As a small business owner, understanding that financial risk management is essential to ensure the long-term success and sustainability of the business well into the future is paramount. By understanding and actively mitigating financial risks, businesses can safeguard their assets, maintain stability during economic fluctuations, and seize growth opportunities. Examples of financial risks, such as economic downturns and unexpected customer behaviors, among many others, can be most detrimental to the operation of a small business if not managed accordingly. Other necessities of financial risk management for a small business include its broader view concerning the potential dangers it may face in operation, particularly the threat of economic uncertainty, market volatility, natural disasters, operational risks, and unpredicted changes in customer demand.

Business Risk Assessment

Building a successful small business requires strategic foresight and the ability to mitigate potential threats. This is where business risk assessment becomes crucial. It’s a comprehensive process that identifies, analyzes, and evaluates potential risks that could impact your financial stability and operational continuity.

This assessment goes beyond generic factors, delving into market trends, economic indicators, operational vulnerabilities, and external threats. By integrating this process into your financial risk management strategy, you gain valuable insights into the broader business environment and, more importantly, the unique risks specific to your company.

This proactive approach empowers you to fortify your business against the inherent uncertainties of the market. It’s the foundation for cultivating a robust risk management culture, leading to long-term stability and growth.

You can minimize potential financial disruptions by leveraging sound risk assessment principles and implementing effective risk management strategies. This allows you to navigate a dynamic business landscape confidently, build financial resilience, and achieve sustainable growth.

In essence, a proactive business risk assessment empowers you to take control of your future and steer your small business toward long-term success.

Small Business Risk Strategies

1. Diversification of Revenue Streams

Diversification of the revenue stream is one critical strategy a small business should pursue in financial risk management. Depending on one product or service is a great risk, as it may expose the business to great risks, market fluctuations, or changes in consumer demand. This could be further expanded by offering another or a new segment of customers. Business risk assessment and business risk strategies in place should include revenue diversification. This will go a long way to ensure these small enterprises enjoy financial stability and continuity.

2. Building Emergency Funds and Contingency Plans

Small business owners seeking to better their financial risk management would do well in that area to reach emergency funds and contingency plans. Reserving money to get through unexpected financial challenges while trying to hedge off the possibilities of incidents ranging from economic downturns to natural disasters is part and parcel of such a process. Consequently, having a clear contingency in place enables businesses to respond in the best and quickest way to minimize potential financial risks better. would be necessary to make a strong assessment of business risks and make strategies for small business risks, like making an emergency fund and making the contingency plan compulsory for small enterprises to strengthen their financial stability. By doing this, the small business owner would be better prepared for different financial risk possibilities and have a better resistance level in the changing business environment.

3. Strategic Financial Planning and Forecasting

Small businesses need to be strategic about their financial planning and forecasting. Proper planning and forecasting of small businesses can get huge benefits since this allows owners to project future cash flow and simultaneously make proactive decisions in managing financial challenges within robust business risk assessment and small business risk strategies. Moreover, effective financial planning will allow the business to allocate resources wisely, creating an approach toward prioritizing practical risk management initiatives. When these risk management small business strategies are integrated with the main financial planning process, the business may build more resiliency to deal with uncertainties more effectively and strategically. This will enable small businesses to lay a good foundation to strengthen their financial stability and develop their long-term success amidst the cutthroat business competition, thus emphasizing the needs of financial planning and forecasting for small business risk management.

4. Insurance and Risk Transfer

The other aspect of financial risk management for small businesses is suitable coverage through insurance. From the various types of property insurance to different liability covers and business interruption insurance, the purchase of appropriate types of insurance can be a major strategy for risk management. Small businesses can thus manage well by covering possible financial burdens through insurance they possess, per the identified risk profiles in business risk assessments and small business risk strategies. This will enable small business owners to strengthen their enterprises against unforeseen financial adversities through insurance and transfer incorporated as a tool for risk management strategies. Proactive management of potential risks in business with comprehensive insurance demonstrates how to apply the principles of financial risk management in reality—bringing back to life the potentialities of small businesses amid many uncertainties prevailing in the business environment.

Conclusion

Effective financial risk management for small businesses is an all-inclusive effort of business risk assessment that merges tailor-made risk management strategies. In their quest for long-term success, which significantly hinges on effective financial risk management, small business owners are bound to adapt to numerous potential threats by being proactive. By conducting effective business risk assessments, small enterprises can gain valuable insights and develop targeted risk management strategies that help strengthen the enterprise against uncertainties through resilience.

Accurate financial records are the bedrock of stability and growth in the intricate web of business operations. Bookkeeping, a process encompassing the recording, organization, and categorization of financial transactions, is the cornerstone upon which informed decisions are made and regulatory compliance is upheld. Yet, amidst its critical significance, myriad challenges often obstruct the seamless execution of bookkeeping duties. In this blog post, we identify and dissect 10 prevalent bookkeeping roadblocks.

Inaccurate Data Entry

Precise data input is fundamental to sound bookkeeping practices. Businesses can overcome this obstacle by investing in automated data entry systems to minimize human error and streamline the process. Implementing double-entry bookkeeping enhances accuracy and error detection. Regular data audits proactively identify and rectify inaccuracies, ensuring data integrity. Addressing inaccurate data entry through these measures establishes a robust foundation for bookkeeping, emphasizing the importance of accurate financial records for informed decision-making and regulatory compliance. Prioritizing accuracy in data entry is crucial for sustained financial health and operational efficacy amidst bookkeeping roadblocks.

Incomplete Records

Implementing a standardized record-keeping system is essential to address this roadblock. Regular audits should be conducted to identify and rectify any inconsistencies, ensuring the completeness and accuracy of the records. Additionally, leveraging modern bookkeeping software can streamline the record-keeping process, enabling businesses to maintain comprehensive, error-free records. By adopting these practices, businesses can overcome the challenge of incomplete records, thereby enhancing the reliability of their financial data and facilitating informed decision-making.

Lack of Standards

Overcoming the challenge of a lack of standards in bookkeeping is pivotal for operational integrity. Establishing clear and defined bookkeeping standards and procedures is crucial. Organizations can maintain consistency and accuracy in their bookkeeping practices by defining standardized procedures, providing comprehensive training for adherence to these standards, and conducting regular quality checks. Addressing this roadblock ensures uniformity and reliability in financial record-keeping, ultimately supporting informed decision-making and regulatory compliance. Improving standards within bookkeeping processes is central to establishing a strong foundation for efficient financial management and reporting.

Template Design

template design in bookkeeping is essential for effective record-keeping. User-friendly and comprehensive templates are crucial for accurate data entry and efficient financial management. Businesses can invest in professionally designed templates or customize existing ones to align with their specific requirements, ensuring optimal functionality and relevance. Organizations can streamline their bookkeeping processes by enhancing template design, minimizing errors, and improving overall efficiency. Investing in well-designed templates is key to overcoming this roadblock and establishing a strong foundation for reliable financial record-keeping.

Training

training in bookkeeping is essential for maintaining efficient and accurate financial processes. Comprehensive training programs for all bookkeeping staff are crucial to ensure proficiency in data entry, financial analysis, and compliance. Organizations should prioritize ongoing skill development opportunities to keep pace with evolving industry standards and technologies. By investing in proper training and continuous skill development, businesses can equip their bookkeeping staff with the knowledge and expertise necessary to navigate complexities and effectively contribute to the organization’s financial health. Overcoming inadequate training as a roadblock underscores the importance of a well-trained workforce in maintaining robust bookkeeping practices.

