax preparation easier.

Monitor and Categorize Transactions: Automate this process using accounting software to improve accuracy and potentially save tax through precise expense categorization.

Synchronize Sales Channels: Integrate transactions from various platforms into a single database for easier financial oversight and analysis.

Automate Tax Calculations: Simplify complex tax requirements across jurisdictions by leveraging accounting software capabilities.

Distinguish Chargebacks and Returns: Track and categorize these accurately for proper financial recording and analysis.

Generate Detailed Reports: Utilize robust reporting features to gain insights into your business, analyze performance, identify trends, and make informed strategic decisions.

Integrate Budgeting and Forecasting: Employ budgeting and forecasting tools within your accounting software to gain insight into future financial projections for informed business decisions. This helps plan for future investments, expansions, and potential challenges.

Utilize Inventory Management: Leverage accounting software’s features to track stock levels, manage inventory across locations, and optimize stock control. This ensures effective inventory management, accurate financial reporting, and informed purchasing decisions.

Automate Invoice Generation: Automate sending and generating invoices through your accounting software, saving time and ensuring accuracy, professionalism, and, ultimately, improved cash flow and client satisfaction.

Track Expenses Meticulously: Use your accounting software to track and categorize business expenses meticulously. This helps identify cost-saving opportunities, ensure compliance with tax regulations, and facilitate accurate financial reporting.

Long-Term eCommerce Accounting Strategies

Detailed Accounting Reports: Regularly analyze reports to gain insights into sales trends, profitability, and inventory management.

Cash Flow Management: Monthly cash flow statements offer a clear view of financial health, highlighting areas for potential improvement.

Scalable Accounting Policies: Regularly review and adjust your accounting practices to accommodate business growth and expansion, ensuring your systems can scale with your business.

Integration with CRM Systems: Integrate Xero with Customer Relationship Management (CRM) software to gain a comprehensive understanding of customer behavior and preferences, enabling targeted marketing strategies and improved customer engagement.

Advanced Data Analytics: Leverage Xero’s advanced analytics capabilities to delve deeper into financial and operational data, gaining profound insights for strategic planning, forecasting, and enhanced decision-making.

Next Steps with Xendoo

The next steps involve implementing your newfound understanding of e-commerce accounting to streamline your processes and unlock even greater efficiency and visibility for your business. By harnessing the synergy between robust bookkeeping and your online sales platform, businesses can optimize efficiency and lay the groundwork for sustained success in the dynamic eCommerce landscape. Let Xendoo help you remove the guesswork and embrace the power of data-driven e-commerce accounting. It’s time to build a business that’s agile, responsive, and ready to crush its goals.

In today’s rapidly evolving business environment, more than merely relying on innovation and agility is required to maintain a competitive edge; it necessitates real-time insights and data-driven decisions. Efficient bookkeeping and accounting are not mere administrative tasks for growing businesses but are strategic pillars for success. Real-time financial management empowers businesses to make informed decisions promptly, manage resources effectively, and adapt swiftly to market changes. By embracing real-time bookkeeping and accounting practices, businesses can comprehensively understand their financial health and position themselves for sustainable growth. Tailoring these practices to meet the specific needs of expanding enterprises further enhances their effectiveness, enabling businesses to navigate complexities and seize opportunities confidently. In this blog post, we delve into the significance of real-time financial management and explore how it can be customized to fuel the success of growing businesses.

The Need for Real-Time Insights

The need for real-time insights in financial management must be balanced, particularly in today’s fast-paced business landscape. Traditional bookkeeping and accounting methods, characterized by manual entry and periodic updates, are ill-equipped to meet the demands of rapidly evolving environments. While suitable for small businesses with limited transactions, these approaches falter when providing timely information crucial for decision-making.

Real-time bookkeeping and accounting offer a paradigm shift by providing continuous monitoring and instant access to financial data. This enables businesses to enhance decision-making processes significantly. With up-to-date financial information readily available, stakeholders can assess cash flow, evaluate performance, and identify growth opportunities promptly. Real-time insights empower business owners and managers to act swiftly and decisively, gaining a competitive edge in the marketplace.

Moreover, real-time financial management improves overall financial control and resource allocation. By tracking income and expenses in real time, businesses can proactively identify trends, manage cash flow effectively, and allocate resources optimally to support growth initiatives. This proactive approach enhances financial stability and resilience, mitigating risks associated with volatile market conditions.

Additionally, real-time accounting fosters adaptability, a critical factor for survival in today’s dynamic market landscape. Businesses can monitor market fluctuations, respond to emerging trends, and adjust strategies promptly based on real-time data. This agility enables businesses to stay ahead of the competition, capitalize on opportunities, and mitigate risks effectively.

In essence, adopting real-time bookkeeping and accounting practices represents a strategic imperative for businesses seeking sustainable growth and competitiveness. By leveraging real-time insights and tailoring them to their specific needs, businesses can confidently navigate uncertainties and capitalize on emerging opportunities in an ever-changing business environment.

Tailoring Solutions for Growing Businesses

While real-time bookkeeping and accounting benefits are clear, implementing these practices requires careful planning and customization, especially for growing businesses, without encountering common bookkeeping roadblocks. Here are some strategies to tailor solutions to their specific needs:

Scalable Systems:

When selecting accounting software, prioritize scalability. Opt for platforms offering flexible pricing and advanced features to adapt to growing transaction volumes and complexity. Scalable systems ensure your financial management tools can seamlessly expand alongside your business, preventing bottlenecks and inefficiencies as operations evolve. Investing in software that accommodates your company’s growth trajectory establishes a foundation for sustainable scalability, enabling smoother transitions and enhanced performance as your business flourishes.

