With the qualified business income deduction (QBI), small business owners and self-employed workers could deduct up to 20% of their taxable income.

The QBI deduction is only available to pass-through entities between the tax years 2018-2025. A pass-through entity is a business that doesn’t need to file a separate business tax return. Instead, the owners report business income on their personal income tax returns.

Pass-through entities include:

Sole proprietorships

Partnerships

LLCs

S-Corps

In some cases, certain trusts and estates may also qualify. As a pass-through entity, business owners pay taxes for their business on their personal tax returns.

If your business is a pass-through entity, you may be able to lower your taxable income with the 20% QBI deduction.

This post will cover everything businesses need to know about the qualified business income deduction—including how to claim it.

What is the qualified business income deduction?

The qualified business income deduction (QBI) is part of the Tax Cuts and Jobs Act (TCJA) of 2017. With the deduction, non-corporate taxpayers (pass-through businesses) can deduct 20% of their qualified business income.

Since it’s a deduction, it will lower your taxable income, which might mean that you get taxed at a lower rate. In other words, you could pay less in taxes if you qualify.

Who qualifies for the QBI deduction?

To qualify for the QBI deduction, you must have income from a pass-through entity.

There are some exceptions and income limits, especially if your business is an SSTB—a specific service trade or business.

SSTBs

If your company’s main asset is your skill or reputation, or that of your employees, then your business is an SSTB. Some common SSTB industries include:

Health

Law

Accounting

Art and design

Consulting

Financial services

Investment management

SSTBs can’t claim any QBI deduction once they reach the highest income limit. If your business isn’t an SSTB, you can claim a full or partial deduction. REIT/PTP dividends also qualify for the QBI deduction.

REIT and PTPs

If you have dividends from a Real Estate Investment Trust (REIT) or a Publicly Traded Partnership (PTP), you could deduct 20% of that income too. You must hold the dividends for more than 45 days to qualify.

If you have qualified business income and dividends, you can deduct 20% of your taxable income from each. As long as your total QBI deduction falls under 20% of your taxable income, you can take advantage of the stackable deductions.

Taxable income limits

The rules get complex once your taxable income hits the QBI limit. You may qualify for a partial deduction, depending on your total taxable income and your business.

Your filing status is the main factor that determines your income limits. Joint filers have one set of numbers, while all other filers have their own range.

QBI (full deduction)

To qualify for the full 20% deduction, your taxable income must be under $340,100 if you’re filing jointly.

If you’re filing single, head of household, or something else, your taxable income must be under $170,050.

Filing Status

2022 Taxable Income

QBI

SSTB

Joint

Up to $340,100

20%

20%

All others

Up to $170,050

20%

20%

QBI (partial deduction)

If your joint taxable income is between $340,100 and $440,100, you’re eligible for a partial QBI deduction.

For those that aren’t filing jointly, your income needs to fall between $170,050 and $220,050 to qualify for a partial deduction.

Filing Status

2022 Taxable Income

QBI

SSTB

Joint

Up to $440,100

Partial

0%

All others

Up to $220,050

Partial

0%

Once you pass the taxable income limits above, you’ll need to do a little bit of math to find your deduction amount.

You’ll choose the higher deduction out of the two options below:

50% of the W-2 wages paid by your business

25% of the W-2 wages and 2.5% of property

For a property to qualify, you must still be able to claim it as a depreciation expense, so its value is spread out over many years.

Property that qualifies is usually under 10 years old. For real estate, the depreciation life is between 27 and 39 years, depending on if it’s residential or commercial.

2023 QBI taxable income limits

Hopefully, you’ve filed your tax return and claimed the QBI deduction for the 2022 tax year. If not, it’s good to plan ahead for next year. For 2023, you can find the taxable income limits using the charts below.

Filing Status

2023 Taxable Income

QBI

SSTB

Joint

Up to $364,200

20%

20%

Joint

Up to $464,200

Partial

0%

All others

Up to $182,100

20%

20%

All others

Up to $232,100

Partial

0%

Filing Status

2023 Taxable Income

Option 1

Option 2

Joint

Over $464,200

50% W2 wages

25% W2 wages + 2.5% qualified property

All others

Over $232,100

50% W2 wages

25% W2 wages + 2.5% qualified property

QBI deduction example

To simplify the QBI deduction process, let’s look at some examples.

Say you’re a sole proprietor with a single filing status. In 2022 you earned:

$100,000 from your independent contract work

$50,000 in REIT dividends

If this is your total taxable income, you qualify for the full 20% deduction.

But what if your sole proprietorship is a small piece of your portfolio? Take the following scenario instead and say you have:

Total taxable income is $400,000

Paid $40,000 in W2 wages

Qualified property worth $300,000

In this case, you won’t qualify for the full 20% deduction.

Even though your pass-through income is under $170,050, your total taxable income is well over the highest limit. You’ll need to do some simple math to find your deduction amount and decide which partial deduction will save you the most.

50% partial QBI deduction

First, multiply the wages you paid by 50%. This will give you your first deduction amount.

$40,000 x 0.5 = $20,000

25% partial QBI deduction

Next, follow the three steps below to calculate your second amount.

Take the wages you paid and multiply it by 25% – $40,000 x 0.25 = $10,000

Multiply your qualified property value by 2.5% – $300,000 x .025 = $7,500

Combine the two numbers – $10,000 + $7,500 = $17,500

In this case, the 50% partial deduction is higher, so it’s the better option.

How to claim the QBI deduction

You may not have the time or desire to figure out eligibility requirements, gather and fill the required documents, and submit your forms to the IRS by the deadlines.

If you think you qualify for the QBI deduction, these steps will simplify and maximize your small business tax deductions.

1. Leverage CPA services

The easiest way for small business owners to maximize their QBI deduction and other tax credits is to work with a tax CPA. Professional financial services like Xendoo help small business owners get the best deductions. We also have in-house bookkeepers and CPAs to file your taxes without sharing your information with third-party services.

If you’d like to know the overall process to claim a QBI deduction, you can read through the simplified steps below.

2. Calculate taxable income

Your CPA will calculate your taxable income for the year. Your taxable income is all your combined income, minus deductions based on your business activity and expenses.

3. Determine if you’re eligible

Once you’ve calculated your taxable income for the year, you’ll know whether you’re eligible for the QBI or not.

If you’re filing jointly in 2022 and your income is under $340,100, you’re eligible for the full 20% deduction. All other filers are eligible for the full deduction when taxable income is under $170,050.

Even if your income is above the limit, you might qualify for a partial tax deduction.

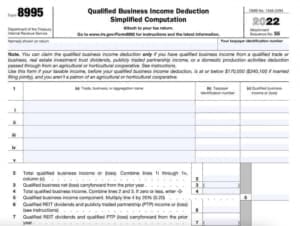

4. File Form 8895 or 8895-A

If you’re eligible for a full or partial deduction, you’ll need to file the correct form. There are two forms, and the one you’ll file depends on if you get a full or partial deduction.

Both forms come with worksheets to help you find your exact QBI deduction amount. However, it will take some time and math on your part.

If you missed the tax deadline but filed an extension, you can still claim the QBI deduction. To get caught up and take advantage of all the tax breaks, many businesses consult catch up bookkeeping experts and CPAs.

Xendoo does business taxes, bookkeeping, and accounting under one roof. To learn more about Xendoo’s services and how they can help you manage all your business finances (and save money in the long run), schedule a call today.

This post is intended to be used for informational purposes only and does not constitute as legal, business, or tax advice. Please consult your attorney, business advisor, or tax advisor with respect to matters referenced in our content. Xendoo assumes no liability for any actions taken in reliance upon the information contained herein.

If you’re wondering how to pay less in taxes, you’re not alone. Everyone—from individuals to business owners—wants to know how to lower their taxes.

Tax laws are complicated and they can change each year. Our tax accountants know all the tax breaks for business owners and how to leverage them. With some guidance, you can legally reduce your tax liability and avoid paying more than you owe.