Complex Accounting Systems

Complex accounting systems present challenges, potentially leading to confusion and errors. To address this, simplify systems when possible, invest in user-friendly software solutions, and provide extensive employee training. By simplifying processes and leveraging user-friendly software, businesses can streamline their accounting practices and minimize the risk of errors. Moreover, comprehensive training ensures that employees are proficient in navigating these systems, ultimately enhancing efficiency and accuracy in financial management. Overcoming the roadblock of complex accounting systems is essential for maintaining robust bookkeeping practices and ensuring accurate financial reporting.

Limited Software Features

Outdated and limited software can impede bookkeeping progress. To overcome this challenge, businesses should consider investing in modern bookkeeping software with robust features tailored to their needs. Upgrading to software that aligns with the business’s requirements enhances efficiency and accuracy in bookkeeping processes. Organizations can streamline financial management, mitigate errors, and adapt to evolving industry standards by leveraging modern software with advanced features. Overcoming the roadblock of limited software features is crucial for maintaining effective bookkeeping practices and ensuring reliable financial record-keeping.

Insufficient Resources

sufficient resources in bookkeeping is crucial for maintaining efficient financial management. Ensuring the bookkeeping team has adequate resources and support, such as additional staff when needed, updated technology, and access to external support when needed, is essential. These resources enable the team to handle their responsibilities effectively and adapt to evolving needs. By providing the necessary resources, organizations can bolster their bookkeeping practices, enhance productivity, and minimize the risk of errors. Overcoming the challenge of insufficient resources is pivotal for sustaining robust bookkeeping processes and upholding the accuracy of financial records.

Outdated Methods

Outdated bookkeeping methods can hinder efficiency. Investing in modern technology and automating repetitive tasks helps streamline processes. Staying updated with industry best practices ensures compliance and operational effectiveness. By embracing modernization and automation, businesses can overcome the roadblocks of outdated methods, paving the way for improved accuracy and efficiency in their bookkeeping practices.

Conflicting Priorities

Conflicting priorities may lead to not paying attention to bookkeeping tasks. To address this, allocate dedicated time for bookkeeping, emphasize its importance within the organization, and communicate its relevance to all staff. By prioritizing bookkeeping tasks and underscoring their significance, businesses can ensure that financial matters receive the required attention, minimizing the risk of oversights or errors. Effective time allocation and clear communication of priorities help overcome the roadblock of conflicting priorities, reinforcing the importance of consistent and accurate bookkeeping practices within the organization.

Conclusion

By recognizing these roadblocks and taking proactive measures, businesses can navigate their bookkeeping challenges effectively, leading to smoother operations and better financial health. By leveraging Xendoo ‘s cutting-edge solutions and expert guidance, businesses can confidently surmount the hurdles of inaccurate data entry, incomplete records, and other common roadblocks. Implementing these strategies can pave the way for more reliable bookkeeping practices, providing a solid foundation for business success. Addressing these common roadblocks, head-on can contribute to improved accuracy, efficiency, and overall financial well-being for any organization. Together, let’s embark on a journey of financial excellence with Xendoo.com as our trusted partner, unlocking the path to operational efficiency and sustained success.

In today’s rapidly evolving business environment, more than merely relying on innovation and agility is required to maintain a competitive edge; it necessitates real-time insights and data-driven decisions. Efficient bookkeeping and accounting are not mere administrative tasks for growing businesses but are strategic pillars for success. Real-time financial management empowers businesses to make informed decisions promptly, manage resources effectively, and adapt swiftly to market changes. By embracing real-time bookkeeping and accounting practices, businesses can comprehensively understand their financial health and position themselves for sustainable growth. Tailoring these practices to meet the specific needs of expanding enterprises further enhances their effectiveness, enabling businesses to navigate complexities and seize opportunities confidently. In this blog post, we delve into the significance of real-time financial management and explore how it can be customized to fuel the success of growing businesses.

The Need for Real-Time Insights

The need for real-time insights in financial management must be balanced, particularly in today’s fast-paced business landscape. Traditional bookkeeping and accounting methods, characterized by manual entry and periodic updates, are ill-equipped to meet the demands of rapidly evolving environments. While suitable for small businesses with limited transactions, these approaches falter when providing timely information crucial for decision-making.

Real-time bookkeeping and accounting offer a paradigm shift by providing continuous monitoring and instant access to financial data. This enables businesses to enhance decision-making processes significantly. With up-to-date financial information readily available, stakeholders can assess cash flow, evaluate performance, and identify growth opportunities promptly. Real-time insights empower business owners and managers to act swiftly and decisively, gaining a competitive edge in the marketplace.

Moreover, real-time financial management improves overall financial control and resource allocation. By tracking income and expenses in real time, businesses can proactively identify trends, manage cash flow effectively, and allocate resources optimally to support growth initiatives. This proactive approach enhances financial stability and resilience, mitigating risks associated with volatile market conditions.

Additionally, real-time accounting fosters adaptability, a critical factor for survival in today’s dynamic market landscape. Businesses can monitor market fluctuations, respond to emerging trends, and adjust strategies promptly based on real-time data. This agility enables businesses to stay ahead of the competition, capitalize on opportunities, and mitigate risks effectively.

In essence, adopting real-time bookkeeping and accounting practices represents a strategic imperative for businesses seeking sustainable growth and competitiveness. By leveraging real-time insights and tailoring them to their specific needs, businesses can confidently navigate uncertainties and capitalize on emerging opportunities in an ever-changing business environment.

Tailoring Solutions for Growing Businesses

While real-time bookkeeping and accounting benefits are clear, implementing these practices requires careful planning and customization, especially for growing businesses, without encountering common bookkeeping roadblocks. Here are some strategies to tailor solutions to their specific needs:

Scalable Systems:

When selecting accounting software, prioritize scalability. Opt for platforms offering flexible pricing and advanced features to adapt to growing transaction volumes and complexity. Scalable systems ensure your financial management tools can seamlessly expand alongside your business, preventing bottlenecks and inefficiencies as operations evolve. Investing in software that accommodates your company’s growth trajectory establishes a foundation for sustainable scalability, enabling smoother transitions and enhanced performance as your business flourishes.

Customized Reporting:

Customized reporting is pivotal for businesses, allowing them to develop tailored reports and dashboards aligned with their objectives. Personalized reports offer invaluable insights, whether it’s tracking key performance indicators (KPIs), monitoring departmental expenses, or assessing profitability by product lines. By providing relevant data in a format that suits decision-makers’ needs at every level of the organization, customized reporting enhances understanding and facilitates informed decision-making. It empowers businesses to identify trends, pinpoint areas for improvement, and capitalize on opportunities, ultimately driving efficiency and success.

Integration with Business Tools:

Integration with various business tools is pivotal for maximizing efficiency. Businesses create a unified ecosystem where data flows effortlessly across departments by seamlessly connecting accounting software with CRM platforms and inventory management systems. This integration minimizes manual errors, eliminates duplication of efforts, and enhances overall operational efficiency. For instance, sales data from the CRM can seamlessly sync with accounting records, providing real-time insights into revenue generation. Similarly, inventory updates can be automatically reflected in financial reports, facilitating accurate cost management. Such integration streamlines processes and empowers businesses to make data-driven decisions confidently.

Professional Support:

Collaborating with accounting specialists catering to growing businesses is invaluable. Their expertise aids in establishing robust accounting procedures, interpreting financial data accurately, and integrating best practices to foster business expansion. With their guidance, businesses can navigate financial complexities confidently, ensuring compliance and optimizing resource allocation. Partnering with seasoned professionals enhances financial management efficiency and empowers businesses to make informed decisions crucial for sustained growth.