Customized Reporting:

Customized reporting is pivotal for businesses, allowing them to develop tailored reports and dashboards aligned with their objectives. Personalized reports offer invaluable insights, whether it’s tracking key performance indicators (KPIs), monitoring departmental expenses, or assessing profitability by product lines. By providing relevant data in a format that suits decision-makers’ needs at every level of the organization, customized reporting enhances understanding and facilitates informed decision-making. It empowers businesses to identify trends, pinpoint areas for improvement, and capitalize on opportunities, ultimately driving efficiency and success.

Integration with Business Tools:

Integration with various business tools is pivotal for maximizing efficiency. Businesses create a unified ecosystem where data flows effortlessly across departments by seamlessly connecting accounting software with CRM platforms and inventory management systems. This integration minimizes manual errors, eliminates duplication of efforts, and enhances overall operational efficiency. For instance, sales data from the CRM can seamlessly sync with accounting records, providing real-time insights into revenue generation. Similarly, inventory updates can be automatically reflected in financial reports, facilitating accurate cost management. Such integration streamlines processes and empowers businesses to make data-driven decisions confidently.

Professional Support:

Collaborating with accounting specialists catering to growing businesses is invaluable. Their expertise aids in establishing robust accounting procedures, interpreting financial data accurately, and integrating best practices to foster business expansion. With their guidance, businesses can navigate financial complexities confidently, ensuring compliance and optimizing resource allocation. Partnering with seasoned professionals enhances financial management efficiency and empowers businesses to make informed decisions crucial for sustained growth.

Conclusion

In conclusion, adopting real-time bookkeeping and accounting through platforms like Xendoo.com signifies a transformation in financial management for businesses. By embracing these practices and customizing them to their unique requirements, growing enterprises position themselves advantageously in the dynamic market environment. The advantages are diverse, ranging from the ability to make swift, data-informed decisions to enhancing financial control and adaptability. As technology progresses, prioritizing real-time insights becomes increasingly critical. Businesses that integrate these practices ensure their survival and pave the way for sustained growth and competitiveness. In essence, real-time financial management isn’t just a trend but a strategic imperative for businesses striving to thrive amidst constant change and uncertainty in today’s business landscape. Leveraging platforms like Xendoo.com facilitates seamless integration of real-time financial data, further enhancing the efficiency and effectiveness of financial management processes.

Net income is one key metric that you can use to assess your business’s financial health. It is the bottom line on your income statement, also called a Profit & Loss Statement (P&L), and it tells you how much money you have remaining after deducting your costs and operating expenses from your total sales.

What Is Net Income?

Net income can be compared to “take-home pay” for an employee. It’s the amount of money remaining after taxes, insurance, and other expenses are deducted from your total pay or gross income.

Similarly, a business’s net income is the amount of money remaining after deducting all business expenses, including wages, interest, product costs, operation costs, and taxes. Net income, also known as the bottom line, net earnings, or net profit, appears at the bottom of income statements.

Generally, a healthy, growing business will have positive net incomes and increase consistently. In other words, the more you increase revenue and decrease expenses, the healthier you are.

The net income or net loss of your business may also show up on your balance sheet as retained earnings. Retained earnings are the amount of money that is held (not distributed to shareholders) to sustain and grow the business.

How Do You Calculate Net Income?

The net income formula helps calculate the net income of either an individual or a business.

Calculating net income is fairly straightforward for individuals. You take the total amount earned (gross income) and then deduct all expenses, such as interest payments and taxes. It is a little more complicated for businesses.

Net Income Formula

Businesses can use the net income formula to calculate net income for any timeframe. There are two primary ways to calculate net income: revenue and expenses or gross profit and expenses. We’ll go over each net income formula and how to use them.

Total Revenue

Total Revenue = Quantity Sold * Price – Discounts

Cost of Goods Sold

COGS is the cost of the product or the service being delivered. If you have a t-shirt company, it is the wholesale cost of the t-shirt, plus freight, labor, and printing costs. If you provide consulting services, it is the cost of labor to provide the consulting.

Gross Profit

Gross profit represents the profit made on selling the product or service. This provides insight into whether your pricing brings you the desired profit on each sale.

Gross Profit = Revenue – Costs of Goods Sold

Operating Expenses

Operating expenses are running the day-to-day business, including advertising & marketing, rent, payroll, insurance, software, website, postage, auto expenses, meals, travel, and more. These are the below-the-line (Gross Profit) costs.

Net Income

Net Income = Gross Profit – Operating Expenses

It’s important to note that net income can be a net loss. If your operating expenses exceed your gross profit, you have a net loss. When your operating expenses are less than your gross profit, you have a net income.

Often, when a business is in start-up mode, a net loss is not surprising. Although a net loss has a tax benefit, it doesn’t lead to a sustainable or scalable company without further investment.

It’s also important to note that net income may include revenue that is not from your core business activities. For example, if your business owns real estate and rents out part of it or gains royalties from a past partnership, this is generally referred to as non-operating income.

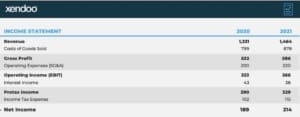

Business Net Income Example

Let’s look at a hypothetical business scenario to understand the net income formula fully.

