The biggest rule of thumb when running a company is to keep your personal and business finances separate. To do that, you need to choose the best business bank for you, which may not be the same one you use for your personal finances.

Business bank accounts have different terms and benefits than personal accounts. As an online accounting service, xendoo works with many companies and business banking services.

The best business bank for you depends on your particular needs. But there’s much more to consider. Some banks are stronger in commercial lending, while others have stronger lines of credit.

We’ll compare the best business banks and their features to help you decide which options are right for you. Review each bank’s rates and services to determine which suits your needs.

- Wells Fargo

- Chase

- Bank of America

- Mercury (for global and online-specific companies)

- Citibank

- Capital One

- PNC

- US Bank

- TD Bank

- Cogent Bank (or similar regional banks)

How to choose a bank for your business

Choosing a bank is a big decision in your business journey. However, there’s no one-size-fits-all business banking solution. Factors like your monthly revenue, number of cash payments, and company structure (LLC, S corp, C corp, etc.) will influence which features you need most. You may also want to get startup funding or a loan from the same place you do your banking.

Although these factors may vary, there are some criteria all companies should look at when choosing a banking partner. Here are the features we looked at to evaluate the best business banks.

View-only access, wires, and online banking

As a baseline, all business banks must have robust technology to support VOA (view-only access), wires, and online statements. You can share view-only access to your bank statements with bookkeepers, accountants, and other trusted financial partners. They’ll only be able to view, not make changes to, the data they need to record and manage your finances.

Fees and costs

Some banking services come with fees and financial requirements that might not be obvious at first. Common banking fees include:

- Transaction limits and fees

- Monthly account maintenance fees

- Deposit limits and fees

Opt for a bank that provides transparency in its fee structure and offers the best value.

Annual Percentage Yield (APY)

In simple terms, APY is how much an account can earn in a year through interest. However, it’s not the same as interest rate because it also includes compound interest.

For example, let’s say you open an account with 1% APY and your first deposit or principal balance is $20,000. Then, every month you deposit another $20,000. Instead of only earning interest on the original amount, compounding interest factors in the updated account balance.

In-person locations

If you run an online business and rarely have cash transactions, a bank with in-person locations might not be a priority for you. Instead, it might be more convenient to look for online banking solutions.

If you have cash transactions, which is common with franchises, retail stores, and restaurants, physical bank locations are more important. You might need to make frequent cash deposits and prefer in-person service.

10 Best business banks

Whether you’re considering switching banks or starting a business checking account for the first time, you can compare features, fees, and more below.

1. Wells Fargo

Best for: Companies that want loans, business checking, and in-person banking.

Wells Fargo is one of the oldest banks in the United States. However, its reputation has taken some hits in recent years. But, that also means that it is under heavy scrutiny from regulators and is focused on regaining consumer trust.

- Monthly fee: $10-$75 per month

- Minimum deposit requirement: $25

- Transaction limit: 100-250 monthly

- Deposits: $5,000-$20,000 fee-free cash deposits

- APY: None

- Member FDIC: Yes

- ATMs: Over 12,000 ATMs in 40 states

Overall, Wells Fargo has a huge physical presence, which might be a fit if you value in-person banking. But, its past actions and high fees for overdrafts, transactions, maintenance, and more make it less than ideal.