Conclusion

In conclusion, adopting real-time bookkeeping and accounting through platforms like Xendoo.com signifies a transformation in financial management for businesses. By embracing these practices and customizing them to their unique requirements, growing enterprises position themselves advantageously in the dynamic market environment. The advantages are diverse, ranging from the ability to make swift, data-informed decisions to enhancing financial control and adaptability. As technology progresses, prioritizing real-time insights becomes increasingly critical. Businesses that integrate these practices ensure their survival and pave the way for sustained growth and competitiveness. In essence, real-time financial management isn’t just a trend but a strategic imperative for businesses striving to thrive amidst constant change and uncertainty in today’s business landscape. Leveraging platforms like Xendoo.com facilitates seamless integration of real-time financial data, further enhancing the efficiency and effectiveness of financial management processes.

Running a small business means juggling lots at once, but quite possibly, the most important one is keeping meticulous financial records. Bookkeeping is an essential part of organized financial management and paves the way for the business to maneuver through the complications of financial control. However, with all these activities, the primary activity that usually goes unsung by an entrepreneur is bookkeeping. It is not just a recording of transactions but the creation of a system of openness and accountability towards finances. Without the right approach and right tools, however, of reliable accounting software such as Xero, QuickBooks, or is important and will turn cumbersome work into swift and effective procedures. These platforms help businesses with monotonous tasks, keep a record of expenses easily, and help develop elaborative financial reports, which makes it like a roadmap for success for small businesses.

Neglecting Reliable Accounting Software

Failing to invest in sound accounting software is a regular oversight with small businesses. Buying systems such as Xero, or QuickBooks, provide benefits to different aspects of your business, ranging from mere bookkeeping activities to expense tracking. This measure translates to the software facilitating the financial process that includes invoicing, tracking expenses, and reconciling bank records by saving time and effort. Second, the provision of detailed financial reports at the touch of a button is invaluable and, in return, empowers one with the decision-making processes within the business. It only means that these kinds of software are integrated into business operations and, therefore, enable accurate records and analysis of transactions related to finance.

Failure to Establish Dedicated Business Accounts

The most common error of small businesses is mixing the finances of a business and personal finances. Without a clear separation of business accounts, finances may be mixed up, possibly leading to distorted bookkeeping and clear visibility of where your business stands. It is critical to have dedicated business accounts, where entrepreneurs streamline their finances and bolster credibility and trust within the marketplace. Clear separation of personal and business finances leads to compliance and sound tax reporting and lays a solid foundation for financial health and growth.

Irregular Reconciliation of Accounts

Consistently reconciling bank and credit card accounts would seem a rather mundane exercise in maintaining financial integrity, but it is one of the most important. Regular checks help ensure that the financial records reflect the true picture of your business’s finances, and minimizes the risk that an error or discrepancy will go unnoticed. It also considers any possible financial pitfalls in discovering irregularities or unauthorized transactions in good time. Timely reconciliation presents a clear view of the cash flow so proactive decision-making may increase, ensuring visibility in financial matters.

Disorganized Financial Records

Good bookkeeping largely depends on the systematic organization of financial records for small businesses. A systematic approach toward invoices, receipts, bills, and other important documents is paramount for small businesses. An organized set of financial records will give business owners easy access to important information within a very short time. This measure could easily avoid the risk of negligence of critical financial data and improve the efficiency in the overall financial management process of any business

Inadequate Expense Tracking

Lack of proper expense tracking is a major issue for most small businesses, it leads to spending patterns getting obscured and potential lost opportunities to optimize finances. Inefficiencies and lack of visibility may affect business profitability without a proper expense categorization system. A good expense tracking mechanism ensures that companies know the cost areas where savings could be made, resulting in saving costs in several areas and budgeting accordingly to allow businesses to make informed decisions.

Ignoring Cash Flow Monitoring

Monitoring cash flow regularly is necessary to maintain the financial stability of small businesses. Cash flow influences almost every activity in an organization, from day-to-day expenses to long-term investments. Lack of cash flow visibility in this area means that the business may be asleep at the switch when unforeseen opportunities strike or financial crises. This technique paves the way for making proactive decisions and making strategic plans once the financial health of the business is highlighted.

Invoicing Best Practices

Efficient invoicing is more than sending out bills and is really about ensuring smooth sailing processes so that all payables are made on time, leading to good client relationships. Invoice automation through online software allows for organization and ease of the invoicing process, streamlining the workflow and removing any friction that billing may have. Automated processes can then follow up on the status of overdue invoices, allowing faster collections and lessening the risk of a gap in cash flow.

With robust strategies and modern services like Xendoo, businesses will avoid complexities in managing finances. With Xendoo, you have access to a dedicated team of financial experts ready to assist you with your bookkeeping and accounting needs. Our innovative solutions ensure the accuracy and organization of your books, reducing errors and discrepancies. From monthly bank reconciliation to the meticulous tracking of expenses, Xendoo offers services that relieve the time and stress involved in managing finances for your company, leaving you more time to work on growth for your business. Schedule a free consultation today to find out how Xendoo can free up your time so you can do what you love and grow your business.

In today’s fast-evolving business world, digitizing financial processes has become imperative for competitiveness and managing financial health. All the tools and approaches with modern technology presented for keeping books enable an owner of a business to make decisions well-informed. Here are ten tips and tactics for innovative digital bookkeeping strategies and insights on how Xendoo will address your financial needs.

1. Embrace Cloud-Based Accounting Software

The benefits of migrating to cloud-based accounting software for small businesses are tremendous. Some platforms, such as Xero and QuickBooks Online, allow real-time access to financial data from practically any device that can get online. Intuitive user interfaces and automation features handle routine tasks like invoicing, expense tracking, and financial reporting. They may also integrate smoothly with other business applications to improve efficiency and productivity.

2. Utilize Digital Receipt Management

Digital receipt management solutions revolutionize the way businesses handle expenses. Receipts captured through a smartphone camera in apps such as Receipt Bank and Expensify ensure that they are automatically extracted with all the needed details to categorize and reconcile expenses. Going digital with receipts would ensure that paper clutter is eradicated, manual data entry errors are reduced, and processes on reimbursing employee expenses are made smoother and more manageable.

3. Implement Automated Bank Feeds

Automated bank feeds make reconciling transactions from the bank and credit card statements with the accounting software much easier. One would be able to sync financial data from bank accounts directly and, in this regard, do away with manual data entry with reduced errors and ensure records are exact. Feeding the information into the accounting software by the automated bank feeds would prompt the accurate and real-time retrieval of all information regarding transactions from the bank. Reconciliations are facilitated, saving the company time and effort on behalf of the business owners and accounting staff.

4. Explore AI-Powered Bookkeeping Solutions

AI bookkeeping-powered solutions operate via machine learning algorithms to do repetitious work and provide insightful data about financial performance. They help classify transactions, detect anomalies, and even customize reports, making bookkeeping more efficient. Leverage the power of AI to do away with manual intervention, reduce errors, and make some strategic decisions.

5. Adopt Digital Payment Solutions

Digital payment solutions like PayPal, Stripe, and Square offer numerous business advantages, including faster payment reception, less paperwork, and better cash flow management. Accepting payments speeds up the process of invoicing and quickens receivables when done digitally, increasing liquidity for the business. Moreover, these digital payment solutions are easily connected with accounting software and impact transaction reconciliation, providing a clearer real-time picture of the financial position.

6. Leverage Blockchain Technology for Transparency

Blockchain technology offers a decentralized and transparent ledger system that can change financial record-keeping. Applying blockchain-based platforms will help increase the security level of financial transactions and bring out transparency and immutability. Blockchain technology can increase tamper-proof record-keeping, decrease fraud risk, and ensure the integrity of all available data. More importantly, the ability of blockchain solutions to offer real-time visibility into transactions makes it possible to track assets, simplifies auditing procedures, and creates trust among the relevant parties.

