Top 7 Requirements to Secure Ecommerce Funding (Hint: They’re Not What You Think)

In the past, online sellers often had to dig into their own pockets to fund their eCommerce business dreams.

Since small or growing businesses are technically high-risk investments, banks and other financial institutions were reluctant to part with their cash to help eCommerce sellers.

But times have changed.

Today, there is a growing number of funding options eCommerce entrepreneurs can tap into to make even their biggest, hairiest goals reality. Great news, given that 9.5% of businesses without financial capital say it negatively impacts their profitability.

Yet, many eCommerce sellers are stuck in their ways, seeking capital from red tape-heavy banks or going without any funding support at all. In fact, a staggering 50% of UK SMEs don’t look beyond traditional funders—and the tunnel vision can definitely cost them.

The good news? It doesn’t have to be this way.

To prepare you to face your next funding application with confidence, let’s jump into some of the requirements you’ll need.

Ready for a flexible funding solution? Learn more about how we help eCommerce owners improve their cash flow.

Secure ECommerce Funding the Simple Way

- How to Fund an Ecommerce Business: Know Your Options

- What Do I Need to Secure Ecommerce Funding?

1. Proof your business is on the right track

2. Know what eCommerce funding you need (and what for)

3. Showcase your good moral character

4. Get your paperwork in order

5. Show off a little

6. Clean up your credit, stash away cash, and get collateral (but not for the reasons you think)

7. Be mentally prepared to move on

- The Blueprint for Getting Your Ecommerce Business Funded

How to Fund an Ecommerce Business: Know Your Options

Ecommerce funding has come a long way since its inception, and there is now a potential capital source to suit every business size and budget.

Here’s a quick rundown of the most common eCommerce funding options:

- Working capital: The seller receives funding to cover gaps in cash flow for day-to-day business expenses like shipping costs, supplies and utilities, or invest in a new product line, ad campaign or additional inventory for peak sales seasons.

- Cash advances: The seller receives a lump sum and agrees to pay a percentage of their monthly turnover to the lender until the advance is paid in full—note: cash advances aren’t loans.

- Invoice factoring: The business owner sells their accounts receivables (due invoices) to a factoring company at a discount with fees added on top. The factoring company then releases the funds to them.

- Crowdfunding: The entrepreneur pitches their idea on a dedicated online platform to the masses, and individuals can choose to invest. There are three kinds of crowdfunding: debt, donation, and equity crowdfunding.

- Peer-to-peer lending: Usually facilitated through an online platform, the individual receives funding from a person instead of a financial institution.

- Angel investing: The business owner sells a stake in their business to a high-net-worth individual in return for capital.

Are you struggling to decide between cash advances and working capital loans? We can help.

What Do I Need to Secure Ecommerce Funding?

Thanks to the flexibility of some of the newer, more modern funding options, today’s funding requirements for growing eCommerce businesses tend to be much more flexible than those of traditional funders.

While most alternative eCommerce funders won’t throw out your application for lacking things like management expertise, collateral, or credit, there are some standards you’ll have to meet.

Let’s break these down:

1. Proof your business is on the right track

Alternative funding providers are all about businesses with results that prove they’ve got a promising future.

No matter who you acquire eCommerce funding from, there’s one thing your provider will want to know: that they’ll get their money back plus a fair return.

While you don’t have to be the next overnight Amazon sensation to prove your worth, you must show you’re a viable business and a low-risk investment.

Here are some things you can provide to show your business is worth the investment:

- Calculations that demonstrate your business has a high ROI, net operating income, and Debt Service Coverage Ratio (DSCR). (More on this in a minute 😉).

- Documents proving your business consistently turns a profit.

- Store reports showing sales volume and minimal product returns.

- Statements demonstrating you have sufficient liquidity to repay a loan, plus its interest and charges.

- Records showing you’ve been in operation for at least 12 months.

If you meet these requirements, securing funding becomes a win-win situation for everyone, and you’ll have better chances of getting approved.

Looking for a faster solution? Find out how you can pre-qualify for up to $1,000,000 in less than 5 minutes.

2. Know what eCommerce funding you need (and why you need it)

By the time you’re ready to start sending applications to prospective funding providers, you should have concrete answers to these things:

- Your reason(s) for applying for external funding.

- The intended purpose of the cash injection.

- How much capital you need.