| Pros | Cons |

| Physical locations in over 40 states | High monthly fees and other costs |

| You can open an account online | No free checking accounts |

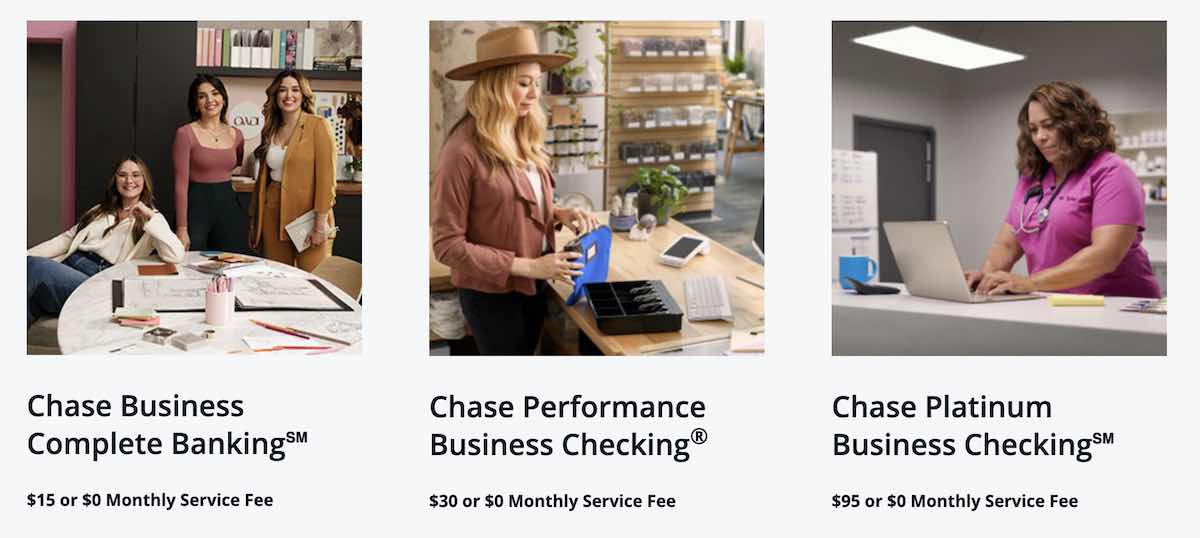

2. Chase

Best for: Companies of all sizes that want a wide range of business and personal financial services (checking, savings, financing, mortgage, etc.)

Chase offers many types of business banking accounts to suit different business sizes and needs. Let’s take a closer look at each in the comparison below.

| Business Complete Banking | Performance Business Checking | Platinum Business Checking | |

| Monthly fee | $15 (waived with $2,000 minimum balance) | $30 (waived with a $35,000 minimum average balance) | $95 (waived with a $100,000 minimum average balance) |

| Minimum deposit requirement | Not available | Not available | Not available |

| Transaction limit | 20 | 250 | 500 |

| Deposits | Unlimited electronic $5,000 free cash deposit limit | Unlimited electronic$20,000 free cash deposit limit | Unlimited electronic $25,000 free cash deposit limit |

| APY | No | No | No |

| Member FDIC | Yes | Yes | Yes |

Chase has locations in over 29 states and over 16,000 ATMs. It might be convenient if you need in-person banking and already have a personal banking account.

If you have a lot of monthly transactions or don’t want to worry about banking fees, then Chase isn’t the best business bank for you.

| Pros | Cons |

| Multiple checking account options to suit different business needs | Monthly fees, but they are waived if you meet the account balance threshold |

| Wide network of branches for in-person service | No APY for business checking |

3. Bank of America

Best for: Businesses that have large, monthly cash deposits and need in-person services.

Bank of America has two business banking accounts: Fundamentals and Relationship. The Fundamentals account is more suitable for small-to-medium businesses while Relationship is for larger enterprises.

Each account has various fees and requirements. Here’s the breakdown for the Fundamentals account:

- Monthly fee: $16 (waived with $5,000 monthly account balance)

- Minimum deposit requirement: $100

- Transaction limit: 200 per month

- Deposits: Free up to $7,500 and a .30 charge per $100 over

- APY: Not available

- Member FDIC: Yes

- ATMs: Over 4,500 locations and ATMs

| Pros | Cons |

| One of the largest and most established banks | Complicated monthly fees and requirements can mean more expensive banking costs |

| Branches and ATMs all over the country for in-person banking and cash deposits |

4. Mercury

Best for: Growing global and online-only startup businesses.

One of the reasons why xendoo partners with Mercury is that it’s tech-enabled banking at its finest. Compared to traditional banking platforms, it has an incredibly, user-friendly interface.