7. Implement Multi-factor Authentication for Security

Multi-factor authentication is one of the core security measures in the wake of growing cybersecurity threats. This security measure has to be implemented since it requires so many levels of identification of one’s self by a person before access to an account or system is granted. MFA reduces the risk of unauthorized access, data compromise, and financial fraud. Apart from the increased compliance with the regulatory bodies, MFA also increases the confidence of the customers and stakeholders.

8. Stay Abreast of Regulatory Changes

Regulatory compliance remains a moving terrain for businesses in the digital era, which they must keep a keen eye on, whether it concerns tax laws, accounting standards, data privacy, or the delivery of goods and services. Being updated on regulation changes really is a long way to helping businesses make sure they are legally compliant, take minimal risks, and do not attract penalties, which could be very costly. This notion means ensuring the proper up-to-date information is received from government agencies, industry associations, and legal experts and seeking professional guidance occasionally.

9. Leverage Data Analytics for Insights

Data analytics helps businesses get insights into financial performance, identify trends or patterns, and identify key performance indicators. In return, the analysis of financial data equips one with the basis that they can make well-informed decisions, optimize processes, and boost growth. Using advanced features of data analytics tools like predictive modeling, trend analysis, and scenario planning will help businesses anticipate changes in the market and build new opportunities out of them. Further, data-driven decision-making would instill innovation and agility. Hence, businesses remain fitter for the long haul in the digital economy.

10. Invest in Continuous Learning and Development

As technology continues to evolve, investments in the continuous learning and development of business managers should be made to keep in line with the developments. This measure involves going to workshops, webinars, and online courses that expand one’s knowledge and skills in the digital way of keeping books. In addition, businesses have to support employees in certification, areas of personal development, and training related to the industry. Investments in continuous learning and development kindle the culture of innovation, adaptability, and excellence that makes the business relevant to the dynamic digital space.

Embracing modern bookkeeping solutions can transform how you manage your business finances. Equipped with such few tools, which include dependable accounting software, dedicated business accounts, and proactive financial practices, your business will be well set, ready, and positioned for success in this era of the digital age. From expert bookkeeping to financial management, xendoo is with you every step of the way. It involves staff dedicated to handling your business books, accountants, and CPAs with a complete package for you. From preparing and reconciling monthly statements to detailed expense management and tax preparation, xendoo has you covered with professional, expert oversight. Schedule a call with xendoo today and take the first step toward ensuring a brighter financial future for your business.

We share your passion for small businesses and are inspired by your dedication to making your dreams a reality. That’s why we’re committed to providing you with the financial visibility and support you need to thrive.

More Than Just Numbers

It’s more than simply crunching numbers. It’s about building meaningful relationships with our clients and understanding their needs. Our people-first mentality ensures you receive personalized attention and expert guidance throughout your financial journey.

A One-Stop Solution

Xendoo offers a comprehensive suite of services, including:

Full-service bookkeeping and accounting team to free up your time and resources.

Hassle-free tax preparation and filing

Fractional CFO Services to work with you on a roadmap of future growth

A dashboard that provides real-time financial insights

Passionate about your success?Xendoo is, too. We provide the financial visibility and support small businesses need to thrive and scale. Let us handle the financial burden so you can focus on what matters most – running your business and achieving your goals.

Contact Xendoo today and discover how we can give you time back to grow your business.

Running a small business comes with many responsibilities, but some of the most vital duties are keeping good and accurate records. Bookkeeping is such a critical function to keep the proper administration of business under control, and by adopting the right strategies, you can always ensure that things will be in order. Understanding the reasons for bookkeeping is essential as it provides a clear framework for the financial management of your business.

1. Leverage Reliable Accounting Software

Small businesses need to leverage this reliable accounting software not just to keep their books in order but to empower them to manage their finances accurately and with ease. With tools like Xero, QuickBooks, FreshBooks, and many other accounting software, managing finances becomes an enjoyable process from what could be otherwise a tiring one. Most of the daily mundane work like invoicing, tracking expenses, and reconciling the bank would be handled through these platforms, thus freeing time for business owners to concentrate more on growth strategies. Also, prepare detailed financial reports in the blink of an eye, giving valuable insights into the financial health of your business on which to base judicious decision-making. Consequently, by incorporating such software into your typical day’s work, you can be assured that every financial transaction will be recorded and analyzed accurately and is ready for review, which will act as a good foundation for your business’s financial success.

2. Establish Dedicated Business Accounts

The first step to professionally organized financial management is to have a separate account for the business. By so doing, the separation of business monies from personal money is drawn, and it is well defined. It helps not just in ease of management but also in keeping the financial regulation, which, otherwise, may get entangled in a complicated way if found intermingling with personal and business transactions. Further, keeping separate books assures the business is well prepared for the tax filing, as there will be a proper account of income and expense concerning the business, thus little probability of mistakes and variances in the reports filed. Ultimately, dedicated business accounts are instrumental in establishing credibility and trust with financial institutions and within the broader market, setting a solid foundation for financial health and compliance.

3. Regular Reconciliation of Accounts

Reconciling your bank and credit card accounts regularly is one of the important practices in ensuring that your financial records are accurate. It would help identify differences or errors to maintain the integrity of the financial data. Timely reconciliation helps identify unauthorized transactions and sometimes even fraudulent activities.

4. Organize Financial Records Systematically

Proper bookkeeping will be most dependent on how your financial records are organized. You should develop a systematic plan whereby invoices, receipts, bills, and other documents will be arranged. This is a scenario that will aid you in keeping records of financial data in an organized manner and getting them when they are needed with less trouble.

5. Categorical Expense Tracking

Organization of your business expenses is necessary for properly gathering insights related to your spending trends and to ensure that you optimize your budget appropriately. Expense categories help you organize where your money goes, and they help you find more opportunities to save on costs and optimize deductible business expenses.

6. Vigilant Cash Flow Monitoring

Monitoring your business’s cash flow regularly lies at the crux of the movement of money in and out of your operations. A clear picture of your cash flow would enable you to make sound decisions and foster your business’s financial health.

7. Implement Invoicing Best Practices

Invoice billing processes are important for timely payments from your clients and customers. Some online invoicing software would help you automate the process and easily send professional invoices, hence letting you easily track the payment status.

8. Stay Tax-Ready Throughout the Year

Be tax-ready at all times. Keep good records, and be informed about the tax deductions and credits available to your business. Staying informed will ensure proper compliance with tax regulations and, at the same time, make sure that tax savings are maximized for your small business.

9. Understanding Financial Statements

Interpreting your business’s financial performance involves developing a basic understanding of essential financial statements, including the profit and loss statement, the balance sheet, and the statement of cash flows. All these statements give insight into how profitable your business is, how liquid it is, and how financially healthy it is.

10. Seek Professional Guidance

It is best to consider consulting with professionals, such as bookkeepers or accountants, based on your organization’s needs to assist in optimizing both your processes for bookkeeping and in managing your finances. Professional consultants’ support can help understand the intricacies of financial matters, unlock maximum tax advantages, and ensure financial accuracy.

What Can Xendoo Do for You?

All of the above 10 important tips and strategies on small business bookkeeping are bound to have you equipped with enhanced accuracy, better insight into the financial status, and, in turn effectively managing your business finances. Bookkeeping is much more than just compliance; it’s a tool that gives you an understanding of the financial health of your business and empowers you to make knowledgeable decisions. At Xendoo, we understand the sophistication with which bookkeeping and financial management for small businesses need to be done.