Not only will this help narrow down the type of funding you need (and suitable providers), it’ll also show you’ve done your due diligence.

Taking on funding is no child’s play, and mistakes in this area can cost you. Funding providers want to know you understand the risks involved and are prepared to take on this commitment.

Here’s how to show eCommerce funders you’re ready, step-by-step:

- Create a documented breakdown of the capital amount you need for each task (adjusted with a buffer for unplanned bills).

- Work out your return on investment (ROI). Are you making enough returns to make funding feasible? Note long term debt reduces ROI.

- Analyse your net profit income. How healthy is it? Will you have enough liquidity in your business to operate once you start to repay successfully?

- Assess whether any existing debts will inhibit you from making repayments. Calculate your Debt Service Coverage Ratio (DSCR) to help you with this task.

These are the three equations you’ll need:

1. ROI % = (Net profit) / Cost Of Goods Sold (COGS) * 100

I.e. $20,000 / $10,000 *100 = 200%

2. Net Operating Income = Revenue – Cost of Goods Sold (COGS) – Operating Expenses

I.e. $50,000 – $20,000 – $10,000 = $20,000

3. Debt Service Coverage Ratio (DSCR) = Net Operating Income / Annual Debt Obligation

Not a fan of calculations? Try this DSCR calculator.

And, there you have it! A summary of your most important figures that prove your eCommerce business is good to go.

💡 Top tip: For best results, submit funding applications during peak seasons. When your sales volume spikes, you’ll be able to cover the repayments with plenty left over. This extra wiggle room helps funders feel more comfortable funding your business, and removes the stress of worrying about repayments.

3. Showcase your good moral character

Most traditional funders will expect you to show good moral character—but some of the newer funding providers take a fresh angle on what this actually means.

Here’s what a funding provider might look for:

- Overdue bills: Zero overdue bills (like student loans or credit card debt).

- Missed payments: If you’ve gone rogue on payments to another funder, a credit check will reveal this to your prospective funder.

Note: If you have slipped on paying existing debts, don’t beat yourself up. According to Experian, US credit card debt stood at $756 billion. It’s a problem for many. Take active steps to get back on track with your payments and reduce your debt balance before applying for additional funding.

- Get your paperwork in order

It may seem like an old-school requirement, but being organized can pay off big time in your eCommerce funding journey.

Not only can getting your ducks in a row make the application process go smoother and faster, it may also earn you brownie points with the people reviewing your application.

As the saying goes, ‘how you do one thing is how you do everything’.

Remember, despite your funder being a financial institution or VIP, you’re still dealing with people—so first impressions count.