It has an API, so businesses can integrate other financial tools and services they use. For example, you can connect bookkeeping, payments, payroll, and more to your Mercury business banking account. This way, it’s easier to keep track of and manage your finances.

It also has Mercury Raise, a program that helps connect startups with investor funding.

You can sign up for a business banking account in 10 minutes.

They also have a non-traditional approach to business loans with Mercury Venture Debt. If your startup has raised venture capital (VC) funds in the past year, you could be eligible. Instead of looking at cash flow and other financial indicators, it looks at your investment team.

- Monthly fee: $0

- Minimum deposit requirement: $0

- Transaction limit: Unlimited, including savings account

- Deposits: Unlimited

- APY: Up to 5.10% yield with Mercury Treasury (as of writing)

- Member FDIC: Yes (up to $5 million)

- ATMs: Not available

| Pros | Cons |

| Free checking and savings accounts | No cash deposits |

| Helps startups with funding through Mercury Raise and its Venture Debt loan program. | It doesn’t accept some businesses (i.e. cannabis or businesses with many cash transactions) |

| No overdraft fees | |

| You can connect bookkeeping, accounting, payments, and other tools |

5. Citibank

Best for: Businesses that maintain a high monthly balance to avoid fees.

Citibank has also been around for a long time, so it has all the basic business accounts and some extras. It has several options for business checking accounts as well as savings accounts, credit cards, loans, and more.

However, it doesn’t have a free checking option. There are monthly fees unless you maintain an average monthly balance over $5,000 to $10,000, depending on the account you use.

- Monthly fee: $15-$30

- Minimum deposit requirement: $1

- Transaction limit: Limited free transactions (250-500 depending on the account)

- Deposits: $5,000-$2,000 free cash deposit limit

- APY: Not available

- Member FDIC: Yes

- ATMs: 2,300 ATMs

| Pros | Cons |

| Full suite of business services | All business checking accounts have fees (some are waived with a monthly balance) |

| Must open an account in-person at a local branch |

6. Capital One

Best for: Small businesses that want to build credit and make many purchases with a credit card.

Capital One is most known for its credit cards. However, it also offers personal and business banking services. There are two checking account options: Basic and Enhanced.

One drawback is that each account has monthly fees. Capital One waives them for account balances that average $2,000-$25,000 or more in the last 30 to 90 days. Its basic account also has fees for monthly cash deposits over $5,000. Then, you’ll pay $1 for every $1,000 over.

- Monthly fee: $15-35

- Minimum deposit requirement: $250

- Transaction limit: Unlimited

- Deposits: Unlimited

- APY: Not available

- Member FDIC: Yes

- ATMs: Over 70,000 through Capital One, MoneyPass, or Allpoint

| Pros | Cons |

| Business credit cards that offer cash back, travel, and other rewards | No free business checking |

| Business cards integrate with Quickbooks, Xero, and other accounting software | Monthly fees and cash deposit limits |

7. PNC

Best for: Small business owners that don’t have more than X transactions each month.

PNC has a wide range of banking account options. For example, it has specialized accounts for non-profits and law firms. Most organizations, however, will choose from two primary checking accounts for businesses. Here’s a comparison of the features for each.

| Checking | Plus | |

| Monthly fee | $12 (waived with a $500 minimum monthly balance) | $22 (waived with a $5,000 minimum monthly balance) |

| Minimum deposit requirement | $100 | $100 |

| Transaction limit | 150 | 500 |

| Deposits | $5,000 cash deposits | $10,000 cash deposits |

| APY | No | No |

| Member FDIC | Yes | Yes |

PNC has over 2,500 locations and 9,000 ATMs. It has a decent mobile app and in-person services. However, you must go to a PNC location to open an account. Also, some fees like overdraft costs and a monthly fee for direct integrations with Quickbooks and other software can add up.

| Pros | Cons |

| Wide selection of business accounts to choose from, including industry-specific ones | A monthly fee for some software integrations |

| Strong mobile app | Lower cash deposit and transaction limits |

| In-person banking services | Monthly fees, but they’re easy to waive |

8. US Bank

Best for: Startups that are also interested in easy loans and lines of credit.