You have at your disposal a dedicated team of experts with innovative solutions that make it possible to keep your books well-organized, ensure that you are never found wanting in terms of taxes, and leave you with only one job that ultimately defines your business success. Xendoo wants to bring down your stress levels and help put more money in your pocket—with real people and real bookkeepers who focus on your financial well-being. Let Xendoo take care of the complexities of bookkeeping and free up your time to give more attention to what you love. Schedule a call with Xendoo today to get your bookkeeping and tax prep more aligned with the modern day. Xendoo could be the ticket to a much better bookkeeping setup for your business.

The biggest rule of thumb when running a company is to keep your personal and business finances separate. To do that, you need to choose the best business bank for you, which may not be the same one you use for your personal finances.

Business bank accounts have different terms and benefits than personal accounts. As an online accounting service, Xendoo works with many companies and business banking services.

The best business bank for you depends on your particular needs. But there’s much more to consider. Some banks are stronger in commercial lending, while others have stronger lines of credit.

We’ll compare the best business banks and their features to help you decide which options are right for you. Review each bank’s rates and services to determine which suits your needs.

Wells Fargo

Chase

Bank of America

Mercury (for global and online-specific companies)

Citibank

Capital One

PNC

US Bank

TD Bank

Cogent Bank (or similar regional banks)

How to choose a bank for your business

Choosing a bank is a big decision in your business journey. However, there’s no one-size-fits-all business banking solution. Factors like your monthly revenue, number of cash payments, and company structure (LLC, S corp, C corp, etc.) will influence which features you need most. You may also want to get startup funding or a loan from the same place you do your banking.

Although these factors may vary, there are some criteria all companies should look at when choosing a banking partner. Here are the features we looked at to evaluate the best business banks.

View-only access, wires, and online banking

As a baseline, all business banks must have robust technology to support VOA (view-only access), wires, and online statements. You can share view-only access to your bank statements with bookkeepers, accountants, and other trusted financial partners. They’ll only be able to view, not make changes to, the data they need to record and manage your finances.

Fees and costs

Some banking services come with fees and financial requirements that might not be obvious at first. Common banking fees include:

Transaction limits and fees

Monthly account maintenance fees

Deposit limits and fees

Opt for a bank that provides transparency in its fee structure and offers the best value.

Annual Percentage Yield (APY)

In simple terms, APY is how much an account can earn in a year through interest. However, it’s not the same as interest rate because it also includes compound interest.

For example, let’s say you open an account with 1% APY and your first deposit or principal balance is $20,000. Then, every month you deposit another $20,000. Instead of only earning interest on the original amount, compounding interest factors in the updated account balance.

In-person locations

If you run an online business and rarely have cash transactions, a bank with in-person locations might not be a priority for you. Instead, it might be more convenient to look for online banking solutions.

If you have cash transactions, which is common with franchises, retail stores, and restaurants, physical bank locations are more important. You might need to make frequent cash deposits and prefer in-person service.

10 Best business banks

Whether you’re considering switching banks or starting a business checking account for the first time, you can compare features, fees, and more below.

1. Wells Fargo

Best for: Companies that want loans, business checking, and in-person banking.

Wells Fargo is one of the oldest banks in the United States. However, its reputation has taken some hits in recent years. But, that also means that it is under heavy scrutiny from regulators and is focused on regaining consumer trust.

Monthly fee: $10-$75 per month

Minimum deposit requirement: $25

Transaction limit: 100-250 monthly

Deposits: $5,000-$20,000 fee-free cash deposits

APY: None

Member FDIC: Yes

ATMs: Over 12,000 ATMs in 40 states

Overall, Wells Fargo has a huge physical presence, which might be a fit if you value in-person banking. But, its past actions and high fees for overdrafts, transactions, maintenance, and more make it less than ideal.

Pros

Cons

Physical locations in over 40 states

High monthly fees and other costs

You can open an account online

No free checking accounts

2. Chase

Best for: Companies of all sizes that want a wide range of business and personal financial services (checking, savings, financing, mortgage, etc.)

Chase offers many types of business banking accounts to suit different business sizes and needs. Let’s take a closer look at each in the comparison below.

Business Complete Banking

Performance Business Checking

Platinum Business Checking

Monthly fee

$15 (waived with $2,000 minimum balance)

$30 (waived with a $35,000 minimum average balance)

$95 (waived with a $100,000 minimum average balance)

Chase has locations in over 29 states and over 16,000 ATMs. It might be convenient if you need in-person banking and already have a personal banking account.

If you have a lot of monthly transactions or don’t want to worry about banking fees, then Chase isn’t the best business bank for you.

Pros

Cons

Multiple checking account options to suit different business needs

Monthly fees, but they are waived if you meet the account balance threshold

Wide network of branches for in-person service

No APY for business checking

3. Bank of America

Best for: Businesses that have large, monthly cash deposits and need in-person services.

Bank of America has two business banking accounts: Fundamentals and Relationship. The Fundamentals account is more suitable for small-to-medium businesses while Relationship is for larger enterprises.

Each account has various fees and requirements. Here’s the breakdown for the Fundamentals account:

Monthly fee: $16 (waived with $5,000 monthly account balance)

Minimum deposit requirement: $100

Transaction limit: 200 per month

Deposits: Free up to $7,500 and a .30 charge per $100 over

APY: Not available

Member FDIC: Yes

ATMs: Over 4,500 locations and ATMs

Pros

Cons

One of the largest and most established banks

Complicated monthly fees and requirements can mean more expensive banking costs

Branches and ATMs all over the country for in-person banking and cash deposits

4. Mercury

Best for: Growing global and online-only startup businesses.

One of the reasons why Xendoo partners with Mercury is that it’s tech-enabled banking at its finest. Compared to traditional banking platforms, it has an incredibly, user-friendly interface.

It has an API, so businesses can integrate other financial tools and services they use. For example, you can connect bookkeeping, payments, payroll, and more to your Mercury business banking account. This way, it’s easier to keep track of and manage your finances.

It also has Mercury Raise, a program that helps connect startups with investor funding.

You can sign up for a business banking account in 10 minutes.

They also have a non-traditional approach to business loans with Mercury Venture Debt. If your startup has raised venture capital (VC) funds in the past year, you could be eligible. Instead of looking at cash flow and other financial indicators, it looks at your investment team.

Monthly fee: $0

Minimum deposit requirement: $0

Transaction limit: Unlimited, including savings account

Deposits: Unlimited

APY: Up to 5.10% yield with Mercury Treasury (as of writing)

Member FDIC: Yes (up to $5 million)

ATMs: Not available

Pros

Cons

Free checking and savings accounts

No cash deposits

Helps startups with funding through Mercury Raise and its Venture Debt loan program.

It doesn’t accept some businesses (i.e. cannabis or businesses with many cash transactions)

No overdraft fees

You can connect bookkeeping, accounting, payments, and other tools

5. Citibank

Best for: Businesses that maintain a high monthly balance to avoid fees.

Citibank has also been around for a long time, so it has all the basic business accounts and some extras. It has several options for business checking accounts as well as savings accounts, credit cards, loans, and more.

However, it doesn’t have a free checking option. There are monthly fees unless you maintain an average monthly balance over $5,000 to $10,000, depending on the account you use.

Monthly fee: $15-$30

Minimum deposit requirement: $1

Transaction limit: Limited free transactions (250-500 depending on the account)

Deposits: $5,000-$2,000 free cash deposit limit

APY: Not available

Member FDIC: Yes

ATMs: 2,300 ATMs

Pros

Cons

Full suite of business services

All business checking accounts have fees (some are waived with a monthly balance)

Must open an account in-person at a local branch

6. Capital One

Best for: Small businesses that want to build credit and make many purchases with a credit card.