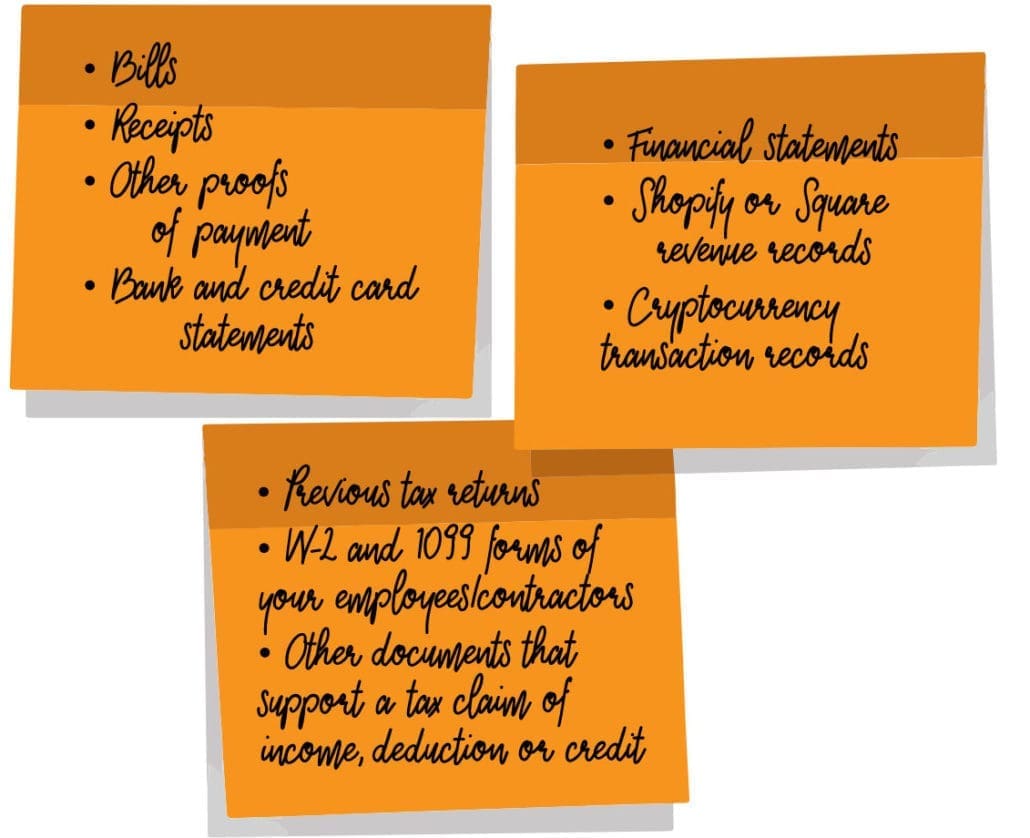

Here are the docs you’ll need to prepare as standard:

- Proof of address

- Articles of Association (and the names of directors and associated persons)

- Company bank statements

- Financial accounts, i.e., Income Statements, Profit and Loss statements

- Financial projections

- VAT returns/ Tax returns

- Business plan

- Show off a little

To stand out, you need to get comfortable with a pinch of humble bragging. Opportunities to show off about your business only come around rarely, so when they do, grab it with both hands.

For example:

- Do you have a business degree or business-related qualification(s)?

- Have you worked in retail, sales, or management for X amount of years?

- Is your team excellent at drumming up funds through pre-launches?

These details will let potential funders know you care about success and are willing to invest in yourself to excel.

- Clean up your credit, stash away cash, and get collateral (but not for the reasons you think)

An increasing number of funding providers are choosing to overlook bad credit or a lack of assets at first glance—but there’s often a catch, and if you’re not careful you might end up with crappy interest rates, terms, or fees.

Having good credit, savings, and assets will put you in a better position to choose funding types and providers as well as negotiate terms. Plus, it’ll demonstrate to your potential funding providers that you:

- Are in a stable financial position.

- Have an alternative source of funding and aren’t in dire straits (desperation is never a good look).

- Have a concrete backup plan should things take a turn for the worst.

Now you know why it pays to clean up your credit, here’s a game plan to go ahead and straighten up your finances:

- Start your credit-building journey by getting yourself and your business a credit card to build credit history and pay off existing debts. The debt avalanche and snowball methods are the most commonly used systems for clearing debt fast.

- Analyze your progress through a credit score tracker.

- Build a saving pot for your business by putting away a slice of your profits into a business saving account. Treat it like a bill you must pay no matter what.

- Finally, work on securing assets for your business, like better equipment and storage units. They’ll impress funding providers and help you optimize the running of your business.

- If you hit any road bumps, motivate yourself by picturing how impressive you’ll look to prospective funders with savings and good credit. 💪

- Be mentally prepared to move on

Having the relevant paperwork, collateral, and credit is essential—but it’s only part of the story to secure eCommerce funding.

So what’s missing? Resilience.

You’ll likely hear a lot of no’s on your journey, so be prepared to pick yourself up, keep your goal in sight, and move on to the next.

Compared to traditional loans, eCommerce funding is still a new game—that means funding providers are continuously adapting their rules and approaches, and many are yet to catch up with eCommerce’s speed.

Does this make life as an eCommerce owner more complex? You bet.

But don’t forget you have a ton of options that give you the advantage. If you’ve tried to secure funding through traditional avenues before, and it’s just not working—move on.

Your dream funding option is out there, and your perseverance will pay off. After all, only 20% of US-based small businesses don’t use external funding.

The Blueprint for Getting Your Ecommerce Business Funded

Thanks to a sharp rise in alternative modern solutions, business leaders can now overcome traditional funding requirements and opt for more flexible terms.

But you aren’t entirely off the hook. 🎣

Today, eCommerce funding is a whole new ballgame with a new set of requirements to fulfill.

So, learn what you need to get approved by each, then execute with precision. Who knows, you may end up with more funding options that you know what to do with!

At Sellers Funding, our application process focuses firmly on sales performance, not credit history or collateral. If you’re not sure which funding option is right for your business, we can help.