In this guide, we’ll go over how to lower taxable income and keep more of your profits while staying on the right side of the IRS. We’ll also share 12 tax-saving strategies, including a detailed explanation of each and how to determine if you qualify.

Business owners are responsible for filing taxes for their personal income as well as business income. You can file these together or separately, depending on what type of business you own.

For example, if you own a C corporation, you’ll file business and personal taxes separately. However, if you run an LLC not taxed as a corporation, you’ll pay taxes as a pass-through entity.

To differentiate:

The IRS taxes a regular corporation—or C corporation—as a separate entity. The corporation uses Form 1120 to report income and claim credits and deductions each year.

A pass-through entity doesn’t file taxes as a separate entity. Instead, the income “passes through” to the owner of the business who pays personal income taxes on their share of the business.

The majority (95%) of businesses are pass-through entities. Below, we’ll cover how you can pay less in taxes on your business and personal income as a pass-through entity.

How much do Americans pay in taxes?

You pay taxes as a percentage of your income. There are seven tax brackets in the US tax code, ranging from 10% to 37%. Everyone’s tax situation is different.

There’s no one average tax bill, but the latest reports claim the average income tax payment in 2020 was $16,615. Thankfully, this amount isn’t paid all at once. Business owners pay estimated taxes quarterly, while employees pay a portion with every paycheck.

It’s worth noting, however, that most people don’t pay that much. In 2020, Americans in the most common tax bracket—incomes between $50,000 and $75,000—paid an average of $4,567 in income tax.

You pay a higher percentage of your income in taxes as your adjusted gross income (AGI) increases. Your AGI is the amount of your income that’s taxable after you subtract credits and deductions.

You can drastically reduce your tax bill by taking advantage of all your business tax credits and deductions.

What is taxable income?

Taxable income is the amount of income that the IRS uses to calculate how much you owe in taxes each year. It includes earned income from your business or wages from a job. Also, it includes unearned income, such as interest from investments. Some important concepts to keep in mind regarding taxable income:

Tax deductions lower your taxable income, which can land you in a lower tax bracket. If your taxable income drops to a lower tax bracket, the IRS could tax you at a lower rate.

Revenue – deductions = taxable income

Tax credits reduce your tax bill dollar for dollar. If your tax liability is $2,000, but you qualify for a $1,000 tax credit, you’ll only owe $1,000.

Deductions and credits should be part of your overall tax-reduction strategy. We’ll go over both and suggest ways you can maximize them.

Start in minutes

Bookkeeping? Taxes? CFO services?

Our bookkeeping and accounting experts keep your books clean, organized, and on time, every time.

One benefit of working with Xendoo’s experienced tax specialists and CPAs is that we know how to save you money on taxes legally. Most tactics that can lower your tax bill fall into three categories.

Deductions

Credits

Investment strategies or losses

We’ll break down each of these and show you how to lower your taxable income to pay less in taxes.

1. Pass-through tax deduction (QBI)

Congress passed the Qualified Business Income (QBI) deduction as part of the Tax Cuts and Jobs Act. It’s commonly known as the pass-through tax deduction and will end after the 2025 tax year. With the pass-through tax deduction, you can deduct up to 20% of your business income from a pass-through entity.

Your overall business income or loss determines the pass-through deduction. If you have several businesses and an overall loss, you can’t claim it. This is true even if one or more of your businesses was profitable.

Finally, you have to have taxable income to qualify. If the standard deduction or other deductions reduce your tax liability to zero, you won’t be able to claim it.

There are also income limitations on “specified service” businesses, such as doctors and lawyers—who are likely highly paid and self-employed. If your income comes from one of the specified services, you still qualify for the pass-through deduction. However, it starts phasing out at $321,400 for married filing jointly or $160,700 for other filers. If your income is over $260,700 ($421,400 joint), the pass-through deduction decreases.

The pass-through deduction can be complicated. (The IRS has 248 pages of guidance on it.) However, if you qualify, it can significantly lower your taxable income—at least through 2025.

2. Charity donations

As a pass-through entity, you’ll claim charity donations on your Form 1040—your individual return. You must make charitable donations to an organization that the IRS recognizes.

Your total charitable donations can’t be more than 60% of your AGI, including your business income. Some charities have lower limits. These are explained in the IRS Deductibility Status Codes.

If you exceed this amount, you can carry over deductions for up to five years. Keep a record of your donation for documentation. You’ll need additional documentation for the below.

Donations of cash or property worth over $250 require a letter of acknowledgment from the charity.

Non-cash donations of $500 or more require you to fill out Form 8283. You’ll also need an appraisal if your total donations exceed $5,000.

You can’t deduct the value of your volunteer time or services. However, you can deduct expenses related to volunteering like travel and mileage.

3. Business expense write-offs

You can deduct expenses related to running your business. Most business owners don’t claim all these expenses, either because they don’t know about them or they don’t keep records. Some common business expense deductions include:

If you use your vehicle for business purposes, you can deduct its expenses. You may also be able to deduct the cost of a company vehicle.

You’ll use either the accrual or standard mileage rate to determine the deduction amount. The standard mileage for 2022 is 58.5 cents per mile for the first half of the year. It’s 62.5 cents per mile for the second half of the year. The standard mileage rate is more beneficial if your car gets good gas mileage and has low operating expenses.

To figure out your mileage deduction, keep track of the miles that you drive for business purposes. You’ll also need to provide the total miles you drove the car. If you take the standard mileage, you can still deduct auto loan interest, vehicle taxes and fees, and parking and toll expenses.

Your other option is to deduct the actual expenses. This includes auto-related expenses such as:

Gas

Repairs

Maintenance

Insurance

Depreciation

Garage fees

Licenses

You’ll need to keep track of your actual expenses and how many miles you drove the car. Calculate the business-related mileage by dividing the business miles by the total miles. Once you figure out the business-related mileage, deduct a corresponding percentage of actual costs.

If you buy an electric vehicle, you can also qualify for the electric vehicle tax credit—up to $7,500. However, that’s a separate credit, not a deduction.

5. Depreciation

Business equipment will lose its value over time as you use it. You can deduct the depreciation, although there are limits. You can use one of several methods to claim depreciation:

Section 179 deduction – gives you a large deduction for the first year’s depreciation. For 2022, the deduction limit is $1,080,000.

Bonus depreciation – deducts a larger amount of the purchase price for new vehicles and equipment. The Tax Cuts and Jobs Act increased the bonus deduction to 100% for 2022, but it will decrease each year. In 2023, it will be 80%, 60% the next year, and so on.

Modified Accelerated Cost Recovery System (MACRS) depreciation – deduct more depreciation during the early years you own an asset and a smaller amount in the later years.

Business vehicle deduction – deduct up to $10,200, plus up to $8,000 in bonus depreciation. For an SUV (between 6,000 to 14,000 pounds), you can deduct the entire cost of the vehicle the year you buy it using bonus depreciation.

6. Business startup costs

You can claim a deduction for the costs of starting your business. This deduction is capped at $5,000 for the first year if your total startup costs were under $50,000.

If your expenses were over $50,000, reduce the amount you deduct by the amount over $50,000. If your startup costs were over $55,000, you don’t qualify for a first-year deduction.

Instead, you’ll need to spread out your expenses and claim them starting in your second year for 15 years. If you anticipate a loss in your first year, it may be better to break up your startup costs and use them to offset profits in later years.

7. IRA contributions

There are several different types of IRAs, and they all offer tax advantages—although not all contributions are tax deductible.

SEP IRAs

SEP IRAs are ideal if you’re self-employed or don’t have employees. They have much higher contribution caps than traditional IRAs—either $66,000 or 25% of total compensation, whichever is less. However, if you set up a SEP IRA for yourself, you also have to set up and fund one for all eligible employees for an equal percentage. Contributions to a SEP IRA are tax deductible.

SIMPLE IRA

A SIMPLE IRA is a good option if your business has no more than 100 employees who earned at least $5,000 in the past year. Unlike SEP IRAs, employees can also contribute to SIMPLE IRAs. The SIMPLE IRA contribution limits are $1,400 for 2022 and contributions are tax deductible.