Capital One is most known for its credit cards. However, it also offers personal and business banking services. There are two checking account options: Basic and Enhanced.

One drawback is that each account has monthly fees. Capital One waives them for account balances that average $2,000-$25,000 or more in the last 30 to 90 days. Its basic account also has fees for monthly cash deposits over $5,000. Then, you’ll pay $1 for every $1,000 over.

Monthly fee: $15-35

Minimum deposit requirement: $250

Transaction limit: Unlimited

Deposits: Unlimited

APY: Not available

Member FDIC: Yes

ATMs: Over 70,000 through Capital One, MoneyPass, or Allpoint

Pros

Cons

Business credit cards that offer cash back, travel, and other rewards

No free business checking

Business cards integrate with Quickbooks, Xero, and other accounting software

Monthly fees and cash deposit limits

7. PNC

Best for: Small business owners that don’t have more than X transactions each month.

PNC has a wide range of banking account options. For example, it has specialized accounts for non-profits and law firms. Most organizations, however, will choose from two primary checking accounts for businesses. Here’s a comparison of the features for each.

Checking

Plus

Monthly fee

$12 (waived with a $500 minimum monthly balance)

$22 (waived with a $5,000 minimum monthly balance)

Minimum deposit requirement

$100

$100

Transaction limit

150

500

Deposits

$5,000 cash deposits

$10,000 cash deposits

APY

No

No

Member FDIC

Yes

Yes

PNC has over 2,500 locations and 9,000 ATMs. It has a decent mobile app and in-person services. However, you must go to a PNC location to open an account. Also, some fees like overdraft costs and a monthly fee for direct integrations with Quickbooks and other software can add up.

Pros

Cons

Wide selection of business accounts to choose from, including industry-specific ones

A monthly fee for some software integrations

Strong mobile app

Lower cash deposit and transaction limits

In-person banking services

Monthly fees, but they’re easy to waive

8. US Bank

Best for: Startups that are also interested in easy loans and lines of credit.

US Bank has several business checking account options, including specialty ones for non-profits. Here are the three most popular options and a comparison of each.

Silver

Gold

Platinum

Monthly fee

$0

$20

$30

Minimum deposit requirement

$100

$100

$100

Transaction limit

125

300

500

Deposits

$2,500 free cash deposits

$10,000 free cash deposits

$20,000 free cash deposits

APY

No

No

No

Member FDIC

Yes

Yes

Yes

US Bank has over 4,000 ATMs and branch locations in 26 states. It also offers many business loan options, including SBA and Quick Loans. Quick Loans focus on growing businesses with equipment, vehicle, and other purchases.

Pros

Cons

Includes a wide range of business checking and loan options

Its checking account terms can be difficult to compare

Offers merchant services like payment processing and point-of-sale options for a fee

Monthly deposit limits are low with a complex tracking method

9. TD Bank

Best for: Small businesses that want 24/7 support and more flexible in-person banking hours.

TD Bank has all the bells and whistles you need for a business checking account including mobile deposit, online bill pay, and ACH transfers. You can also apply for loans or lines of credit, but there is a vetting process.

However, like most established banks, it has a monthly fee, so you could be charged if your account doesn’t meet the average monthly balance requirements.

Monthly fee: $10-35

Minimum deposit requirement: $250

Transaction limit: 200-500 free transaction limit

Deposits: $5,000 cash deposit limit for most accounts

APY: 0.05% APY for a business interest-bearing account

Member FDIC: Yes

ATMs: A few hundred (mostly on the east coast)

Pros

Cons

Interest-bearing checking account options

No free business checking accounts

Some banks are open weekends and Sundays

It’s mainly located on the east coast

10. Cogent

Best for: Best bank for local small businesses with complex regulation and banking needs.

Cogent Bank stands out with its commitment to providing customized services. For example, many big banks don’t offer accounts to cannabis companies because of the regulation. However, Cogent provides banking to cannabis and other industries with complex financial needs like blockchain and healthcare.

Another feature that sets Cogent apart is its Insured Cash Sweep® (ICS) service. It splits deposits that are over $250,000—the FDIC-insurable limit—into smaller chunks and sends them to member banks. You get interest-bearing and FDIC-insured cash deposits without the trouble of setting up and managing multiple accounts.

You can open a business banking account with Cogent online within minutes. Most will choose between two checking account options.

Business Checking

Business Edge Checking

Monthly fee

$0

$50 (waived with $50,000 average monthly balance)

Minimum deposit

$0

$0

Transaction limit

200 transactions per month

500 transactions per month

Monthly fee: $0 for business checking

Minimum deposit requirement: $0

Transaction limit: 200-500 transactions per month with a $0.50 charge per transaction over the limit

Deposits: Same as transactions

APY: None

Member FDIC: Yes

ATMs: 8 Florida locations

Pros

Cons

Customized banking solutions

Transaction limits

Experience in highly-regulated industries

There are many business banking options, which can make researching all the features and choosing one a daunting task. Ultimately, the best business bank for you should offer a range of features with few banking fees.

FAQs

Which bank is best for a business account?

The best bank for a business account varies based on your specific business needs. Low fees, high APY, and a range of business-oriented services like merchant services can influence this decision. Researching and comparing the terms of each can help you make the right choice.

How are business and personal checking accounts different?

Business and personal checking accounts differ in terms of fees, transaction limits, and additional services. Business accounts cater to higher volume transactions and provide access to business credit. They also make it easier to manage payroll, invoicing, accounting, and more.

What banks offer free business checking accounts?

Many banks offer free business checking accounts, though conditions may apply. Banks such as Mercury, BlueVine, and Grasshopper Bank provide free checking options, but you should review each bank’s specific terms and conditions, including minimum balance requirements and transaction limits, to ensure it suits your business needs. Many other banks will also waive monthly fees if you meet certain criteria.

This post is intended to be used for informational purposes only and does not constitute as legal, business, or tax advice. Please consult your attorney, business advisor, or tax advisor with respect to matters referenced in our content. Xendoo assumes no liability for any actions taken in reliance upon the information contained herein.

You’ve put your heart and soul into your business. So why does it feel like you’re spinning your wheels, trying to keep up with your core business and your administrative overhead at the same time?

When you first started your company, it might have made sense to try to handle your own bookkeeping and accounting needs. After all, it kept costs down. But it may not have taken long to realize that you could use some help.

Why not rely on an online accounting service to take these tasks off your plate so you can focus on your business?

Today, we’ll take a closer look at the business benefits of online bookkeeping and see how these services can help you to get your head out of the books and back in the game.

Business Benefits of Online Bookkeeping

Traditionally, businesses would hire a staff member to handle their books. They might even consider hiring a full-scale accounting department, depending on the size of their company.

But these days, more and more companies are going digital, opting to use online accounting and bookkeeping services to handle their needs. This is happening for good reasons, as online bookkeeping offers a host of benefits. We’ll explore some of these benefits in depth below.