Marcus’ Archery, a company specializing in manufacturing and selling archery equipment, wants to calculate its net income for the fourth quarter. Here are the necessary figures to calculate net income from its accounts:

Total Revenue: $20,000,000

Costs of goods sold (COGS): $8,750,000

Rent: $150,000

Utilities: $40,000

Payroll: $250,000

Advertising: $70,000

Interest expense: $70,000

According to the net income formula, Marcus’ Archery first needs to calculate Gross Profit. You would do this by subtracting the costs of goods sold, including direct labor costs, from the total revenue.

Marcus’ Archery can now calculate its net income with all these results. You use the net income formula to subtract total expenses from gross income to do this.

The fourth quarter’s net income for Marcus’ Archery is $10,670,000.

Cash Flow vs. Net Income

These are simplified explanations of how to calculate net income. However, net income does not equate to how much money is in the bank. We often hear questions like, “I made $100,000 this year, but why don’t I have $100,000 in the bank.” That is because cash flow is very different from net income

Factors like credit cards, business loans, owner’s payments, or investment income affect the money in the bank but aren’t factors in net income. You can learn more about cash flow vs. profit and how to use cash flow for decision-making in our blog.

Individual Net Income Example

We focus on business bookkeeping and accounting at Xendoo. However, looking at an individual net income example can help you better understand how it differs from calculating the net income for a business.

Let’s consider Nancy, an employee at a local ski shop. Nancy receives her paycheck every two weeks with gross pay of $4,500. She also receives $200 in interest and $600 in equity as her other forms of income.

She then pays all her taxes, including:

Social Security taxes ($279)

Federal taxes ($450)

State taxes ($163.91)

Medicare taxes ($65.25)

Insurance ($280)

These are usually automatically deducted from your paycheck. After all these deductions, Nancy has a net income of $4,061. Here are the exact steps to calculate it.

Because Nancy’s gross income includes equity and interest, it totals $5,300. Based on her biweekly paycheck, Nancy has an annual net income of $105,586.

What key financial insights can business owners gain from income statements and other reports?

Business owners have a valuable resource in income statements and other financial reports. These tools offer crucial insights into a business’s financial health and can guide decision-making to foster growth. Income statements, for example, give a clear view of cash flow, offering a snapshot of profitability over time. Analyzing these statements allows business owners to grasp net income, a key measure of financial well-being. Paired with balance sheets and visual reports, income statements provide comprehensive insights into a business’s financial standing.

These reports are indispensable for tracking revenue, expenses, and profits. They help identify patterns and areas ripe for improvement. Access to current financial data allows business owners to make informed decisions rather than relying on guesswork. Ultimately, these insights enable entrepreneurs to manage resources effectively, spot growth opportunities, and steer their businesses toward success.

How can financial statements, including income statements, help small businesses understand their financial health?

Financial statements, particularly income statements, are crucial in providing small businesses with a comprehensive view of their financial well-being. By analyzing income statements, small business owners can gain insights into various aspects of their financial health. These statements detail important financial indicators such as sales revenue, cost of goods sold, gross profit, operating earnings, and net profit. Income statements offer a clear breakdown of the money flowing in and out of the business, enabling owners to gauge their profitability and track overall performance. Through these financial snapshots, businesses can identify trends, pinpoint areas for improvement, and make well-informed decisions based on precise financial data. Understanding and utilizing income statements can ultimately empower small businesses to optimize their financial strategies and enhance their overall financial health.

How Xendoo Can Help

Net income is critical for any individual or business’s financial health. The monthly income statement report details how effective the sales and operations process is at achieving financial success.

At Xendoo, generating up-to-date net income reports is one of the many bookkeeping and tax services you can access from our organization.

With Xendoo, you get a team of real people and bookkeepers who dedicate their skills and expertise to your business’s or individual finances’ success. Additionally, we integrate our services with the best software to ensure all your accounts are accurate. Get started today to meet your dedicated CPA team and expert bookkeeper.

Being a business owner comes with dozens of decisions, one of which is your accounting method. Although there are a handful of accounting methods, most business owners choose between two primary types: cash and accrual.

In this article, we’ll explore the main differences between cash and accrual basis accounting, helping you determine which method is right for your business.

What is Cash Basis Accounting?

Cash accounting recognizes revenue and expenses based on when cash is deposited or withdrawn from your bank account. This accounting method focuses on cash inflows and outflows, making it more straightforward for business owners just starting out.

Let’s say that you delivered a product to a customer on December 31, but don’t receive payment until January 2. If your year-end was December 31, the transaction would not be reported in income because the customer did not pay until the next year.

The simplicity of cash basis accounting makes recordkeeping easy for small businesses, closing out the year based on the bank statement. Furthermore, if your business is set up as a sole proprietorship or single-member LLC and you report all income or loss on Schedule C, you will use the cash basis of accounting.

What is Accrual Basis Accounting?

Accrual accounting is more complex, recognizing business transactions based on when contractual obligations are satisfied. To hold invoices and receivables not paid, accrual accounting uses accounts receivable and accounts payable accounts. Furthermore, the Financial Accounting Standards Board recently passed legislation that expanded revenue recognition under ASC 606. There are five steps to recognize revenue, including:

Identify the contract with a customer.

Identify each performance obligation, such as installation and ongoing support.

Determine the contract price.

Allocate the contract price to each performance obligation.

Recognize revenue once each performance obligation is satisfied.

Let’s say that you have a contract with a customer with $50,000 for delivery and $25,000 for ongoing support. Once you’ve delivered the product, you’ve completed the performance obligation, which results in the recognition of $50,000 of revenue, even if the customer has not paid yet.