Roth IRA

The contributions you make to a Roth IRA are not deductible. However, since you’ve already paid taxes on the money, you won’t have to pay taxes when you withdraw it. There are no penalties for early withdrawal.

If you think you’ll be in a higher tax bracket when you retire, a Roth IRA can be the better option. As long as your income is less than $129,000 ($204,000 joint), you can open an IRA. You can contribute up to $6,000 (or $7,000 if you’re over 50) for 2022. However, you won’t be able to contribute as much if your income is higher than $129,000 ($204,000 joint).

SEP IRAs

SIMPLE IRA

Roth IRA

2022 contribution limits

$66,000 or 25% of total compensation

$1,400

$6,000 $7,000 for those over 50

Are contributions tax deductible?

Yes

Yes

No

Who’s it a good fit for?

You’re self-employed or don’t have employees

Your business has no more than 100 employees

You’ll be in a higher tax bracket when you retire

8. Health insurance plan deductions

If you’re self-employed, you may be able to deduct insurance premiums for your family, including:

Health

Dental

Long-term care

Even if you take the standard deduction, you can still deduct insurance premiums. However, you can only claim this deduction if you or your spouse were not eligible for an employer-sponsored plan. You also need a net income to claim this deduction.

If your small business offers health insurance to employees, you can also deduct the amount you contribute to their insurance premiums. It’s more complicated for partners and 2% S corporation shareholders, but you can still deduct health insurance premium contributions.

9. HSA contributions

An HSA is a health savings account you can use to pay for qualifying medical costs. You’re only eligible for an HSA if you have a high-deductible insurance plan. Your contributions are tax-deductible, and the earnings and qualified withdrawals are tax-free.

The maximum amount you can contribute for 2022 is $3,650 for yourself or $7,300 for your family. For 2023, the amounts increase to $3,850 for yourself and $7,750 for your family. The limits change yearly based on inflation. If you’re over 55, the limits are $1,000 higher.

2022 Tax Year Limits

Single Plan

Family Plan

Max Contribution Limit

$3,650

$7,300

Minimum Deductible

$1,400

$2,800

Maximum Out-of-Pocket

$7,050

$14,100

Over 55 Catch-up

$1,000

$1,000

For retirement plans, don’t contribute more than the limit. Otherwise, you’ll lose the tax benefits, and you may have to pay a 6% penalty. Also, you have until next year’s tax deadline to make contributions, so you can deduct contributions for 2022 until April 2023.

To claim a deduction for your HSA account, you don’t have to itemize it but you must have income. HSAs are one of the more complicated deductions. Below is guidance for different tax situations. If you’re unsure, consult one of our licensed tax CPAs.

Business owners or sole proprietors – you can’t contribute to an HSA with your pre-tax dollars. However, you can contribute with your after-tax money and deduct your contributions from personal income tax.

LLCs with employees – you can make pre-tax contributions to an HSA. You can also deduct any contributions you make to their HSAs. If your business is an S corporation, the business can’t provide owners with tax-free contributions to HSAs.

C corporations – the IRS taxes corporations as legal entities. For HSAs, it treats owners the same as employees. However, all contributions must still comply with IRS rules for employer contributions.

10. Tax-loss harvesting

You can use losses on capital investments to offset capital gains taxes. The capital gains tax is what you pay when you sell an asset for a profit.

Tax-loss harvesting is a year-end strategy to lower your tax bill. You’ll need to sell an asset at a loss to claim this deduction.

If your losses exceed your gains, you can deduct up to $3,000 from your personal income. You can claim losses over $3,000 in future years. But, don’t purchase a similar investment within 30 days—before or after—a loss. If you do, you can’t claim it. This is called a “wash sale.”

11. Student loan interest

You can deduct up to $2,500 of student loan interest if your MAGI is less than $70,000 or $145,000 filing jointly. Your MAGI is your AGI plus any untaxed foreign income, non-taxable Social Security benefits, and tax-exempt interest. Student loans you took out for your spouse, dependents, or yourself qualify.

If your MAGI is between $70,000 and $85,000 ($175,000 filing jointly), you can still claim some interest. However, you can’t claim the entire $2,500. Here’s a breakdown of the credit amounts depending on your filing status.

Maximum credit amount

$2,500

Single, head of household income (MAGI) limit

Less than $70,000 – eligible for the full amount $70,000- $85,000 – partial credit

Married filing jointly income (MAGI) limit

Less than $145,000 – eligible for the full amount $145,000-$175,000 – partial credit

This deduction is “above the line,” which means you subtract it from your taxable income. You can claim it even if you take the standard deduction. But, you can’t take the student loan interest deduction if:

Your filing status is married filing separately

Someone claims you as a dependent

You’re not legally obligated to repay the loan

12. Higher education costs (for yourself or children)

If you’re paying for college for yourself or your children, you may be eligible for either the American opportunity tax credit (AOTC) or the lifetime learning credit.

The American opportunity tax credit is worth more but has stricter rules for qualification. If you qualify, you can claim a $2,500 tax credit. The full credit is available if your modified adjusted gross income (MAGI) is $80,000 or less for single filers or $160,000 or less for joint filers.

If your MAGI is between $80,000-$90,000 ($180,000 for joint filers), you can get a partial credit. Taxpayers can use the American opportunity tax credit for:

Undergraduate education

A maximum of four years

Independent students

Parents claiming dependent students

You can claim up to 20% of the first $10,000 you pay in tuition and fees when you claim the lifetime learning credit. It’s available for undergraduate, graduate, or vocational credits. There’s also no limit on how many years you can claim it.

However, you can’t claim both credits in the same year. You can claim the lifetime learning credit if your MAGI is less than $59,000 ($118,000 for joint filers). If your MAGI was over $59,000 but under $69,000 ($138,000 for joint filers), you can get partial credit.

Here’s a comparison of credit amounts and income limits to decide which will reduce your taxes the most.

American opportunity tax credit

Lifetime learning credit

Maximum credit amount

Up to $2,500 credit per eligible student

Up to $2,000 credit per return

Single, head of household income (MAGI) limit

Full amount – $80,000 or less to claim the full amount Over $80,000 and under $90,000 for partial credit

$80,000 or less to claim the full amount Over $80,000 and under $90,000 for partial credit

Married filing jointly income (MAGI) limit

$160,000 or less to claim the full amount Over $160,000 and under $180,000 for partial credit

$160,000 or less to claim the full amount Over $160,000 and under $180,000 for partial credit

How to pay less taxes with Xendoo

Xendoo’s experienced, licensed CPAs and tax professionals do more than file your taxes for you. Unlike some other bookkeeping and business tax services that outsource tax preparation and filing, we do it all in-house. We assess your unique tax situation and identify all the ways that you can lower your taxable income and pay less in taxes. Reach out today for a consultation.

This post is intended to be used for informational purposes only and does not constitute as legal, business, or tax advice. Please consult your attorney, business advisor, or tax advisor with respect to matters referenced in our content. Xendoo assumes no liability for any actions taken in reliance upon the information contained herein.

Minimizing your company’s tax burden can help maximize profits. One way of doing this is through business tax credits. Leveraging the right tax credits can save your business thousands of dollars in taxes each year.

However, there are many types of business tax credits and the IRS has strict eligibility requirements. How do you know which tax credits will save you the most money? An experienced tax professional can identify which credits you’re eligible for and even file them for you.

This guide goes over business tax credits that could save you money on taxes. You’ll also learn how to maximize their impact with the help of an experienced CPA or tax accountant.

Small Business Tax Credits vs. Deductions

Small business tax credits and deductions are valuable tools for reducing your tax bill. They are incentives the government offers to reduce the amount of taxes you owe. However, they work in different ways.

Tax Credits

Unlike deductions, tax credits directly reduce the amount of taxes you owe instead of lowering your taxable income. If you’re eligible, you can lower the amount of taxes you owe dollar-for-dollar.

For example, let’s say you owe $1,500, but you have a credit worth $500. You could deduct the credit amount ($500) from what you owe ($1,500). Then, your total amount would be $1,000.