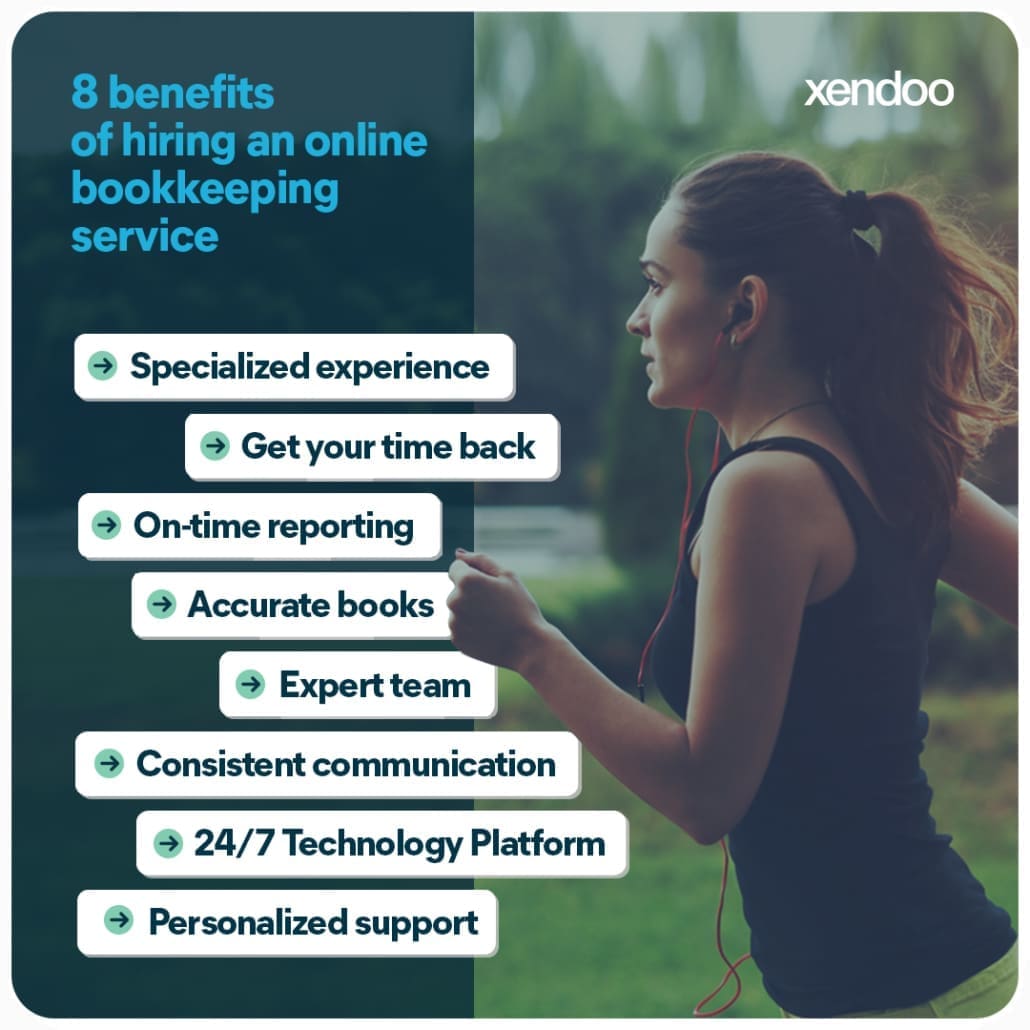

1. Specialized Experience

Today’s businesses require specialists, not generalists. Increased regulation and the unique needs of individual businesses often demand a specialized set of skills. It’s rare that a staff accountant has experience in the kinds of niche areas that your business needs.

Conversely, an online accounting firm can often provide experience in such areas as:

Personal financial planning and assistance

Forensic Accounting

Managerial Accounting

IT auditing

Non-profits

Tax Preparation

Some of these tasks tend to be cyclical, such as your annual tax preparation. It makes sense to consult with an online accounting firm that can provide the services you need when you need them without the overhead of hiring a full-time CPA.

2. Accurate Books and Low Cost

One of the greatest business benefits of online bookkeeping is a reduction in cost.

According to the Journal of Accountancy, the average salary for a full-time CPA is over $100,000 per year. The cost of a full-time bookkeeper is cheaper, but your business may still be looking at paying over $40,000 per year for their services, according to the U.S. Department of Labor Statistics.

Don’t forget that these salaries are only a starting point. Hiring a full-time employee also demands that you provide employment benefits. You may even have to make adjustments to your facilities in order to provide an office or similar workspace.

Time is another factor to consider. Who will be in charge of hiring and managing your employees? Unless you have a human resources department, these responsibilities might fall on your shoulders as the business owner. Sure, hiring a CPA means you won’t be handling the books, but instead, you’ll have the task of hiring an additional employee.

Why swap one responsibility for another, when you can simply outsource your needs to an accounting firm?

Online bookkeeping services can be surprisingly affordable, eliminating the overhead associated with hiring a regular employee.

By relying on an online solution for your financial needs, you won’t have to worry about diverting valuable space to set up an office or workstation,, allowing you to cut costs in every imaginable capacity.

3. On-time Reporting

Staying on top of the details is a full-time job in and of itself. But the more information you have about your business, the better. As a business owner, you want access to trends like:

Losses

Profits

Tax information

Personnel and payroll data

Insurance payments

Procurement

Online bookkeeping ensures that you have access to the latest information, with reports available with unparalleled speed. This data is useful for highlighting areas of your business that could stand to be improved, which is why you need access to these reports in a timely manner. Since these reports are generated online, you’ll also save on paperwork.

In addition to internal reporting, online bookkeeping services can speed up your invoicing process. By streamlining your entire financial department, you’ll be in a better position to send invoices to clients and maintain your overall cash flow.

Faster reporting can accelerate this process even further by monitoring your income and alerting you to clients that have outstanding payments that need to be collected.

In addition, virtual accounting services can help you to manage your inventory. Xendoo, for example, can help you integrate your platforms and inventory with software like Xero, which has a number of basic inventory management features, as well as other third-party platforms that can help you optimize your ability to keep track of your inventory. These tools can be a great help when it comes to keeping your shelves stocked and your orders flowing.

This increased efficiency doesn’t just save you a headache; it can help grow your business, too. Having access to the latest data increases the rate at which you can invoice clients and receive payments.

The data you receive from an online bookkeeper can even help you plan for the future, which can be helpful when it comes to tasks like managing your inventory and looking for ways to expand your business.

4. Accurate Books

While CPAs typically have an advanced degree in addition to their certification, there are no advanced professional standards when it comes to bookkeeping.

That’s not meant to be a slam against bookkeepers, as many of them do an excellent job. But if you try to cut corners by hiring a junior accountant or a financial novice, you could end up with errors creeping into your books. That’s also true if you try and handle the books yourself, especially since it’s unlikely you’ll be able to give your books your full, undivided attention.

Why is accuracy so important? For starters, accurate books can eliminate accounting errors. Maintaining accurate books can be essential for the efficient management of your business.

But when it comes to tax preparation or other financial audits, accuracy is indispensable. Make an error in your tax forms, for example, and your business could be looking at penalties and additional fees that could otherwise be avoided.

Accuracy is one of the top business benefits of online bookkeeping. Accounting firms rely on the best bookkeepers in the industry, which ensures that businesses receive the benefit of meticulous, detail-oriented professionals to handle their books. In turn, this can ensure a smooth process when it comes time to prepare and pay your taxes.

If you’re concerned about the accuracy of your current books, an online accounting firm can perform an audit and troubleshoot your financials, ensuring you’re back on track for an error-free future.

Xendoo offers “catch-up bookkeeping” services that you can rely on to update your books so that you can keep things accurate. This can be particularly helpful for business owners who have been multitasking or ones who need a helping hand to stay current on their financial records.

Ultimately, assigning your bookkeeping needs to an online firm can prevent errors from recurring in the future.

5. Expert Team

Virtual bookkeeping companies rely on the best and brightest bookkeepers that the industry has to offer. But the benefits of this go beyond accuracy and attention to detail. Having an expert team behind you can provide the confidence that your business can grow and that you’ll enjoy the dedicated support you need for any financial change.