Since accrual accounting doesn’t record transactions based on your bank account, there is usually more work involved for your accounting team. Especially with recent legislative changes, revenue recognition under accrual accounting is subject to more scrutiny.

Comparing Accrual vs Cash Basis Accounting

Accrual and cash basis accounting have some stark differences. Let’s break down these differences, giving you the information needed to decide which one fits your company.

Approved by GAAP

The cash basis of accounting is not a recognized method under Generally Accepted Accounting Principles. This means if you need to issue formal financial statements to your lender or investors, you will need to report on an accrual basis.

However, this doesn’t mean that you can’t use the cash basis of accounting for internal reporting purposes, but you will have more work to convert your financials over to accrual for formal reports.

Insights into Financial Health

Accrual accounting leads to more transparency in your accounting system. If you report under a strict cash basis of accounting, how will you know how much money customers owe you? What about the amounts you owe to vendors? Without tracking detailed schedules, like the accounts receivable and accounts payable aging reports, you can lose track of your cash flow.

Financial health insights are indispensable if your business is trying to grow or improve cash flow. In fact, over 80% of small businesses fail due to poor cash flow. Reporting with accrual accounting helps you better manage transactions in your checking account, promoting strong cash flow.

Required Reporting

Sometimes, you don’t have a choice in which accounting method you use. Schedule C filers are required to use the cash basis of accounting. In addition, c corporations, certain manufacturing businesses, and businesses with an average annual revenue of $25 million over a three-year period are required to use accrual accounting.

Furthermore, if your business is required to issue certified financial statements, such as through a compilation, review, or audit, you will need to use accrual accounting. This is common when you take out financing from investors and financial institutions.

Tax Reporting

Since accrual and cash accounting have different procedures for recognizing income and expenses, your taxable income can vary between the methods. The cash basis of accounting gives you more flexibility in the timing of revenue and expenses. For example, if you receive a large check from a customer on December 31, but it doesn’t clear until January 1, that income will be deferred until the next year.

With the accrual basis of accounting, the check would be reported in income, regardless of when it clears the bank. It’s important to note that both accounting methods will result in the same taxable income eventually. However, the timing of transactions will differ each year.

Choosing Your Method

Which method sounds right for your business? By default, most businesses start out using the cash basis of accounting. For Schedule C filers, the cash basis of accounting is non-negotiable. On the contrary, business returns select their accounting method on the first filed tax return. The default method is cash accounting. Double-check your business return to see what you are filing as.

Some business owners also choose to utilize a combination of both accounting methods, known as modified accrual. In this hybrid method, revenues are only recognized when they are measurable and available. For example, if it’s too hard to assign a price to each contractual obligation, you might decide to recognize revenue when the entire contract is complete. Expenses take a different approach, being recorded on an accrual basis of accounting since they are always measurable when they are incurred.

As your business begins to grow or you need to issue formal financial statements, switching to a full accrual basis of accounting might make more sense. To make the switch, you will need to file Form 3115 with your tax return. This will result in a change to your opening equity balance with either an income increase or reduction in the current year to convert your records over. Accounting method conversions can be complex, which is why it’s best to work with an expert throughout the process.

Getting Started

Whether you are looking for more information surrounding accounting methods or are ready to make the switch on your next tax return, reach out to Xendoo today. We can help you navigate converting your accounting records and reporting accurate tax returns, as we have the expertise to manage all three types of accounting methods

Whether you are looking for guidance on cash accounting, accrual accounting, or a combination of both, our team at Xendoo has you covered. Reach out today to schedule your free consultation.

Undoubtedly, part of owning a business is understanding that you may face high competition and crowded industries. Knowing how to make your business stand out and what sets it apart from the competition is vital to keep it from fading into the background. In other words, you need to know what sets your business apart to sell. And once you figure that out, you’ve got to shout it from the rooftops.

What Exactly is a Differentiator?

The basic definition of a differentiator is a unique set of benefits that sets your business apart from your competition. Understanding what you are good at and highlighting those qualities shows your customers why you are worth putting above your competition and spending more on your product.

Overall, differentiators validate your customers in their purchase, and a person who feels confident in their purchase is more likely to continue purchasing from you in the future.

Types of Differentiators

Though understanding what you’re good at may sound easy, it can be tricky to figure out.

Your company can have many types of differentiators. Some of the more popular differentiation factors are based on the customers’ experience, the price of your product, or even your specialization for a specific target market or industry. Pricing your services effectively can also be a powerful differentiator.

Say your company’s differentiator is the experience you give your customers and the personality of your business. If you go above and beyond to give your customers a great experience when they are shopping, they’ll remember it. In the best-case scenario, they will tell their friends about how friendly your employees are and how great of an experience they had.

Another example could be your expertise in serving a very specific target audience. Say you own a marketing agency that specializes in serving law firms. When a law firm looks for a marketing agency, it’ll appreciate finding one with lots of experience in its field.

Questions to Ask to Help Identify Your Differentiators?

Having trouble putting your finger on what makes your business special? Don’t worry. We have some simple tips and tricks that can help you.

Ask yourself what you do that your competition does not.

This is a chance to do market research and analyze how your competition works. Take a look at how they’re advertising themselves. What do they highlight most? What don’t they talk about? Next, list everything your business does that others aren’t talking about (or that you know they don’t do well). Then, write down a list of all the ways you overlap with your competition. Writing down your similarities and differences is a quick and simple exercise that can have long-term benefits and lead to a quick conclusion about your differentiators.