Tax credits can range from investing in research and development to hiring new employees.

For example, the Work Opportunity Tax Credit rewards small businesses for hiring individuals that meet certain criteria. Knowing which tax credits are available to you and how to use them can significantly impact your business finances.

Tax Deductions

Deductions can move you to a lower tax bracket, so the IRS taxes you at a lower rate. Examples of tax deductions include business expenses like office supplies, equipment, and travel costs.

Deductions can also be tricky as there are different rules for claiming them, and not all expenses are tax deductible. If you’re unsure which small business tax deductions you may qualify for, consult a tax professional.

11 Small Business Tax Credits

The IRS has specific eligibility requirements for each tax credit. To maximize your tax savings, here are 11 of the top tax credits for businesses and how to use them.

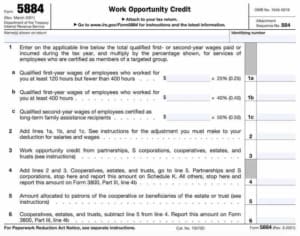

1. Work Opportunity Credit (Form 5884)

The Work Opportunity Tax Credit (WOTC) is a federal tax credit available to employers who hire and employ individuals from certain targeted groups. The IRS bases this credit on the employee category, how much you’ve paid them during the first year of employment, and how many hours they’ve worked.

To qualify, you must hire an eligible worker in one of these categories:

Unemployed veterans

Ex-felons

Temporary Assistance for Needy Families (TANF) recipients

Supplemental Nutrition Assistance Program (SNAP) recipients

Designated community residents

Vocational rehabilitation referrals

Long-term family assistance recipients

Qualified summer youth employees

Qualified long-term unemployed individuals

You can claim the Work Opportunity Tax Credit by completing Form 5884 and submitting it along with your tax return.

You must also provide information about newly-hired employees onForm 8850 within 28 days of the hire. You’ll submit this form to your state workforce agency for certification.

In case of an IRS audit, you should maintain records for your WOTC claims for at least the last four years. Those who meet all eligibility requirements could receive up to 40% of the first $6,000 in wages ($2,400) as a tax credit.

2. R&D Credit (Form 6765)

Businesses that invest in research and development (R&D) activities might be eligible for the R&D Tax Credit. To be eligible, your business must incur expenses for developing or improving a product, process, technique, invention, or software. Qualifying expenses may include wages, supplies, and contract research fees.

Startups that have less than $5 million in annual gross receipts could apply up to $250,000 of the credit to offset payroll taxes. Since the IRS calculates the tax credit amount based on the amount a company spends on R&D, most early-stage startups don’t qualify for the full amount.

The Inflation Reduction Act increased the maximum threshold from $250,000 to $500,000, starting with the tax year 2023.

To obtain this credit, businesses must submit Form 6765 to their federal income tax return by April 18, 2023. You must also include information about your R&D activities and expenses.

3. Alternative Fuel and Electric Vehicle Credits

Taxpayers who purchase, lease, or install alternative fuel vehicles and infrastructure are eligible for a series of federal tax credits. The credit amounts vary depending on the type of vehicle or infrastructure you install.

Biodiesel and Renewable Diesel Fuels Credit (Form 8864) – Claim a credit of up to $1.00 per gallon of biodiesel, renewable diesel, and alternative fuels you purchase.

Alternative Fuel Vehicle Refueling Property Credit (Form 8911) – If you install an alternative fuel vehicle refueling station, you can receive up to $30,000 in tax credits.

Biofuel Producer Credit (Form 6478) – This credit is available to taxpayers who produce biodiesel and renewable diesel fuels. The amount varies depending on the type of fuel you produce.

Qualified Electric Vehicle Credit (Form 8834) – If you purchase or lease a new electric vehicle, you may be eligible for up to $7,500 in credits.

You’ll need to file the appropriate form with your federal income tax return to claim these credits. Your filing date should match the deadline for your tax return. Alternative fuel and electric vehicle credits may be subject to phase-out dates and other restrictions. It’s best to consult a professional for tax compliance and filing information.

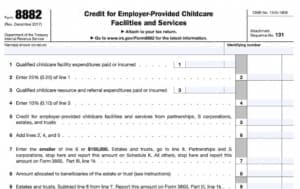

4. Employer-Provided Childcare (Form 8882)

If your business provides childcare assistance to its employees, then you may be eligible for the Employer-Provided Childcare Credit (Form 8882). The government encourages businesses to offer childcare benefits to assist working parents. The credit can offset some of those costs.

To determine eligibility, you’ll need to calculate the cost of qualified expenses for each employee. The credit equals 25% of qualifying expenses up to $150,000. You can also claim 10% of childcare resources and referral expenses.

To claim the Employer-Provided Childcare Credit, submit Form 8882 by the tax return due date. You have up to three years to file claims for this credit. Also, you should keep childcare expense records for at least four years from the filing date.

5. Small Employer Health Insurance Premiums (Form 8941)

To offset health insurance coverage expenses, you can use the Small Employer Health Insurance Premiums Credit (Form 8941). You must have fewer than 25 full-time employees and pay at least half the single coverage cost for each employee.

You can calculate the amount of the credit as a percentage (up to 50%) of your health insurance premiums. For non-profits, it is up to 35%. To claim the credit, you must submit Form 8941 with your federal income tax return by April 18, 2023. You will need to provide information about your health coverage and expenses.

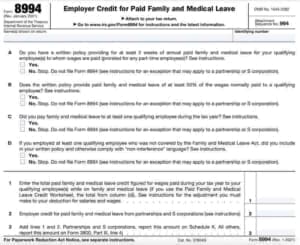

6. Paid Family and Medical Leave Credit (Form 8994)

Your business may be eligible for the Paid Family and Medical Leave Credit (Form 8994) if it provides paid leave to employees. The credit encourages businesses to offer paid leave by offsetting the costs.

To qualify, a business must have a written policy that provides at least four weeks of annual paid family and medical leave to full-time employees. Part-time employees should receive up to two weeks of paid leave.

You can calculate the credit as a percentage (ranging from 12.5% to 25%) of the wages you pay employees while on leave. You must provide records of wages along with Form 8994 by April 18. 2023.

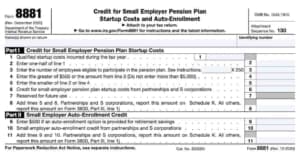

7. Retirement Plan Startup Costs (Form 8881)

Businesses that have a qualified retirement plan are eligible for the federal Retirement Plan Startup Costs tax credit (Form 8881). It incentivizes businesses to offer retirement plans—401(k), SEP, SIMPLE IRA, and others—to employees.

The maximum credit is 50% of qualifying startup costs with a $500 limit. If your business qualifies you could reduce your tax bill by up to $500. To qualify, a business must have 100 or fewer employees that have received at least $5,000 in compensation from you in the previous year.

To claim the credit, submit Form 8881. The deadline to submit will vary depending on your tax filing status.

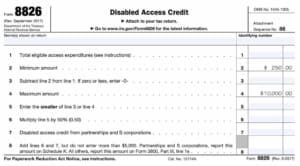

8. Disabled Access Credit (Form 8826)

If you’ve spent money to make your business locations accessible to individuals with disabilities, you may qualify for the federal Disabled Access Credit (Form 8826). Qualifying costs include modifying entrances, restrooms, and parking.

To apply for the credit, your business must have earned $1 million or less and have fewer than 30 employees. The maximum credit will be 50% of the expenses, with a maximum of $5,000 per year. To receive the credit, you’ll need to submit Form 8826.

Note, you may also be eligible for a business expense deduction of up to $15,000 too. It’s called the Architectural Barrier Removal Tax Deduction. To be eligible, you must have spent money on making your facility ADA-accessible to the elderly or disabled.

9. Energy Efficient Home Credit (Form 8908)

The Inflation Reduction Act (IRA) brought the Energy Efficient Home Credit (Form 8908) back. If you’re a contractor that has made energy-efficient improvements to homes you sold or rental properties, you may qualify.