An expert team can be counted on to understand the best practices for modern bookkeeping. They will also be familiar with the latest financial software. With these tools, they can provide you with consistent, efficient reporting and expert financial analysis.

These expert-level skills would typically be out of reach for small business owners, as many lack the funds to invest in bookkeepers of this caliber. However online firms can provide you with top-tier care and insight at a mere fraction of the cost of hiring an employee, helping you balance quality and affordability with your financial needs.

6. Consistent Communication

Information is only as helpful as it is available. When you rely on a staff accountant, you’ll typically have access to financial data during normal business hours, which limits you to Monday through Friday from 9 to 5. But what if you need a piece of information when your staff accountant is “off the clock”?

Today’s business world doesn’t operate within the traditional 40-hour workweek. A global economy and a shift toward 24-hour customer service have placed new demands on business owners. You need a solution that matches these needs.

Online accounting firms can fill this need by being available when you need their services the most, offering you consistent, regular communication through email, phone, and other channels.

This kind of streamlined communication may be particularly helpful for business owners who have to travel often. Digital communication solutions can ensure that your accounting staff is right in your pocket, even when you’re out of the office—or even out of the country.

In other words, a virtual financial team never clocks out and never takes a sick day. You can rely on online firms to provide you with the data you need when you need it most, so your business never has to slow down.

7. 24/7 Technology Platform

You’re probably already familiar with software like QuickBooks, but this is just the tip of a larger digital iceberg. Virtual accounting firms have access to the latest digital tools and software packages to help their clients optimize their business.

At Xendoo, we can sync your accounts and optimize your books using the following platforms:

Amazon

TaxJar

Gusto

Stripe

Shopify

Expensify

Bill.com

Of course, this list is always subject to change, which is one of the best business benefits of online bookkeeping.

Virtual accounting firms can take advantage of the latest online bookkeeping features offered in these and other software platforms. Virtual firms also have the resources to keep up with changes in technology.

By adapting and innovating, online accountants can ensure your business can continue to thrive and compete in an increasingly digital climate.

8. Personalized Support

Finally, there is simply no substitute for the personalized, custom support that you receive when you partner with an online bookkeeping service. The days of hiring a one-size-fits-all accountant are over. Modern businesses require the agility and personalization that come from a virtual firm.

An online accounting firm can adjust its areas of specialty to the needs of your business, providing solutions for the usual bookkeeping services as well as solutions for eCommerce, business software integration, and more.

But perhaps most importantly, a virtual financial firm offers an array of services that can be tapped into as your business evolves and grows, so you can have the confidence that you’ll always have access to industry-leading services that are tailored to the needs of your business.

What Can Xendoo Do for You?

Are you ready to experience the business benefits of online bookkeeping for yourself? Why not consider what Xendoo can do for you and your business? Join high-profile businesses like Starbucks and Century 21 in trusting an industry leader to handle your books, prepare your taxes, generate reports, and perform a host of other financial services that are tailored to the unique demands of your business.

Xendoo offers flexible pricing based on the size of your business. We even provide scalable solutions to help your business to grow. Each plan includes standard bookkeeping services, as well as reporting on profits and loss and other data.

Select plans include provisions for tax returns and consulting, which can be invaluable for businesses of any size.

Sign up for our bookkeeping services, and you’ll see how our advanced services can help your business. It’s time to stop handling your own books. Let us handle the details so that you can keep your focus on what matters: Growing the business you love and connecting with the customers you’ve come to rely on.

Running a business is, without a doubt, a challenging task that requires a lot of commitment, effort, and attention to detail. Did you know 82% of small businesses fail due to cash flow management? Besides managing all aspects of the business, taking care of your books is crucial to achieving financial success while being tax ready all year round.

At Xendoo, we know you didn’t start a business to do the accounting and taxes; but we did. In this blog post, we’ll explore the necessity of catching up on your bookkeeping and how it will benefit your company.

To start, let’s look at why keeping your books up to date year-round will help your business.

1. Avoid an audit

Filing your business taxes on time, will avoid hefty fines or legal action and keep your financial health in good shape. Even if you can’t pay in full, the IRS will work with you. By staying on top of your bookkeeping, you avoid further issues and stay on good terms with the IRS and other regulatory agencies.

2. Obtain a business loan

Consistent bookkeeping also makes it easier to obtain a business loan and improves the application process. Up-to-date financials give you a clear picture of your loan needs, so you know how much funding you need.

Lenders want a solid financial history and a clear picture of your current financial health. That way, you increase your chances of securing the funding you need to grow your business.

3. Avoid costly mistakes

Consistent bookkeeping helps you avoid mistakes such as:

Heavy inventory

Inaccurate invoices

Predatory lending options

Accounts receivable and accounts payable errors

An online bookkeeping service that provides 24/7 access to financial experts and reporting all year will alert you to mistakes quickly and even prevent them. It can also help you make objective business decisions that contribute to your success.

4. Identify fraud and errors

Keeping your financial records up-to-date can help you identify potential fraud or errors. Regularly reconciling your bank accounts, credit card statements, and invoices can help you quickly catch any discrepancies and take appropriate action to rectify them. Doing so can protect your business’s financial integrity and prevent losses due to fraudulent activities.

5. Focus on growth, not your bookkeeping

Now that you’ve secured funding for that second location (or that expansion) and got caught up on your books, you can focus on growth. When your books are in order, you can devote your time and energy to other business areas, such as marketing, sales, or product development.

Xendoo makes a great partner whether you need help getting caught up or staying up to date on your bookkeeping.

Achieve financial peace of mind with up-to-date bookkeeping and enjoy the benefits of a healthy and thriving business! For more benefits about keeping your books current and staying on track with your business needs, visit this article.

Small business financing is vital as it can make or break your business. When first starting, there are many factors that you need to consider, such as your business plan and your financing options. When creating your business plan, it should outline your goals and objectives to have a clear idea of how to implement your plan. It’s important to plan ahead so you don’t miss any crucial steps that will bring on more than necessary. In this blog post, we will help you navigate the different types of financial assistance options to give you more insight into what could be a good fit for you.

When it comes to financing, it’s important to ensure that you’re choosing the right option for your business. Starting a small business isn’t easy and comes with many challenges, but if you take the right steps in the planning stage, it’ll make the process go more smoothly.

Without the right financing, getting your business off the ground may be hard because you won’t have enough support behind your idea. There are many financing options available, but it’s up to you to find the one you feel will work the best. Some options to fund your business include a small business loan, personal financing, or even a home equity line of credit loan.

Types of Financing Options

A small business loan can be a good option when looking for some additional financing while keeping in mind small business loans have a long list of requirements that have to be met to qualify for the loan. Cross-check the qualifications beforehand, and if all the requirements are met, it could be a good option for you. If you have been running your business for a while but are trying to qualify for a small business loan, the lender may ask to see a recent balance sheet of your business. It’s important that when applying for a small business loan, you understand the information that you’ll have to present.

Financial statements are one of the many requirements needed to qualify, so it’s important that you understand how to read your financial statements so that you will be able to discuss the information with the lender. If you don’t want to look to outside sources for financing assistance and feel that you have the ability to invest in it yourself, then personal financing may be the best choice for you. Personal financing loans are guaranteed through your personal credit history. This often makes them easier to get approved for than a small business loan if you have good credit, which might look at both a personal and business credit score.

For homeowners, another viable option is taking out a home equity line of credit loan. This type of loan allows you to borrow money against the equity you’ve built in your house. You receive the funds as a line of credit, so you’re able to access additional financing for your business as needed. This could be beneficial as it can be easier to qualify for than other loan options.

Keep your Finances Up to date