Ask yourself what your customers get from choosing your business. This is another way of saying you must be familiar with your customer’s experience.

Customer experience: The interaction between a business and a customer over their entire relationship.

Map out your company’s entire customer journey. What happens from the first time they hear about your brand through when they become happy, loyal customers? Putting yourself into your customer’s shoes shows you what they’re experiencing as they engage with your business and what benefits they see. From here, you can ask yourself:

What type of customers do you help?

What are your customers happiest about?

Still Having Trouble? Go Straight to the Source

Asking your loyal customers what benefits they get from your products or services may be the easiest way to determine your differentiators. Going straight to the source gives you a foolproof and immediate answer that helps you avoid making educated guesses.

You might ask them:

Did you meet their expectations?

Where did you exceed their expectations?

Why did they choose you over your competition?

What do they like about your business?

Got Your Differentiators? Now Brag About Them

Knowing how to use your key differentiators is just as important as determining them. Communicating these with your current and potential customers will help them understand how you will help them and what your business stands for. This starts by living and breathing your differentiators. Ensure everyone on your team knows what your business stands for and how you want to portray that through them.

The best part of understanding your differentiators is you can use them in your marketing strategy. A solid marketing plan will be useful when capitalizing on your company’s strengths. Highlight these differentiators when creating ads, posting on social media, and talking about your brand, which will let people know what you stand for and offer them. Also, a well-executed marketing strategy will give you a competitive advantage in your industry.

Overall, the real importance of differentiation in your business is to stand out and let your customers know what they are getting when using your product. Every few years, you must take a step back and reevaluate the importance and relevance of your company’s differentiators. They might change or stay the same, but keeping them core to your business can put you above your competition.

We share your passion for small businesses and are inspired by your dedication to making your dreams a reality. That’s why we’re committed to providing you with the financial visibility and support you need to thrive.

More Than Just Numbers

It’s more than simply crunching numbers. It’s about building meaningful relationships with our clients and understanding their needs. Our people-first mentality ensures you receive personalized attention and expert guidance throughout your financial journey.

A One-Stop Solution

Xendoo offers a comprehensive suite of services, including:

Full-service bookkeeping and accounting team to free up your time and resources.

Hassle-free tax preparation and filing

Fractional CFO Services to work with you on a roadmap of future growth

A dashboard that provides real-time financial insights

Passionate about your success?Xendoo is, too. We provide the financial visibility and support small businesses need to thrive and scale. Let us handle the financial burden so you can focus on what matters most – running your business and achieving your goals.

Contact Xendoo today and discover how we can give you time back to grow your business.

Getting funding for your startup business is one of the most important decisions you’ll make as a business owner. The type of startup funding you choose will have long-lasting impacts including:

How you structure your business and file taxes

What percentage of ownership or equity you and your investors get

How much profit your business generates and how much you keep

Startup funding can cover the initial costs of setting up and running a company. It can also help you continue to grow years after you’ve launched.

Most startups seek funding to help them reach their goals faster. For example, you might need startup funding to:

Buy or repair equipment

Hire additional employees

Expand your business into new markets

Invest in new projects or products

This article will dive into funding for startups of all sizes and stages and provide guidance on choosing the best option for you.

Types of startup business funding

The type of startup funding you choose should align with your goals and strategies. There are three primary types of funding for startup businesses:

Self-funding

Loans

Investors

Let’s look at the types of funding for startups in more detail to help you decide which fits your needs.

1. Self-funding

Self-funding, also called bootstrapping, is when you use personal funds and savings or borrow money from friends and family to fund your startup.

Unlike other options on this list, self-funding usually comes with fewer risks. You don’t have to worry about paying off high-interest loans or giving up control to outside investors. Without investors, you retain control over how you run your business and its future direction.

You also retain all the profits and debts. So, if your business fails, you could end up losing your personal savings. Many startups begin with bootstrapping but eventually need to raise funds to support their growth. Additionally, if your business model has high startup costs, it’s more difficult and risky to fund on your own.

For example, businesses in the food and accommodation industries have the third-highest startup costs on average. Large-scale restaurants, breweries, casinos, and hotels generally need additional funding for real estate, equipment, and labor.

2. Small business loans

A small business loan is a form of debt financing. You borrow money from banks and other lending institutions. Like self-funding, you retain ownership of your startup business.

However, there are risks with this type of startup funding. As with any other loan, a small business loan comes with interest rates.

Interest rates can strain your finances if they too are high. Additionally, a small business loan requires regular monthly repayments, which can impact your cash flow.

There are several types of loans for small businesses and startups. Also, business loans have various requirements that often include personal and business credit scores. If you’re borrowing higher amounts (over $50,000), you may need to show:

Annual revenue and cash flow

Years in business (some require two years minimum)

Business plan

Financial statements (balance, profit and loss, etc.)

Types of business loans

Traditional business loans

Banks and other financial institutions offer business loans of varying amounts and interest rates. They also have specific requirements you must meet to be eligible.

Microloans

Smaller loans less than $50,000. Six years is the maximum time to repay an SBA microloan. Interest rates are usually between 8% to 13%.

Small Business Administration (SBA) loans

The most common are the 7(a) loans or general-purpose loans. SBA’s 504 loans are for purchasing fixed assets like real estate and equipment.

Lines of credit (LOC)

Flexible loans you draw from when you need capital—you pay interest only on the amount you use.

3. Grants

Small business grants are free money given to individuals, businesses, and non-profits. Unlike loans, you don’t have to repay them.

Grants are one of the best sources of funding for startups. However, they come with specific conditions and requirements.