The maximum credit limit for the 2022 tax year is a $500 lifetime credit. As a lifetime credit, any amount you took in previous years would count toward the total $500 limit.

However, the IRA increased this to an annual credit of up to $1,200 for years after 2022. To qualify for this business tax credit, you must meet energy-efficient improvements. Those may include installing energy-efficient:

Insulation

Windows

Water heaters

Central air conditioning

Furnaces

Doors

Roofing

To claim this credit, you’ll need to keep records of qualified energy-efficient expenses and file Form 8908.

10. Low-Income Housing Credit (Form 8586)

To qualify for the Low-Income Housing Credit (Form 8586), your business must develop and operate low-income residential housing. Eligible businesses must meet specific criteria set by the IRS. These include:

Income restrictions

Rent limits

A commitment to maintain the property over a particular period

You base the credit amount on the qualified basis of the property, which is either 4% or 9% of the project’s gross construction costs.

11. General Business Credit (Form 3380)

The General Business Credit (Form 3800) tallies up all applicable business tax credits. You calculate the credit as the sum of all applicable business tax credits claimed in the current year. You can carry back unused amounts for one year or carry forward 20 years.

You’ll submit Form 3800 with your federal income tax return. Your tax return deadline will depend on your filing status. When filing, provide information about all the business tax credits you’ll claim during the current year.

Lower Your Tax Bill With a CPA

With knowledge of the tax code, including business tax credits, deductions, and more, your CPA can do more than prepare your taxes. An experienced CPA can provide valuable advice on the best ways to lower your tax bill and maximize the profitability of your business.

Tax credits are powerful tools. Xendoo has a team of in-house bookkeepers, CPAs, and tax experts. You don’t just get business tax services, you get personalized financial advice.

As tax professionals, we make it our mission to maximize your business tax savings. Schedule a free consultation and we’ll get to know your business and unique tax situation.

This post is intended to be used for informational purposes only and does not constitute as legal, business, or tax advice. Please consult your attorney, business advisor, or tax advisor with respect to matters referenced in our content. Xendoo assumes no liability for any actions taken in reliance upon the information contained herein.

As a business owner, you probably know that you should file taxes on time. However, if you’ve fallen behind on taxes, you’re not alone. Over 33% of Americans procrastinate doing taxes until the last minute. Reasons for procrastinating taxes vary. Some find it too time-consuming and stressful, while others worry if they are filing correctly.

No matter the reason, missing the tax filing deadline could be costly, especially for businesses. What happens if a business doesn’t file taxes by the due date? The Internal Revenue Service (IRS) can send you a bill for penalties and additional fees. However, we understand that tax filing requirements and rules change each year. It’s hard to keep up without your own accountant or business tax services.

When you run a business, it’s easy to fall behind on your books and taxes. This guide will go over tax filing deadlines and what happens if your business doesn’t file taxes. We’ll also outline your options if you’re behind on your books, missed a filing deadline, or have tax payments.

Tax day is usually April 15th. However, since that falls on a Saturday this year, the date is April 18th. Even though April 18th is tax day, filing deadlines vary.

The date you need to file depends on the following.

Your business entity – How you file depends on if you’re a C corporation, S corporation, Partnership, or LLC.

The state you operate – Check with your state’s revenue department for their filing requirements and deadlines.

Your tax status – Tax-exempt organizations and non-profits have different filing deadlines than for-profit businesses.

The type of return you’re filing – Different returns, including IRS Form 1120 for corporation income tax, have different deadlines.

Whether you’ve requested an extension – If you’ve requested an extension and it’s accepted, you have extra time to submit your taxes. However, you must pay what you owe by the deadline.

Owed taxes or refunds – If you owe taxes, the deadline to pay may be different than the deadline to file your return.

Location – If you’re outside the United States, there are different filing requirements and deadlines.

We recommend you double-check with the IRS and your state’s revenue department for any updates to the filing requirements and deadlines. A tax accountant can also advise you on deadlines and changes.

Here’s a list of common forms and tax filing requirements for businesses and their filing deadlines. For a complete list, we’ve updated our 2023 tax deadlines for businesses here.

Tax Filing

Description

Who Needs To File

Filing Deadline

Estimated quarterly payments

By paying estimated taxes, businesses avoid owing a large amount at the end of the tax year.

Businesses that expect to owe more than $1,000 in taxes at the end of the tax year pay estimated quarterly payments.

Q1: April 18, 2023

Q2: June 15, 2023

Q3: September 15, 2023

Q4: January 15, 2024

W-2

A W-2 details an employee’s wages for the year as well as taxes withheld from their earnings.

Employers must provide W-2 forms to all employees who received wages, salaries, tips, or other compensation during the tax year.

January 31, 2023

W-9

Non-employees and contractors fill out W-9 forms to provide tax information.

Anyone who pays an independent contractor or non-employee must file a W-9 form.

Not subject to IRS deadlines but non-employees should fill it out before beginning work

1099-NEC

The 1099-NEC reports nonemployee compensation payments, such as payments to independent contractors.

Any business that pays an independent contractor or nonemployee more than $600 in a year must file a 1099-NEC form.

January 31, 2023

What Happens if a Business Doesn’t File Taxes?

All corporations must submit a corporate income tax return, even with no profits. LLCs who choose to be taxed as corporations are also responsible for filing a federal tax return. This must be done regardless of whether or not an LLC conducts any business activities during the year.

If your business doesn’t file taxes, you’re subject to IRS penalties and additional fees. It’s best to deal with tax filing issues sooner rather than later. However, if you missed a deadline, it’s not the end of the world. Initially, the IRS sends a notice or letter to notify taxpayers when they’ve missed a deadline or payment.

Everyone’s tax situation can vary. Businesses that don’t meet the tax filing due dates have several options. An experienced tax professional can assess yours and help you meet tax requirements.

If you’ve had IRS notices that you haven’t responded to after several months, the IRS may take these steps.

Penalties

Different penalties apply depending on your unique tax situation. Below are penalties you could face if you don’t accurately file your taxes on time or miss payments.

Failure to File Penalty – if you don’t file your tax return by the due date

Failure to Pay Penalty – if you don’t pay the full amount of taxes you owe by the due date

Penalty for Underpayment of Estimated Taxes – if a business doesn’t pay enough estimated yearly taxes

Accuracy-Related Penalty – if the tax return is incorrect or you fail to report information correctly

In addition to penalties, the IRS charges interest on your unpaid taxes. This is in extreme cases. We’ll look at each penalty in detail, so you know how much it could affect you.

Failure to File Penalty

The IRS calculates the Failure to File penalty as a percentage of taxes that you owe each month the return is past due. The fee starts accruing on the due date and continues until you file the return or reach the maximum penalty limit.

This penalty is usually 5% of the taxes you owe for each month or partial month that you miss. The percentage increases each month until it reaches the maximum cap of 25%. If you’re more than 60 days late on submitting your return, you’ll pay either $435 or 100% of the unpaid tax balance—whichever is lower.

Don’t forget that you can request an extension if you can’t meet the tax filing deadline. The extension will give you an extra six months to file your return, but it won’t change the due date for the taxes you owe. The deadline to file for an extension is the same as the return’s original due date.

Here’s how the Failure to File penalty works:

Months Late

Penalty Amount

1

5%

2

10%

3

15%

4

20%

5+

25%

Failure to Pay Penalty

Taxpayers who have filed taxes but didn’t pay them on time face a Failure to Pay Penalty. The IRS calculates this penalty as a percentage of the amount you owe. The penalty increases gradually each month you haven’t paid. Even if you file your taxes on time, you need to have the money to pay what you owe.

For each month you haven’t paid, the IRS assesses a penalty of 0.5% of the amount you owe. It starts accruing from the due date and continues until you pay it or it caps at 25%.

Remember, the IRS may waive penalties and interest for taxpayers who can show reasonable cause for failure to pay on time. You can request an installment agreement if you cannot pay your taxes by the deadline. With this, you make monthly payments to cover what you owe. However, there’s a fee for setting this up, and interest still accrues on anything you don’t pay.