US Bank has several business checking account options, including specialty ones for non-profits. Here are the three most popular options and a comparison of each.

| Silver | Gold | Platinum | |

| Monthly fee | $0 | $20 | $30 |

| Minimum deposit requirement | $100 | $100 | $100 |

| Transaction limit | 125 | 300 | 500 |

| Deposits | $2,500 free cash deposits | $10,000 free cash deposits | $20,000 free cash deposits |

| APY | No | No | No |

| Member FDIC | Yes | Yes | Yes |

US Bank has over 4,000 ATMs and branch locations in 26 states. It also offers many business loan options, including SBA and Quick Loans. Quick Loans focus on growing businesses with equipment, vehicle, and other purchases.

| Pros | Cons |

| Includes a wide range of business checking and loan options | Its checking account terms can be difficult to compare |

| Offers merchant services like payment processing and point-of-sale options for a fee | Monthly deposit limits are low with a complex tracking method |

9. TD Bank

Best for: Small businesses that want 24/7 support and more flexible in-person banking hours.

TD Bank has all the bells and whistles you need for a business checking account including mobile deposit, online bill pay, and ACH transfers. You can also apply for loans or lines of credit, but there is a vetting process.

However, like most established banks, it has a monthly fee, so you could be charged if your account doesn’t meet the average monthly balance requirements.

- Monthly fee: $10-35

- Minimum deposit requirement: $250

- Transaction limit: 200-500 free transaction limit

- Deposits: $5,000 cash deposit limit for most accounts

- APY: 0.05% APY for a business interest-bearing account

- Member FDIC: Yes

- ATMs: A few hundred (mostly on the east coast)

| Pros | Cons |

| Interest-bearing checking account options | No free business checking accounts |

| Some banks are open weekends and Sundays | It’s mainly located on the east coast |

10. Cogent

Best for: Best bank for local small businesses with complex regulation and banking needs.

Cogent Bank stands out with its commitment to providing customized services. For example, many big banks don’t offer accounts to cannabis companies because of the regulation. However, Cogent provides banking to cannabis and other industries with complex financial needs like blockchain and healthcare.

Another feature that sets Cogent apart is its Insured Cash Sweep® (ICS) service. It splits deposits that are over $250,000—the FDIC-insurable limit—into smaller chunks and sends them to member banks. You get interest-bearing and FDIC-insured cash deposits without the trouble of setting up and managing multiple accounts.

You can open a business banking account with Cogent online within minutes. Most will choose between two checking account options.

| Business Checking | Business Edge Checking | |

| Monthly fee | $0 | $50 (waived with $50,000 average monthly balance) |

| Minimum deposit | $0 | $0 |

| Transaction limit | 200 transactions per month | 500 transactions per month |

- Monthly fee: $0 for business checking

- Minimum deposit requirement: $0

- Transaction limit: 200-500 transactions per month with a $0.50 charge per transaction over the limit

- Deposits: Same as transactions

- APY: None

- Member FDIC: Yes

- ATMs: 8 Florida locations

| Pros | Cons |

| Customized banking solutions | Transaction limits |

| Experience in highly-regulated industries |

There are many business banking options, which can make researching all the features and choosing one a daunting task. Ultimately, the best business bank for you should offer a range of features with few banking fees.

FAQs

Which bank is best for a business account?

The best bank for a business account varies based on your specific business needs. Low fees, high APY, and a range of business-oriented services like merchant services can influence this decision. Researching and comparing the terms of each can help you make the right choice.

How are business and personal checking accounts different?

Business and personal checking accounts differ in terms of fees, transaction limits, and additional services. Business accounts cater to higher volume transactions and provide access to business credit. They also make it easier to manage payroll, invoicing, accounting, and more.