Startups must align with certain goals and objectives, such as advancing a particular industry or contributing to community development. Additionally, applying for grants can be lengthy and time-consuming. They often require a solid business plan, detailed financial projections, and rigorous documentation.

Nonetheless, they’re particularly beneficial during the initial stages, especially if other funding options aren’t available or are too risky.

Government agencies, corporations, and entrepreneurship organizations provide thousands of grants. You can search for federal grants on the website: Grants.gov. There are specialized grants for women, veterans, and minorities. Other resources to search for business grants include:

Crowdfunding is when you raise capital from a large pool of individuals. Primarily, business owners crowdfund through online platforms like Kickstarter or Indiegogo.

It’s particularly useful when your startup has a compelling story or mission that people can connect with emotionally.

There are several types of crowdfunding, including donation, rewards-based, debt, and equity. Rewards-based crowdfunding is the most common, and what you see on Kickstarter. Equity crowdfunding is regulated. Platforms like Republic and WeFunder help founders raise money, but there is a rigorous application process. Entrepreneurs may also need to present finances and pitch.

The type you do will impact your company and crowdfunding platforms usually take a percentage of the funds you raise.

Types of crowdfunding

Type

What it means

Donation

Individuals give money with no strings attached

Rewards-based

You give supporters certain rewards like the product or service you’re launching in exchange for their funds.

Equity

When you raise capital from individual investors for a private business in exchange for unlisted shares (equity).

Debt

Also called peer-to-peer lending, debt crowdfunding is when individuals loan money in exchange for repayment with interest.

5. Angel investors

An angel investor is a high-net-worth individual who provides startup funds or working capital, usually in exchange for equity or convertible debt. Angel investment usually provides funding when your startup is too new or risky to attract venture capital. Angel investors are typically willing to take on more risk than traditional lenders.

These individual investors invest in the potential of the startup founder and business, with the understanding that many startups fail, but the few companies that succeed offer significant returns.

6. Venture capitalists

Individual venture capitalists (VC) or firms fund startups that have high-growth potential in exchange for an ownership or equity stake. Like any funding method, venture capital has advantages and disadvantages.

VCs bring more than money to the table. Ideally, they’ll have extensive experience in your industry. They may provide valuable advice and connections that help you run and grow your startup.

You’ll share a percentage of your profits and potentially lose some control over business decisions.

Additionally, venture capital firms may expect high investment returns within a relatively short timeframe. Partnering with the wrong VCs can pressure your startup to grow rapidly and prioritize short-term gains over long-term stability.

Venture capitalists typically invest in a business during the early stages (Series A and B funding rounds). Investing in early-stage companies may be riskier, but if a business succeeds, the return on investment can pay off.

7. Startup funding rounds

Startup funding rounds are stages in the lifecycle of a startup where you raise capital from external investors. These rounds provide the financial fuel to help your startup grow and move toward profitability.

Here’s a brief overview of what each round entails:

Startup funding round

What it is

Median amount

Pre-seed

The earliest stage of informal funding when you pool funds from your own savings or from friends and family. You may use these funds to do market research and develop your product.

Not available

Seed funding

Seed funding helps you get your business off the ground. It’s the first official stage of funding. You may get funding from angel investors or close friends and family in exchange for convertible debt or a percentage of ownership (ideally less than 10%) of your company.

$2.3 million

Series A

This is the first major series of external, equity-based funding for a startup. Usually, your business will have traction and a proven business model or demand.

$12 million

Series B

At this stage, you have a well-established product and a significant user base. The funding you get is for business development, increasing market share, and achieving broader market expansion.

$25 million

Series C (and beyond)

Rounds are for if your business is already successful and wants to expand, innovate with new products, or acquire other businesses. Series C and further funding rounds often involve private equity firms, hedge funds, and other institutional investors.

Incubators and accelerators are programs that support startups. They differ based on the stage of the startup and the type of support they offer.

Incubator programs support companies at the earliest stages. They help you develop your idea by providing resources such as office space, legal guidance, and access to a network of industry professionals.

Accelerators support more established companies looking to scale up quickly. These programs are usually time-limited. They run for a few months, during which startups receive intense mentoring, education, and networking opportunities.

Often startup incubators and accelerators are used interchangeably.

Keep in mind that these have a rigorous application process that includes financial projections and pitches.

What you need to know before getting startup funding

Before you embark on the journey of securing startup business funding, there are several factors you need to consider:

Understand your business needs: You should know how much funding you need and what you will use it for. This includes knowing your operational costs, projected growth, and future financial needs. Working with an accounting service or virtual CFO with startup experience can help. They’ll be able to pull together many of the necessary financial documents.

Evaluate funding options: Before moving ahead with startup funding, you must first understand the pros and cons. Funding has lasting impacts on the future of your business so it’s not a decision to take lightly.

Prepare a business plan: A comprehensive business plan is a requirement for some types of startup funding. It should include details about your business model, market analysis, sales and marketing strategies, and financial projections.

Get support for startup funding

Securing startup funding is a pivotal process that can significantly influence the trajectory of your business. Seeking professional advice is not just recommended—it’s essential.

Xendoo can give your startup the financial expertise and support it needs during the funding process.

We provide CFO services, bookkeeping, accounting, and tax preparation for growing businesses. With a team of financial experts in your corner, it’s easier to provide a clear and accurate picture of your finances for potential funding. Investors and lenders will expect to see balance sheets, income statements, and more. A bookkeeper or accountant will help you prepare with organized, accurate financials.