Here’s a chart to help you visualize how the Failure to Pay penalty works:

Months Late

Penalty Amount

1

0.5% of the unpaid taxes

2

1% of the unpaid taxes

3

1.5% of the unpaid taxes

4

2% of the unpaid taxes

5

2.5% of the unpaid taxes

Unpaid Taxes and Penalty Interest

The IRS may also tack on interest for any unpaid taxes or fees. Interest accumulates daily and the IRS sets it by the federal short-term rate. The IRS calculates interest from when payment was due until you pay the amount you owe.

As of 2022, the interest rate for underpayment of taxes is 6% per year. This compounds daily, meaning it adds daily to the total amount you owe. The rate for overpayment of taxes is 5% per year. If you pay more than what you owe, you will get a lower rate of interest.

Corporations should be aware of corporate interest rates, which are higher than individual rates.

Here’s how interest works on unpaid taxes.

Number of Years

Accrued Interest

1

6%

2

12%

3

18%

4

24%

5

30%

Filing and paying your taxes within the deadlines can help you avoid costly penalties from the IRS. If you have fallen behind on filing or paying your taxes, consult with a tax professional.

Xendoo’s tax accountants will help you file the right paperwork to prevent additional charges. We’ve seen all kinds of tax situations from missed deadlines to late taxes, so no judgment here.

How Long Can You Go Without Filing Business Taxes?

It’s always best to file and pay your taxes as soon as possible. If this isn’t possible, a tax accountant will help you minimize your liability.

A tax professional familiar with complex tax laws and regulations can help you:

Apply for an extension to get a few more months of breathing room.

Lower your tax bill by leveraging deductions, credits, and other strategies to reduce liability.

Navigate your filing obligations and comply with all applicable laws and regulations.

Avoid errors and omissions that could trigger an audit or penalties.

Even though you must file and pay taxes, there are ways to lower your tax bill legally.

Tax Evasion vs. Tax Avoidance

Tax evasion is illegal and involves deliberately falsifying or concealing income, inflating deductions, or failing to file taxes. On the other hand, tax avoidance is a legitimate way of reducing your tax bill by using legal methods such as deductions and credits.

What Happens if a Business Doesn’t File Taxes for Three Years?

If you don’t file your taxes for three consecutive years, the IRS may consider it willful neglect and impose harsher penalties.

These penalties can include levies on your wages or bank account. You may also be subject to a federal tax lien that limits your access to loans or credit. In extreme cases of intentional tax evasion, the IRS may impose fines of up to $250,000 and possible jail time.

Tax Liens

The government can take action against those who fail to pay their taxes through a tax lien. It takes assets or property the taxpayer owns and gives the government legal interest in those assets. If you continue to owe taxes, the agency might begin proceedings to seize your assets.

Again, this is in rare cases, and usually when the IRS suspects tax evasion.

A tax lien can make it difficult for taxpayers to sell or refinance their property. You must pay off the lien before any transactions occur. In more extreme cases, the government might foreclose on the property.

It’s important to note the difference between a tax lien and a levy. A levy is a legal process by which the government takes possession of assets or property to settle a debt. A lien serves as a legal claim on those same assets or property to secure payment of taxes. There are also different types of tax liens.

Notice of Federal Tax Lien

The IRS uses a Notice of Federal Tax Lien (NFTL) as its initial step when taxpayers have not paid their tax debt. This document serves as public notification that the government holds a legal claim over the taxpayer’s property or assets. If you pay off the taxes or reach an installment agreement, the IRS can lift the NFTL.

Notice of State Tax Lien (NSTL)

A Notice of State Tax Lien (NSTL) is similar to an NFTL but the appropriate state agency files it instead of the IRS. The same rules apply with an NFTL—if you pay the taxes, the IRS can release the lien.

If you receive an NTFL or an NSTL, it is crucial to take action. Tax liens can devastate your financial and credit health, so you should address the issue head-on.

What to Do if You Owe Back Taxes or Miss Filing Deadlines

Back taxes can be expensive and stressful. But, there are measures to help businesses pay off their debt.

If you’re behind on filing or paying taxes, you have options. Here are some steps to help you avoid or lower expensive tax penalties, interest, and other fees.

File a Tax Extension

If you need more time to collect all the documents and submit your business tax returns, you can file an extension. However, filing a tax extension doesn’t give you more time to pay the taxes that you owe. To prevent extra costs due to interest and penalties, make sure to pay by the initial due date.

C corporations, S corporations, and partnerships must fill out Form 7004 to ask for a tax filing extension. Single-member LLCs, sole proprietorships, and trusts submit Form 4868 to request a filing extension. If the IRS approves your extension, you’ll have an additional six months to submit your tax return.

Companies that face unexpected issues may be eligible for a hardship extension. For a hardship extension, you must submit a written request that explains why you need more time and includes the date you’ll submit the return.

Dispute a Penalty

If you believe there has been an error, you can dispute a penalty. Generally, businesses must provide evidence to support their argument and show why the IRS should remove or reduce the penalty.

For instance, if you receive a penalty for failure to file or underreporting income, you might have a reasonable cause for the oversight. Reasonable circumstances could include a fire or natural disaster or incorrect advice from a certified public accountant (CPA).

Waive a Penalty

You can also use first-time penalty abatement (FTA) to request a penalty waiver. To qualify for FTA, your business must have filed all returns and paid all taxes due within the past three years.

An administrative waiver is another way businesses can request relief from penalty charges.

Businesses can request an administrative waiver if they are facing financial hardship or if there’s a reasonable cause for the error.

The IRS also has a Voluntary Disclosure Program (VDP) for business taxpayers who fail to report or underreport their taxes. Businesses can come forward voluntarily and resolve their tax issues. As a result, they limit their exposure to interest and/or penalties by working with the IRS.

Reduce Payment

You can also request an Offer in Compromise (OIC), a settlement agreement between a taxpayer (you) and the government. In it, the two parties agree on a reduced tax payment. You would only be responsible for paying the new amount. However, this option should only be used as a last resort. Taxpayers must provide significant financial information to qualify.

Businesses may also consider filing for bankruptcy protection. This will stop any IRS or state tax agency collection activities while the business reorganizes its financial obligations. It may forgive taxes entirely depending on the type of bankruptcy. However, filing for bankruptcy is a complex process and has many financial consequences, so treat it as a last resort.

Setup a Payment Plan

If you can’t pay in full, you can try setting up a payment plan. To do this, file Form 9465 with the IRS by the deadline. With a payment plan, you make monthly payments toward the taxes you owe. While this won’t reduce your tax liability, it will break up the total into manageable payments.

Businesses can also apply for Currently Not Collectible (CNC) status if they cannot pay their taxes due to financial hardship. When a taxpayer has CNC status, the IRS will temporarily postpone collection actions. It will not pursue collection until the taxpayer’s financial situation improves.

Hire a Business Tax Professional

Skilled tax accountants provide expert advice on how to lower your tax bill and get more money back. They should know all the business tax deductions and credits to save you money.

When choosing a business tax professional, look for experience in business tax preparation and resolution. Xendoo’s team of CPAs, bookkeepers, and tax specialists can help you with:

If you’re concerned about filing taxes for your business on time, hire a tax professional. In addition to hiring a tax consultant, it’s a good idea to invest in a year-round bookkeeping service.

Like taxes, updating your books each month is important but it’s easy to fall behind. If you are behind on your taxes, chances are that you are behind on your books too. With the right help, you can get your books in order and prepare for the next tax filing season.

Xendoo has all the finance expertise a business needs in one place. You can choose from business tax services, bookkeeping, accounting, and CFO services. To learn how Xendoo can help with your particular tax situation or business finances, schedule a time to talk to an expert.

This post is intended to be used for informational purposes only and does not constitute as legal, business, or tax advice. Please consult your attorney, business advisor, or tax advisor with respect to matters referenced in our content. Xendoo assumes no liability for any actions taken in reliance upon the information contained herein.

Filing taxes as a small business owner can be complex, with numerous factors to consider. From tax law revisions to the overwhelming number of forms, understanding your small business tax rate and how to file can be difficult.

Your business entity type and preferred filing status will also affect your tax rate. For example, LLCs that opt for the IRS to tax them as corporations are subject to corporate tax rates. Other businesses like sole proprietorships and limited partnerships may be subject to self-employment taxes. Understanding your entity type and requirements is the first step toward filing your taxes accurately and efficiently.

Tax laws are constantly changing, and it can be challenging to keep up with the latest revisions. A professional tax advisor or CPA can accurately file your business taxes on time. Our experienced tax specialists also know all the deductions and credits that can lower your tax bill.

We’ll cover small business tax rates, filing requirements, and various strategies that can help to reduce your taxes.

Depending on your business structure and income, you may be subject to one or more types of taxes.

Corporate tax

Self-employment tax

Sales tax

Payroll tax

We’ll cover everything you need to know about tax rates for the most popular business entity types—corporations, partnerships, sole proprietorships, and LLCs.

Pass-Through Entities

The IRS considers most U.S. businesses (around 95%) pass-through entities, also known as flow-through entities. Pass-through entities include:

Sole proprietorships – Businesses with a single owner

Partnerships – Businesses with two or more owners

Limited liability companies (LLCs) – LLC owners can protect their personal assets from their business, but get the tax benefits of a pass-through entity. LLCs can also request the IRS tax them as corporations.

S corporations (S corps) – Corporations that have a special tax designation, so the IRS taxes them as pass-through entities.

The biggest advantage of pass-through entities is that they avoid double taxation. The term refers to when the IRS taxes the same income twice—once at the corporation level and again on an individual shareholder’s personal income tax.

Corporations

A corporation (C corporation) stands alone from its shareholders. The IRS taxes corporations as separate legal entities, which opens them up to double taxation. C corporations must report profits and earnings to the IRS. The IRS then taxes them at the corporate income tax rate. Shareholders still must file their personal income tax returns and report the corporate dividends and capital gains they get as part of their taxable income.

Let’s say a corporation earns $1,000,000 in profit and then passes on $200,000 in dividends to its shareholders. The business would have to pay corporate income taxes on the full amount of $1,000,000. Individual shareholders would also be subject to taxation on their share of the $200,000 dividend earnings.

The federal corporate income tax rate currently sits at 21%. A corporation with $100,000 in taxable income would owe $21,000 in taxes. With that said, that’s not necessarily the amount you need to pay. You can apply various small business tax deductions and credits to help reduce your tax liability.

While corporations have advantages, double taxation can be a major drawback. Most small businesses operate as pass-through entities instead.

Start in minutes

Bookkeeping? Taxes? CFO services?

Our bookkeeping and accounting experts keep your books clean, organized, and on time, every time.

Unlike C corporations, the IRS taxes income for pass-through entities at the individual level. Owners file and pay taxes on all income—including business earnings—on their personal income tax returns. However, there are specific forms you need to include depending on your business structure. For example, partnerships will file Form 1065. S corporations will file Form 1120-S.

If you operate a pass-through entity, your small business tax rate will depend on your income tax bracket. The higher your taxable income, the higher your tax rate. Federal income tax rates range from 10% to as high as 37%.

It is important to note that pass-through entities may be subject to other taxes, outside of income. For example, you may need to pay self-employment tax.

Tax rate

Single individual income

Married (filing jointly) income

10%

$10,275 or less

$20,550 or less

22%

$41,775

$83,550

24%

$89,075

$178,150

32%

$170,050

$340,100

35%

$215,950

$431,900

Updates to Small Business Tax Rates

The IRS updates small business tax rates yearly to account for inflation or other economic changes. Therefore, you should look out for the latest rules and regulations or consult a tax professional. Legislation also impacts your tax bill.

Tax Cuts and Jobs Act (TCJA)

For example, the Tax Cuts and Jobs Act (TCJA) made major changes to the U.S. tax code, deductions, credits, and business tax rates. One of the biggest changes is that it lowered the corporate income tax rate from 35% to 21%. It also introduced a 20% deduction for qualified business income (QBI) from pass-through entities. However, some of those changes will phase out in the next few years.

A total of 23 individual and business tax TCJA provisions are set to expire on December 31, 2025. A tax professional can help you understand these changes and their impact on your business.

Inflation Reduction Act (IRA)

The Inflation Reduction Act (IRA) also influences how much you could pay in taxes. For one, it increased incentives for electric vehicles and other energy-efficient upgrades.

It also proposed a minimum tax rate of 15% for corporations that have made over $1 billion over three taxable years. This change has little to no impact on small business taxes. Unless you are a large, publicly traded corporation—think Walmart, Amazon, and Apple—it won’t have an impact on your business taxes.

What Taxes Do Businesses Pay?

Other than income tax, your small business may be subject to payroll taxes, self-employment taxes, and more. In addition to federal taxes, you may also have state and local taxes. Here is an overview of the taxes that businesses must be aware of:

Payroll or Employment Taxes

If your business has employees, then you’ll need to consider payroll tax. Payroll taxes are the taxes employers pay on employee salaries and wages. They include federal, state, and local taxes and Federal Insurance Contributions Act (FICA) taxes. You’ve likely seen FICA taxes appear as Social Security and Medicare on a paycheck.

The current FICA tax rate is 7.65% for the employer and 7.65% for the employee, or 15.3% total. As the employer, you’re responsible for withholding the appropriate payroll taxes from your employee’s salary and paying them to the IRS.

You’ll also withhold income tax from employees’ wages. To know how much tax to withhold, you’ll need to collect a W-4 Form from employees before they start work. This IRS form has details like an employee’s address, social security number, and tax filing status.

In addition to withholding and FICA taxes, there are other types of payroll taxes, including FUTA and SUTA. For example, Federal Unemployment Tax Act (FUTA) is an employer-paid tax that funds state unemployment benefits. Likewise, employers pay State Unemployment Tax Act (SUTA) taxes to fund state unemployment benefits.

Quarterly Taxes (Estimated Taxes)

Most sole proprietorships, partnerships, and S corps owners pay estimated taxes to the government on a quarterly basis. Instead of paying taxes all at once, it’s broken into four payments. You must pay estimated taxes if the amount you expect to owe is greater than $1,000.

Quarterly taxes usually fall into two categories—self-employment taxes (Social Security and Medicare) and income taxes. Even though you pay quarterly taxes, you’ll still need to file an annual tax return.

There are a few ways that you can calculate your estimated taxes. First, you’ll need to estimate your gross income and how much of that is taxable. Then, factor in possible tax savings from deductions and credits. You can also estimate your yearly taxable income and look at the tax rate for your income bracket.

Another method you can use is to look at your tax return for the past year. You can use last year’s figures to estimate your tax liability for this year. However, this method only works if you don’t expect your income to change much year over year.

The due dates are usually April 15, June 15, September 15, and January 15 of each year. However, some of the dates change if they fall on a weekend or holiday.

Here are the due dates for 2022 and 2023.

2022 tax year

2023 tax year

April 18, 2022

April 18, 2023

June 15, 2022

June 15, 2023

September 15, 2022

September 15, 2023

January 17, 2023

January 16, 2024

If you underpay your estimated taxes or don’t pay them by the due dates, you may be subject to penalties.

Xendoo’s business tax services will help you figure out what you owe if you’re unsure of how to calculate your estimated taxes.

Self-Employment Taxes

You’ll factor self-employment taxes into your quarterly or estimated tax payments. As the name suggests, self-employment taxes are taxes that self-employed individuals must pay. This includes those who own an unincorporated business or another type of pass-through entity.

Self-employment taxes consist of two separate parts: Social Security and Medicare. Currently, the combined tax rate is 15.3%. This situation differs from employers who only have to pay half of their employees’ Social Security and Medicare taxes. You won’t be subject to these payroll taxes if you don’t have any employees.

When filing your taxes, you can deduct your self-employment tax payments as an adjustment to income on your tax return. This deduction ensures that you aren’t double-taxed on the same money. Other tax credits may be available to small business owners to offset some or all of the cost of paying self-employment taxes.