Need a bookkeeper, accountant, or CPA? Schedule a call to learn more about how Xendoo can help your business, whether you’re funding a startup or need ongoing bookkeeping and accounting.

FAQs

How much do you need to fund a startup?

How much funding your startup needs varies based on your industry and business model. However, successful startups generally need between a few thousand dollars to millions for the first year. Create a detailed business plan to estimate your specific needs accurately.

This post is intended to be used for informational purposes only and does not constitute as legal, business, or tax advice. Please consult your attorney, business advisor, or tax advisor with respect to matters referenced in our content. Xendoo assumes no liability for any actions taken in reliance upon the information contained herein.

The biggest rule of thumb when running a company is to keep your personal and business finances separate. To do that, you need to choose the best business bank for you, which may not be the same one you use for your personal finances.

Business bank accounts have different terms and benefits than personal accounts. As an online accounting service, Xendoo works with many companies and business banking services.

The best business bank for you depends on your particular needs. But there’s much more to consider. Some banks are stronger in commercial lending, while others have stronger lines of credit.

We’ll compare the best business banks and their features to help you decide which options are right for you. Review each bank’s rates and services to determine which suits your needs.

Wells Fargo

Chase

Bank of America

Mercury (for global and online-specific companies)

Citibank

Capital One

PNC

US Bank

TD Bank

Cogent Bank (or similar regional banks)

How to choose a bank for your business

Choosing a bank is a big decision in your business journey. However, there’s no one-size-fits-all business banking solution. Factors like your monthly revenue, number of cash payments, and company structure (LLC, S corp, C corp, etc.) will influence which features you need most. You may also want to get startup funding or a loan from the same place you do your banking.

Although these factors may vary, there are some criteria all companies should look at when choosing a banking partner. Here are the features we looked at to evaluate the best business banks.

View-only access, wires, and online banking

As a baseline, all business banks must have robust technology to support VOA (view-only access), wires, and online statements. You can share view-only access to your bank statements with bookkeepers, accountants, and other trusted financial partners. They’ll only be able to view, not make changes to, the data they need to record and manage your finances.

Fees and costs

Some banking services come with fees and financial requirements that might not be obvious at first. Common banking fees include:

Transaction limits and fees

Monthly account maintenance fees

Deposit limits and fees

Opt for a bank that provides transparency in its fee structure and offers the best value.

Annual Percentage Yield (APY)

In simple terms, APY is how much an account can earn in a year through interest. However, it’s not the same as interest rate because it also includes compound interest.

For example, let’s say you open an account with 1% APY and your first deposit or principal balance is $20,000. Then, every month you deposit another $20,000. Instead of only earning interest on the original amount, compounding interest factors in the updated account balance.

In-person locations

If you run an online business and rarely have cash transactions, a bank with in-person locations might not be a priority for you. Instead, it might be more convenient to look for online banking solutions.

If you have cash transactions, which is common with franchises, retail stores, and restaurants, physical bank locations are more important. You might need to make frequent cash deposits and prefer in-person service.

10 Best business banks

Whether you’re considering switching banks or starting a business checking account for the first time, you can compare features, fees, and more below.

1. Wells Fargo

Best for: Companies that want loans, business checking, and in-person banking.

Wells Fargo is one of the oldest banks in the United States. However, its reputation has taken some hits in recent years. But, that also means that it is under heavy scrutiny from regulators and is focused on regaining consumer trust.

Monthly fee: $10-$75 per month

Minimum deposit requirement: $25

Transaction limit: 100-250 monthly

Deposits: $5,000-$20,000 fee-free cash deposits

APY: None

Member FDIC: Yes

ATMs: Over 12,000 ATMs in 40 states

Overall, Wells Fargo has a huge physical presence, which might be a fit if you value in-person banking. But, its past actions and high fees for overdrafts, transactions, maintenance, and more make it less than ideal.

Pros

Cons

Physical locations in over 40 states

High monthly fees and other costs

You can open an account online

No free checking accounts

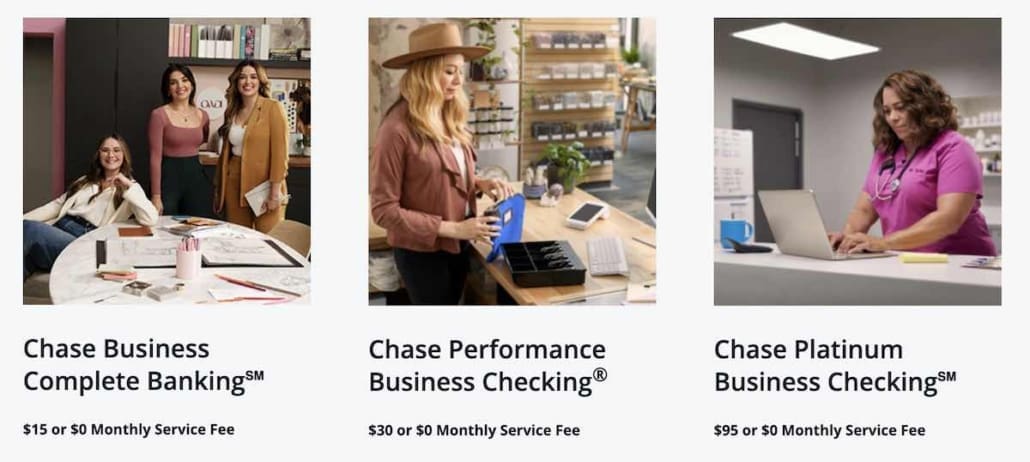

2. Chase

Best for: Companies of all sizes that want a wide range of business and personal financial services (checking, savings, financing, mortgage, etc.)