To avoid paying self-employment taxes, consult a tax professional to discuss incorporating your business. You can take advantage of certain IRS regulations for corporations that may reduce your overall self-employment liability.

Sales Tax

While sales tax laws differ by state, retailers generally collect sales tax when they sell tangible goods to customers within their state.

The location of the sale, not the business location, will determine how much you pay in sales tax. For example, if your business is in one state but sells to someone in another state, you’ll pay the respective state’s sales tax. Certain states have reciprocal agreements that allow businesses to only collect sales tax from customers within their own state. It’s best to check with an accountant or tax professional to comply with the applicable laws.

In most cases, you’ll need to register with the applicable state government before collecting and remitting its sales tax. This process usually requires you to list the items you plan to sell and provide account information. You must also keep accurate records of all transactions made within the state. Failure to comply with the applicable laws could result in penalties, interest payments, and other fees.

Xendoo’s bookkeepers and CPAs are familiar with tracking and remitting sales tax for all types of businesses, including ecommerce. If you’re interested in sales tax services, we can do a consultation for your business.

Capital Gains Tax

The IRS collects capital gains taxes on the profits you earn from selling an asset such as stocks, real estate, or other investments.

Capital gains fall into two categories—short-term and long-term. Short-term gains are from assets that you’ve owned for less than one year before selling. Long-term gains are from assets that you’ve owned for more than one year.

Your capital gains tax rate depends on which category it falls under. The IRS taxes short-term capital gains as income. Tax rates for long-term capital gains are different and usually lower than income tax rates.

Here are 2022 long-term capital gains tax rates.

Tax filing status

0% rate

15% rate

20% rate

Single

Under $41,675 taxable income

$41,675 – $459,750

Over $459,750

Married, filing separately

Under $41,675

$41,675 – $258,600

Over $258,600

Head of Household

Under $55,800

$55,800 – $488,500

Over $488,500

Married, filing jointly

Under $83,350

$83,350 to $517,200

Over $517,200

Keep in mind that capital gains tax rates can vary from this for particular types like collectibles. The time that you own a capital gain can also impact how much you owe in taxes.

How Much Do Small Businesses Pay in Taxes by State?

In addition to federal income taxes, you’ll likely have state and local taxes. The federal corporate income tax rate is currently 21%, but most states have individual tax rates and rules.

Currently, 44 states and Washington D.C. impose taxes on corporate income. Top rates range from 2.5% in North Carolina to 11.5% in New Jersey.

There are also states that don’t have personal income taxes. If you are in one of the below states, you don’t have to file and pay state income taxes on earnings.

Alaska

Florida

Nevada

South Dakota

Tennessee (on wages)

Texas

Washington (state)

Wyoming

Even though some states don’t have an income tax, they may have other taxes. For example, some states have a gross receipts tax that taxes sales instead of profits. Companies must pay taxes on their total amount of sales, even if they don’t make any profit. Look up your state’s requirements or verify with a tax accountant to comply with the applicable laws.

Small Business Tax Professionals

As a small business owner, filing taxes can be confusing. It can be difficult to understand that tax code and all its complexities. But, with an experienced tax specialist, you shouldn’t have to.

Xendoo is an all-in-one service. We have expert bookkeepers, accountants (CPAs), and tax specialists in-house. Our experts work together on your accounts and know all the tax code changes to file your tax returns accurately. They can also choose the best tax deductions and credits that will save you and your business money.

Our bookkeeping plans come with flat monthly fees, so you know exactly what you’re paying each month. If you want to get personalized advice from our tax CPAs, you can add on tax services for as little as $100 per month. We’ll file your taxes too. Schedule a free consultation to see how we can help your business.

This post is intended to be used for informational purposes only and does not constitute as legal, business, or tax advice. Please consult your attorney, business advisor, or tax advisor with respect to matters referenced in our content. Xendoo assumes no liability for any actions taken in reliance upon the information contained herein.

Tax season can be difficult for business owners, and it’s tough when you don’t know what tax forms to fill out or how. If you have a domestic corporation, then you’ll need to use the IRS Tax Form 1120. Corporations and LLCs that are taxed as corporations must use this form to report their income, tax deductions, and credits.

You can use this guide to better understand the purpose of Form 1120 and what information you’ll need to fill it out correctly.

What is Form 1120?

Form 1120, also known as the U.S. Corporation Income Tax Return, is an IRS form that certain businesses use to file taxes. It helps businesses report their yearly profits and losses to determine their tax liability. Businesses can also use Form 1120 to report the gains or losses from the sale of assets and any taxes due from foreign income.

In addition to Form 1120, the IRS requires businesses to make quarterly estimated tax payments if they expect to owe more than $500 on their tax returns. To remain tax compliant, companies must understand the filing requirements and deadlines.

Who Files Form 1120?

C corporations (C corps) or limited liability companies (LLCs) that choose to be taxed as a corporation file Form 1120. Other businesses, such as sole proprietorships and partnerships, do not file Form 1120. S Corporations must file the IRS’ Form 1120-S instead of the standard 1120.

LLCs have a bit more flexibility regarding taxes. They have three tax options—corporation, partnership, or disregarded entity. By default, the IRS taxes LLCs as a partnership when there are two or more owners (multi-member LLC).

If there is only one owner (single-member LLC), then for tax purposes, the IRS doesn’t separate the business from the owner. The owner of the single-member LLC files Form 1040. They must attach Schedule C (Form 1040) to report business Profit and Loss, along with any other required Schedules or forms.

However, a company can choose to be taxed as a corporation instead. If this is the case for your business, then you’ll need to file Form 8832, Entity Classification Election, first. Then, you can use Form 1120.

What You Need to File Form 1120

Now that you understand who must file Form 1120, let’s review what paperwork and records you’ll need for filing. Here is a brief list of what you will need to know:

Business name and Employer Identification Number (EIN)

You should also attach any other required forms or schedules to the form, such as Schedule K-1 for shareholders or Schedule M-1 for reconciling net income with financial statements

You can find most of the information on your financial statements, such as your balance sheet, income statement, and other related documents.

To complete Form 1120 accurately, you can hire a bookkeeper to record your income, expenses, and other financial records for the tax year. They’ll track your receipts, invoices, bank statements, and other business transactions. Once you file taxes, you’ll have all the information you need on hand to fill out the relevant forms.

Start in minutes

Bookkeeping? Taxes? CFO services?

Our bookkeeping and accounting experts keep your books clean, organized, and on time, every time.

There are two ways to file Form 1120: online or by mail. Online or e-filing is the fastest and most accurate way to submit your tax return. You’ll need a copy of Form 1120 that you completed and any required attachments like Schedules and forms. Alternatively, you can mail a copy of Form 1120 with any required payment and attachments to the IRS.

Filing corporate taxes may be confusing, especially for larger businesses that need to consider depreciation, business expenses, and tax credits. Business tax services with CPAs can file all the tax forms for you, on-time and error-free.

Form 1120 Page 1

Page 1 of Form 1120 reports your income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). Information on this page includes:

Business name, contact information, and address – You will need to provide the full name and address of the corporation, as well as the name and title of an officer or responsible party.

Employer Identification Number (EIN) – This is a unique nine-digit number assigned by the IRS to identify your business for tax purposes.

(Line 11) Total gross income for the tax year – This includes income from sales, services, investments, and other sources.

(Line 27) Total deductions – Any expenses your business can deduct from its total gross income on Form 1120.

(Line 30) Total taxable income – You can calculate this by subtracting your deductions from your total gross income.

Tax payments made during the tax year – This includes any estimated taxes paid, any balances due from prior years, and other special payments.

Schedule C

Schedule C of Form 1120 reports any dividends or special deductions the corporation has taken.

On Schedule C, you will need to report dividends the corporation paid to shareholders during the tax year. Dividends are distributions of the corporation’s profits to its shareholders. They may be taxable or tax-exempt, depending on the type of dividend and the shareholder’s tax situation.