Chase offers many types of business banking accounts to suit different business sizes and needs. Let’s take a closer look at each in the comparison below.

Business Complete Banking

Performance Business Checking

Platinum Business Checking

Monthly fee

$15 (waived with $2,000 minimum balance)

$30 (waived with a $35,000 minimum average balance)

$95 (waived with a $100,000 minimum average balance)

Chase has locations in over 29 states and over 16,000 ATMs. It might be convenient if you need in-person banking and already have a personal banking account.

If you have a lot of monthly transactions or don’t want to worry about banking fees, then Chase isn’t the best business bank for you.

Pros

Cons

Multiple checking account options to suit different business needs

Monthly fees, but they are waived if you meet the account balance threshold

Wide network of branches for in-person service

No APY for business checking

3. Bank of America

Best for: Businesses that have large, monthly cash deposits and need in-person services.

Bank of America has two business banking accounts: Fundamentals and Relationship. The Fundamentals account is more suitable for small-to-medium businesses while Relationship is for larger enterprises.

Each account has various fees and requirements. Here’s the breakdown for the Fundamentals account:

Monthly fee: $16 (waived with $5,000 monthly account balance)

Minimum deposit requirement: $100

Transaction limit: 200 per month

Deposits: Free up to $7,500 and a .30 charge per $100 over

APY: Not available

Member FDIC: Yes

ATMs: Over 4,500 locations and ATMs

Pros

Cons

One of the largest and most established banks

Complicated monthly fees and requirements can mean more expensive banking costs

Branches and ATMs all over the country for in-person banking and cash deposits

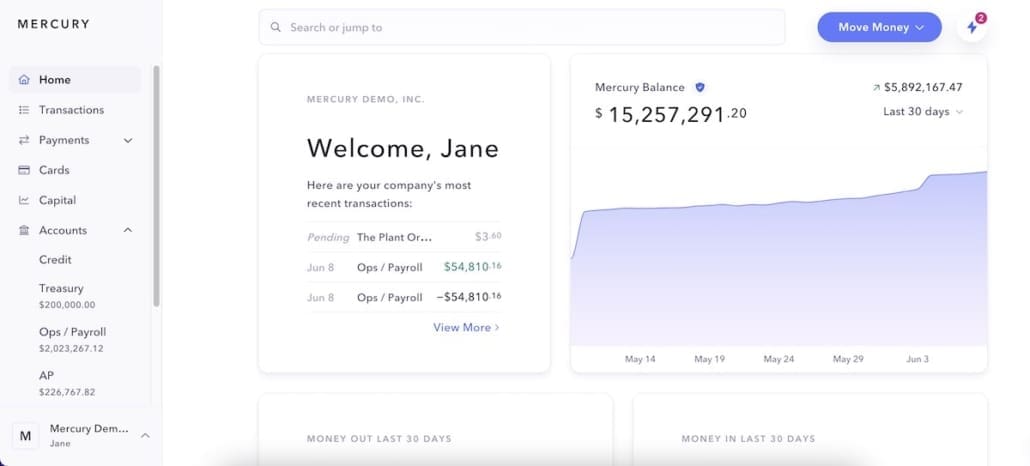

4. Mercury

Best for: Growing global and online-only startup businesses.

One of the reasons why Xendoo partners with Mercury is that it’s tech-enabled banking at its finest. Compared to traditional banking platforms, it has an incredibly, user-friendly interface.

It has an API, so businesses can integrate other financial tools and services they use. For example, you can connect bookkeeping, payments, payroll, and more to your Mercury business banking account. This way, it’s easier to keep track of and manage your finances.

It also has Mercury Raise, a program that helps connect startups with investor funding.

You can sign up for a business banking account in 10 minutes.

They also have a non-traditional approach to business loans with Mercury Venture Debt. If your startup has raised venture capital (VC) funds in the past year, you could be eligible. Instead of looking at cash flow and other financial indicators, it looks at your investment team.

Monthly fee: $0

Minimum deposit requirement: $0

Transaction limit: Unlimited, including savings account

Deposits: Unlimited

APY: Up to 5.10% yield with Mercury Treasury (as of writing)

Member FDIC: Yes (up to $5 million)

ATMs: Not available

Pros

Cons

Free checking and savings accounts

No cash deposits

Helps startups with funding through Mercury Raise and its Venture Debt loan program.

It doesn’t accept some businesses (i.e. cannabis or businesses with many cash transactions)

No overdraft fees

You can connect bookkeeping, accounting, payments, and other tools

5. Citibank

Best for: Businesses that maintain a high monthly balance to avoid fees.

Citibank has also been around for a long time, so it has all the basic business accounts and some extras. It has several options for business checking accounts as well as savings accounts, credit cards, loans, and more.

However, it doesn’t have a free checking option. There are monthly fees unless you maintain an average monthly balance over $5,000 to $10,000, depending on the account you use.

Monthly fee: $15-$30

Minimum deposit requirement: $1

Transaction limit: Limited free transactions (250-500 depending on the account)

Deposits: $5,000-$2,000 free cash deposit limit

APY: Not available

Member FDIC: Yes

ATMs: 2,300 ATMs

Pros

Cons

Full suite of business services

All business checking accounts have fees (some are waived with a monthly balance)

Must open an account in-person at a local branch

6. Capital One

Best for: Small businesses that want to build credit and make many purchases with a credit card.